Over the past two years, it seems, Brazil has remained in the headlines for the very worst of reasons – corruption. In fact, the very latest scandal at Petrobras, the state owned petroleum giant, reached all the way to its upper echelon. Long gone are the days when the Brazilian government was praised for its fiscal discipline; the situation there has become so notorious that the name Brazil, it seems, has become synonymous with corruption. And as if this were not bad enough the country's main exports, which range from iron ore to agricultural goods, have tumbled in crisis. Yet, as investors, we always seem to intuitively look at the bright side of even the worst situation; in this case, we have thoughts of buying because when the situation is as bad as it is, we think, from here on out, that the situation can only get better. The Brazilian economy is basically at a standstill with a weak government at the helm, and there is one corruption scandal seemingly after another, and given the softness in commodities' prices the question that investors want an answer to is this: is the collapse in the Brazilian Real over?

A Broken Banking System

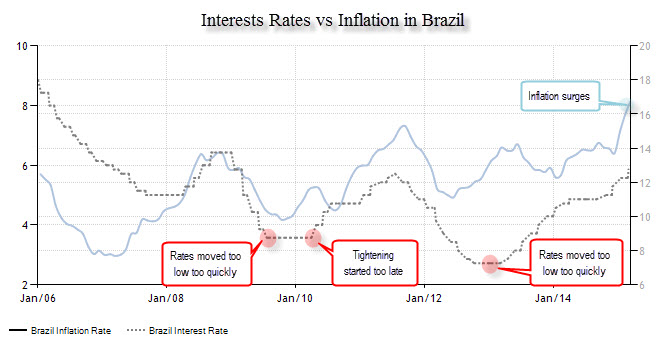

While many see corruption as the core problem in Brazil, this writer thinks the true core and the basis of the problem is, in fact, rooted in the country's banking system and at its heart, with Brazil's central bank, the Banco Central do Brasil. While reforms in the country are key for future growth it is the credibility of its central bank that is key for the Real, and as the chart below reveals, credibility is sorely lacking.

Chart courtesy of Tradingeconomics.com

The central bank has marked the 4.5% as the desired target for inflation. Yet the Brazilian central bank, generally amid political pressure to spur growth, has always eased policy prematurely and too aggressively. However, when it comes to tightening, the fact is the central bank doesn't apply those same standards. When in 2009 inflation peaked, rates were cut quickly, to as low as 8.75%, and left unchanged for several months. Soon after, though, inflation spiraled out of control once again, above 7%. And yet again, the Brazilian central bank was behind the curve, tightening too slowly and allowing inflation to move outside its targeted range. Once inflation slowed to 4.91% the central bank once again cut rates, this time even more aggressively than before, and the results were not pretty. As seen in the chart, inflation was soon out of control, to the extent that the latest reading on inflation hit 8.13%, once again spurred on by a central bank that hands out rate cuts much too easily.

Implications for the Real

With this pattern repeating itself, the question is what is next for the Brazilian Real? Quite simply, it means that, at some point, inflation in Brazil will ease once more but rather than being a buying opportunity it will only provide a temporary respite before the next inflation spiral. The problem is, and as reflected in the chart above, that with each and every wave, inflation comes back more fiercely, reaching to higher peaks and putting more pressure on the country’s bond and credit markets. With a central bank that tends to abandon price stability in favor of growth, and with demand for commodities set to continue to be soft, the pressure on Brazil and the Real will only rise with time. Unless the Banco Central do Brasil finally decides to exercise vigilance and curb the country's very sticky inflation, the situation in Brazil is on the brink of turning from bad to ugly. And that means that while the Brazilian Real has already fallen quite substantially, there is still more downside ahead.

How Low Can It Go?

Of course, with such a fragile economy, things could quickly spiral out of control and set new historic highs for the USD/BRL; the first reasonable target, then, considering the steeper slope for the country, is the 3.98 peak.

Timing is Key

But while the path towards a lower Real seems to be in the making, one must remember that volatility is high and therefore taking a short position on the BRL at the wrong time could substantially narrow any potential gains. Hence it would be wise to wait first for the next wave of inflation. Once inflation in Brazil begins to come down then it would be reasonable, given the historical evidence, to believe that the Central Bank of Brazil will cut rates too early which will precipitate the next crisis and with that the USD/BRL could hit the highs last seen in 2002 of 3.98.

Chart courtesy of Netdania.com

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Hi Mike,

Thank you for following me. As per your question I think this projection is still valid. True it is taking more time to materialize than I initially expected but the fundamentals remain the same and hence there is no reason for me to change my view. Moreover if you examine the USD/ILS chart you can see that the pair can quickly switch from sideways to abrupt bullish momentum.

Hope this helps.

What happened to your prediction of the Israeli shekels hitting 4.20