Introduction

I’ve written a series of articles detailing the utility of options and how an investor can leverage a long position in an underlying security to mitigate risk, augment returns and generate cash without relinquishing the security of interest. I’d like to highlight Salesforce.com Inc. (NYSE:CRM) as an example for a covered call strategy. I’ll be highlighting how I’ve successfully extracted an additional double-digit return via leveraging the underlying security while collecting option premiums over a nine-month span. Taken together, the synergy of the options income and appreciation of the underlying security has yielded 23.6% over this timeframe.

Salesforce is a contentiously debated aggressive growth stock. On an annualized basis, Salesforce is not profitable and thus difficult to assign a valuation as measured by traditional metrics such as the price-to-earnings multiple (P/E ratio) and the PEG ratio. Due to its rapid growth, expanding footprint, major partnerships with Fortune 500 companies (i.e. Home Depot, GE, Wells Fargo, Coca-Cola, etc.), expansion into international markets and its overall ubiquity in terms of its consumer relationship management (CRM) platform, it's reasonable to see why investors are willing to pay a premium. Much of its revenue is deferred as a result of its subscription-based model thus deferred revenue is often discussed on earnings calls. Deferred revenue is not yet revenue however it’s been received by the company. Since Salesforce delivers its service over time, this received amount isn’t reported as traditional revenue since the service hasn’t been rendered. Due to these factors and the difficulty of placing an accurate valuation on Salesforce, options in the form of covered call writing may be an effective way to leverage this growth stock while mitigating downside risk. Salesforce offers the right balance of volatility, liquidity and a high level of interest which gives rise to reasonable yielding premiums on a bi-weekly or monthly basis. This set-up bodes well for those who are long Salesforce (or a stock similar in nature) and desire to leverage options trading to augment returns and mitigate risk throughout the volatile nature of this underlying security. Salesforce’s recent earnings impressed investors and covered call options may accentuate this underlying equity return. Writing covered calls in an opportunistic and/or disciplined manner may mitigate losses and smooth out drastic moves in this underlying security.

Note: This article is backing my long position in Salesforce while opportunistically and responsibly writing covered calls to mitigate downside risk and generate income. I provide my real life examples embedded into my long position as this stock can be volatile.

52-Week Narrow Trading Range

Salesforce has maintained a fairly narrow trading range throughout the past year with the exception of a major correction in February. This trading range has largely been confined to the $70-$80 range with a 52-week high of $84.50 (Figure 1). This narrow trading range for a relatively volatile stock can bode well for options traders.

