Relations between the German Bundesbank and the ECB are turning tense again. What dictates this complex relationship of ups and down is one thing and one thing only—the Bundesbank’s fear of inflation. When deflationary pressures occur (falling prices) the German Bundesbank tends to accord more leeway for the ECB and it mutes its hawkish stance.

But when German inflation is on the rise, then the trauma Germany experienced from the inflationary crisis of the 1930s comes rushing back. Then the Bundesbank’s stance becomes hawkishly vocal and relations become strained. So, what has caused Germany’s Bundesbank to “raise its voice” this time around? This time, it's a bit more complex than just inflation.

Germany Under The Hood

In a superficial analysis, the German economy is doing fine. Growth, while not staggering as Spain’s 3% but at 1.9%, it is still the higher than Frances’s 1.1% or Italy’s 1% GDP growth. Moreover German inflation hit 1.9% which matches the Bundesbank’s close to but below 2%, target inflation.

But when we dive deeper under the hood, the shine quickly wears off. Most of Germany’s growth was derived from exports. But actually from January to November of 2016, export growth was merely 0.8% and derived not from exports to China and the rest of the world but a 1.4% export growth the Eurozone, and more broadly, a 1.9% export growth to the EU countries. In fact, German exports to countries outside the EU shrank by -0.9%. Moreover, when we compare the aggregate growth in the Eurozone trade balance (until November) vs the growth in Germany’s trade balance the discrepancy becomes clearer. The trade surplus for the Eurozone was growing by 14% from January to November 2016, compared to a growth of 1.88% in the German trade surplus to the Eurozone and the rest of the world; from that we can conclude that Germany’s net exports (exports fewer imports) lagged the Eurozone’s aggregate growth.

Chart courtesy of Tradingeconomics

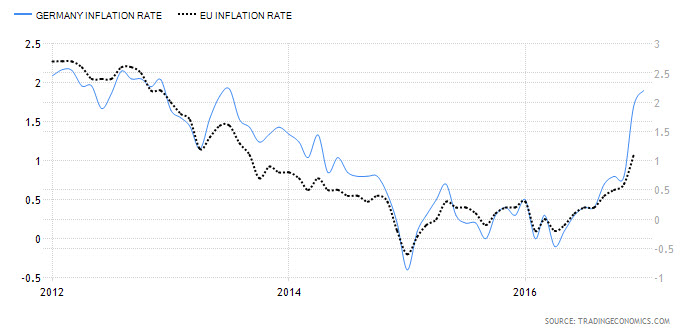

On the other hand, when comparing German inflation to the rest of the Eurozone, we can see that German inflation nudged higher to 1.9%, as compared with 1.8% of the Eurozone. Moreover, housing prices, as indicated by the German housing index, rose sharply in the last quarter of 2016. And that leads to the inevitable conclusion that the €1.4 Trillion of ECB stimulus that has flooded the Eurozone and kept the financial system afloat (albeit fragile) generated inflation in Germany but spurred export growth elsewhere. It is, therefore, unsurprising that the German Bundesbank is becoming uneasy with the ECB’s monetary policy. It accelerates inflation in Germany without real tangible growth in exports.

Chart courtesy of Tradingeconomics

The Bottom Line

The ECB has already tapered its monthly bond purchases under its QE program to €60 billion but that still means €780 Billion of bond purchases by year end. With December of 2017 as the deadline for the current program, the ECB might be pressured by the Bundesbank to reduce its purchases before the end of 2017. And that may potentially spell another crisis for the Eurozone.

The region still has a fragile banking system, with Italian and Spanish banks holding more than €400 billion of bad debt. In Germany, the banking system is not as well capitalized as the banking system in America. With no real deleveraging of bad debt and without restructuring of the banking system (not to mention the burden of labor regulations and high unemployment) and, now, without stimulus, that leaves the Eurozone prone to another stress inducing crisis.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Hi

Thanks to informations but i want results.