Controlling the overall systemic risk of a portfolio is essential as the markets continue to grapple with inflation, a rising interest rate environment, supply chain challenges, and the Russian/Ukraine conflict.

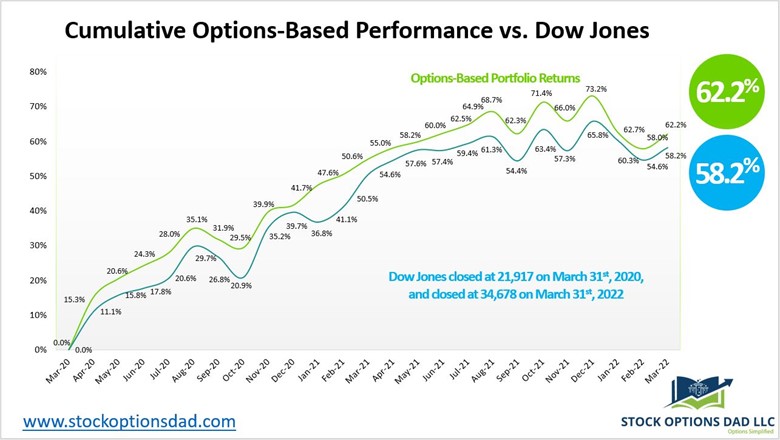

Controlling volatility while generating in-line or superior returns relative to the market is the goal of an options-based portfolio. An option-based strategy is achieved via a blended approach of options, long stock positions, and cash. Options alone cannot be the sole driver of portfolio appreciation; however, they can play a critical component in the overall portfolio construction while keeping volatility in check (Figure 1).

Generating consistent monthly income while defining risk, leveraging a minimal amount of capital, and maximizing returns is the core of an options-based portfolio strategy. They can enable smooth and consistent portfolio appreciation without guessing which way the market will move. Options enable the possibility to generate consistent monthly income in a high probability manner in various market scenarios. An options-based portfolio provides durability and resiliency to drive portfolio results with substantially less risk. Over the previous 2-year period, the portfolio strategy has consistently outperformed the Dow Jones with reduced volatility (Figure 1).

Figure 1 – Previous 24-month period of overall returns for the options-based portfolio strategy relative to the Dow Jones. All option and stock trades executed in the options-based portfolio is available via the Trade Notification Service

Options Screening Tool

Using basic technical indicators and key dates can aid in trade type selection, such as covered calls, put spreads, call spreads, or iron condors (Figures 2 and 3). Continue reading "Options-Based Portfolio Screening Tool"