Figure 1 – 52-week trading range of Salesforce

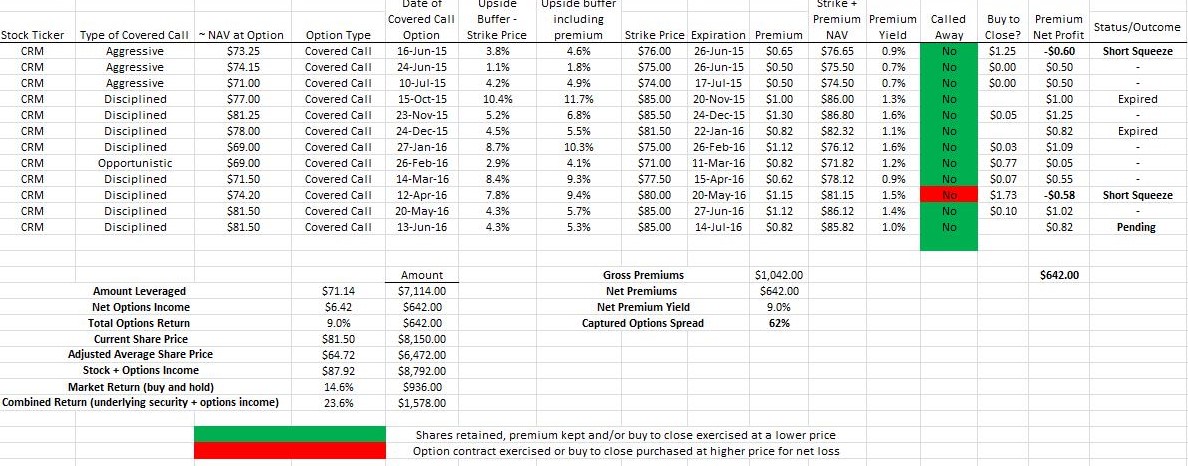

Riding the uptrend waves to the higher end of the 52-week range while writing covered calls one can extract additional value in a long position. Tables 1 and 2 provide the details of each option contact and its classification that I’ve loosely defined as aggressive, opportunistic or disciplined. I assign “aggressive” to options that are typically over short time durations with a strike price that is near the money thus running a high risk of relinquishment. I assign “disciplined” to options that are typically over longer time durations with a strike price that falls far out-of-the-money (~7% higher than the current price). I assign “opportunistic” as a rare scenario in which the underlying security skyrockets high-single digits or low double-digits in a single session or over the course of two to three trading days. This typically occurs over after an earnings beat and rise in guidance.

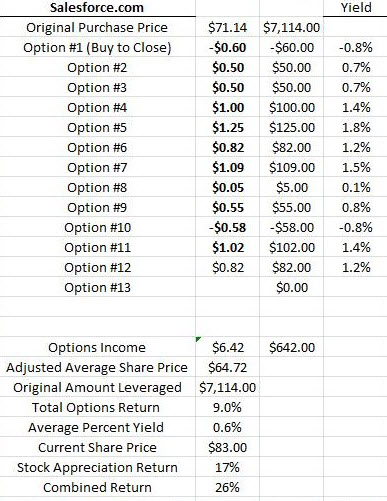

Table 1 - Original purchase price $71.14 along with subsequent options contracts

As detailed in Table 1, I’ve been able to extract an additional 9% in the form of options premiums while the appreciation of the underlying security has an unrealized gain of 14.6%. Taken together, the synergy of the options income and appreciation of the underlying security has yielded 23.6% over the course of roughly 9 months.

Table 2 – Simplified table of the options contacts on Salesforce stock

Opportunistic Spikes And Writing Covered Calls Into Earnings

During the week of October 20th, 2015, on the heels of very robust earnings from Microsoft, Amazon, and Alphabet (Google) the entire tech sector benefited and stocks such as Salesforce witnessed a strong uptrend as a result. I wanted to capitalize on this uptrend as Salesforce broke through its 52-week high at the time. For this options trade, I targeted my soft 10% upside buffer factored into the strike price. For my Salesforce position, a 9% upside was built into the strike price ($85 strike - $78 at option) and factoring in the premium I arrived at a 10% upside buffer. This upside buffer was particularly important as earnings were underway. Salesforce reported earnings on 18NOV15 and handily beat estimates and the stock jumped 5% the next day and touched $83 per share. In this case, for a long position, this 10% buffer was necessary in order to remain in the position while extracting value via far out-of-the-money covered call option writing while factoring in the potential upside as witnessed after the conference call and with the overall uptrend in the stock.

In April/May 2016, Salesforce was stuck in a tight trading range between $74 and $77 per share. I decided to write a covered call when the stock reached $74 per share with a strike at $80 per share with an expiration date of 05/20/2016. Salesforce was due to report earnings on 05/18/2016 just prior to the expiration of this contact. I wrote the option at risk knowing that if the earnings report turned out to be positive, the stock would likely rise higher than the strike of $80. Due to the overall upside of ~9.4% (appreciation in the strike plus the premium yield), I would be effectively paid $81.15 per share if relinquished. However, I was writing this option at risk due to the increased uncertainty surrounding the upcoming earnings report. The earnings report would either move the stock up or down in a dramatic move. I wanted insurance in the event the report turned out to be negative and unfortunately for me this strategy didn’t work out too well (Tables 1 and 2) and I had to buy back the option at a loss in order to avoid relinquishment.

Summary

Salesforce is a highly debated stock and isn’t intended for value investors. Salesforce has been growing at a double-digit clip on an annualized basis, and this impressive growth will likely continue in the near-to-intermediate term as cloud-based analytics are the future to any enterprise business more specifically in the CRM space, not to mention the highly acquisitive nature of Salesforce. In the meantime, as a long investor, writing covered calls in opportunistic scenarios may mitigate these drastic swings in the stock price while generating income. This is especially true given Salesforce’s recent earnings strength and underscores the value of covered call writing to mitigate potential downside swings and smooth out drastic moves in this underlying security. Taken together, options income may greatly augment overall returns as detailed above.

Thanks for reading,

The INO.com Team

Disclosure: The author currently holds shares of CRM and the author is long all this position. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.