Introduction and Set-Up

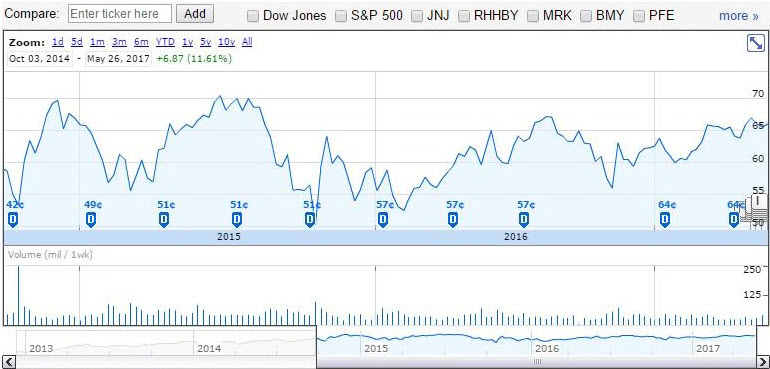

Below I’ll discuss my year-long call/put combination using AbbVie as an example. I’ve successfully been able to obtain a 15.3% return based on the current stock price while the buy and hold strategy would've only yielded 3.6% return. This is greater than a 400% difference in overall returns for this given stock over the past year. Leveraging the coupling of calls and puts around a core position over time can accentuate total returns and mitigate risk on a given stock. As discussed in more detail below, covered calls and covered puts can be combined to one's advantage. This is especially true in large-cap, dividend-paying stocks that tend to trade within a narrow range for long periods of time. AbbVie Inc. (NYSE:ABBV) is a prime example that fits this narrative and thus the stock of choice for this piece. Over the past two-plus years this stock has traded in a tight range between $55 and $65 per share while paying a dividend of ~4% on an annual basis (Figure 1). The company has strong fundamentals, financial stability and a robust pipeline for potential growth and sustainability. The goal here to initiate a position in AbbVie using a covered put to purchase the stock at a lower price than it's currently trading at a future date while collecting a premium in the process. If the stock isn't assigned then walk away with the premium and freed up cash that was earmarked for the potential purchase. If the stock is assigned, then shares are purchased at the agreed-upon price (strike price), less the premium for the actual purchase price. Now we've entered the position via leveraging a covered put, now the shares can be leveraged for covered calls to extract additional value throughout the holding of the stock while collecting the dividend. Ideally, we want to enter the position via a covered put and endlessly sell covered calls while collecting the dividend. However if the stock is called away during the selling of a covered call then this process can be repeated while being cognizant of the x-dividend dates to enhance overall returns.

Figure 1 – AbbVie’s tight trading range over the past 2-plus years

Options Trading: The Key to Accentuating Returns and Mitigating Risk

1. Why buy a stock now if you can purchase the stock in the future at a lower price while being paid to do so? (Covered Put)

2. As stock positions fluctuate, why not leverage these assets and collect residual income on a regular basis? (Covered Put or Covered Call)

3. Why own stocks at all when you can make money on the underlying volatility without owning the underlying security? (Covered Put)

Options trading is the key to addressing these questions and serves as a powerful means for generating income, mitigating risk and accentuating portfolio returns. Generally speaking, leverage is the key focus when engaging in options trading. This can be in the form of stock or cash as both are assets that can be leveraged to one's advantage. As easy as I can define options, technically, an option is a contract which gives the buyer of the contract the right, but not the obligation, to buy or sell the stock of interest at a specified price on or before a specified date. The seller of the option has an obligation to buy or sell the stock of interest if the buyer exercises the option contract. An option that gives the owner the right to buy the stock at a specific price is referred to as a call (bullish); an option that gives the right of the owner to sell the security at a specific price is referred to as a put (bearish or short).

Types of Options Explained (Calls and Puts)

Bullish (call) can be simply stated as when one believes a stock will rise in the future. Thus he/she will buy a call option to have the right to purchase the stock or sell a put option to take on the obligation to purchase the shares. In both cases, he/she believes that the shares will rise significantly. For example, in the first scenario, he/she is buying the call option to have the right to buy the shares of company X at $105 a month from now when the current price is $100. The buyer of the call option believes the stock will rise past $105 and thus be able to buy the shares for $105 (less the premium paid for the option contract) when they may be worth much more a month from now. In the second scenario, he/she is taking on the obligation to buy the shares of company X at $105 a month from now when the current price is $100. The seller of the put contract believes the shares will appreciate beyond the $105 level. Thus the owner of the shares would not exercise the option and assign shares to the put seller if the shares appreciate beyond $105. Why sell the shares at $105 to the put option seller when the owner of the shares could sell them on the open market for a higher price than $105? In this case, the put option seller collects a premium from the put option buyer and still makes money without owning any shares via premium income.

Conversely, bearish or short (put) can be simply stated as when one believes a stock will fall in the future. Thus he/she will sell a call option to have an obligation to sell the stock or buy a put option to have the right to sell the shares. In both cases, he/she believes that the shares will fall significantly. In the first scenario, he/she is selling the call option to take on the obligation to sell the shares of company X at $105 a month from now when the current price is $100. The seller believes the stock will fall or stay below the $105 level and thus be able to keep the shares and the premium paid for the option contract assuming the shares stay below the $105 level. In the second scenario, he/she is buying the right to sell the shares at $105 a month from now when the current price is $105. The buyer of the put contract believes the shares will fall below the $105 level. Thus the owner of the shares would exercise the option and assign shares to the put seller if the shares fall below $105. Why sell the shares below $105 on the open market when the owner can sell them to the put seller for $105? This is effectively an insurance policy against the shares falling. In this case, the put option seller collects a premium from the put option buyer and assigned shares at a higher price than the market price as a result of the shares falling.

AbbVie – A 15% Return Vs. A 3% Buy-and-Hold Return

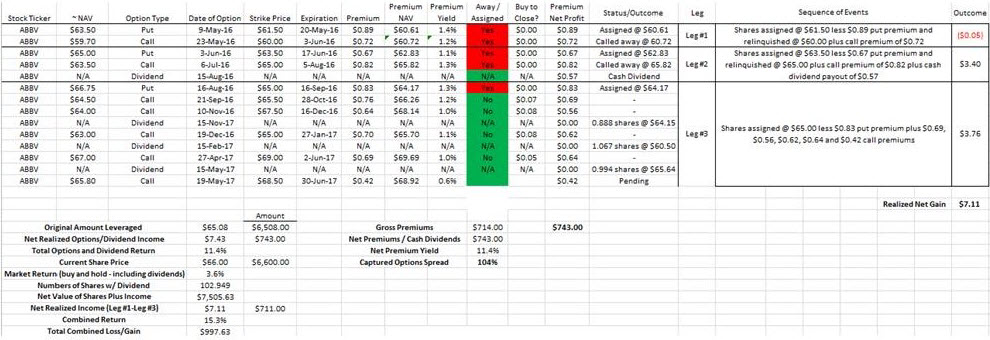

Putting this all together in an empirical case study, I’ve been able to leverage cash and stock in AbbVie over time to annualize a 15.3% return relative to a 3.6% in a buy and hold scenario. Leveraging covered put options may augment overall portfolio returns while mitigating risk when looking to initiate a future position in an individual stock. In the event of a covered put, this is accomplished by leveraging the cash one currently has by selling a put contract against those funds for a premium. Leveraging covered call options in opportunistic or conservative scenarios may augment overall portfolio returns while mitigating risk in a meaningful manner. In the event of a covered call/put combination, this is accomplished by leveraging the cash/shares one currently sits on by selling a call/put contact against those shares/cash and collecting a premium. Here, I’ll provide details focusing on optimizing stock/cash leverage via covered calls/puts (Figure 2).

Let’s walk through the most recent put/call combination that’s still active moving into June 2017. In August of 2016, I sold a covered put on AbbVie when the stock was trading at $66.75 for a strike of $65.00 ($1.75 less than the stock traded at the time of selling the option). I received $0.83 per share in option income which translates into $83 on the contract. AbbVie dipped below the strike of $65 and thus I was assigned shares at $65 less the $0.83 of options income to yield a net purchase price of $64.17 ($65 - $0.83). At this point I own 100 shares of AbbVie at $64.17 and now I can sell covered calls against my position. At this point I sold a string of 5 covered calls with dividend income layered in throughout the past ~ year. I netted covered call income of $69, $56, $62, $64 and $42 (pending) with reinvested dividend income of 0.888 shares, 1.067 shares and 0.994 shares. Total options income and reinvested dividend shares were $293 and 2.949 shares (market value of $195), respectively. Taken together, thus far for the most recent leg of this put/call combination, I’ve earned $488 of option/dividend income and $1.93 per share in stock appreciation. Income of $488 and stock appreciation of $193 translates into $681 or 10.6% return since August 2016 or ~0% over that same time period for the traditional buy and hold strategy.

Figure 2 – A year-long case study deploying a call/put combination on AbbVie to yield a 15.3%

Fates of Option Contracts (Covered Call Focus)/Option Expires Worthless

Three fates of an option come into play: 1) expires worthless, 2) assigned or 3) buy-to-close is executed to cancel the contract. An example of stock X, an owner of stock X sells a covered call at a strike price of $105. The current price is $100 and thus he is willing to sell the shares at $5 more than the current price in the future while collecting a contract premium in the process. This would imply a 5% potential appreciation in the stock on top of the current share price. If the share price fluctuates and remains below $105 throughout the contract time span and prior to expiration, the option will not be exercised and shares will not be relinquished. In this case, the seller of the call option would not relinquish shares as the stock did not reach the strike price of $105. This scenario will result in the option seller retaining the shares and keeping the premium payout. The option expires worthless in this scenario.

Option Is Assigned

Since the owner of the shares is selling the right to buy the shares to the option buyer at a strike price of $105 this increases the potential sale price by 5% from its current price of $100 if the option reaches the strike price. Factoring in the premium per share, the total return would be greater than 5% ($5.00 away from the strike plus premium). Let’s assume the stock reaches $106 prior to expiration, the call seller would relinquish shares at the agreed upon strike of $105 plus the premium paid out for the contract. In this case shares will be assigned to the call buyer.

Buy-To-Close

If the stock of company X increases during the contract time span while not moving above the strike price the time value will evaporate and decrease the value of the option contract itself. The further away the stock price is from the strike price in the negative direction the lower the option value. If the option decreases from $1.50 to $0.25, the option seller can buy-to-close the contract for $0.25 and capture the spread of $1.25 while canceling any right the buyer had to buy his shares. Now the shares can be leveraged again all while keeping all dividends rights and extracting additional value out of the shares. This buy-to-close scenario yielded a $1.25 spread in net cash per share of $125 per 100 shares.

Conclusion

Utilizing a year-long case study of a put/call combination on AbbVie Inc. (NYSE:ABBV), I’ve been able to produce a 15.3% return vs. a 3.6% market return when purchasing shares at $64.17 inclusive of all dividends. This translates into a 400% difference in overall return between the call/put combination and the traditional buy and hold strategy. The key takeaway here is initiate a position using a covered put to purchase shares at a lower price that the stock is currently trading at a future date. If the stock isn’t assigned then one still makes money on the option premium income. If shares are assigned, use these shares to sell covered calls in an effort to extract additional income while collecting the dividend. I sell covered puts into weakness to acquire shares at a discount or collect conservative income in a stock that likely won’t fall much further. I sell covered calls into strength to extract additional income from the underlying stock while collecting the dividend to accentuate returns.

Thanks for reading,

The INO.com Team

Disclosure: The author has no business relationship with any companies mentioned in this article. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.

You said:

"I sell covered puts into weakness to acquire shares at a discount or collect conservative income in a stock that likely won’t fall much further. I sell covered calls into strength to extract additional income from the underlying stock while collecting the dividend to accentuate returns"

.

How about the following strategy?

I SELL COVERED PUTS INTO STRENGTH TO COLLECT CONSERVATIVE INCOME (PREMIUM) IN A STOCK THAT I FOUND OUT BY APPLYING A DIFFERENT ANALYSIS THAT IT HAS THE POTENTIAL TO GO UP

AND,

iI SELL COVERED CALLS INTO WEAKNESS TO COLLECT CONSERVATIVE INCOME (PREMIUM) IN A STOCK THAT I FOUND OUT BY APPLYING A DIFFERENT ANALYSIS THAT IT HAS THE POTENTIAL TO GO DOWN?

Do you consider it a viable method?

Thanks.

Do you suggest any preferred strike price and preferred length of expiry date for this strategy?

Have you experimented this strategy with any other equity?

I use the exact strategy,because my IRA account does not allow me to do anything else.Have made money doing this but,lost some due lack of experience.held

Good..

I have been burned several times with wonderful gurus. Your method seems interesting ...how can I be sure that it will work regularly. I know buying options is dangerous and selling them is easier. However, if you get cashed(in the money)..where is the danger.

Gaetan Roy Fort Lauderdale