There's nothing like an investment that pays off even if there's no capital appreciation. That's the appeal of renting out your home instead of selling it – you get income along with and investment. The way markets are behaving right now with the Fed rate hike delayed once again, most likely until 2016, and uncertainty driving investor decisions, picking a stock that can pay out in more than one way is a huge benefit.

Limited partnership entities differ from traditional corporations in the sense that they are obligated to pass on a lion's share of the profits to shareholders. That gives them an edge when it comes to dividend yields and makes them defensive even if they're not necessarily in a defensive sector of the economy.

The oil and gas pipeline industry might not seem like a defensive environment given what's happened with commodities and energy prices, but this sub-sector operates a little differently. Pipelines are more on the midstream segment of energy operations giving them a more stable business with steady growth prospects regardless of energy prices.

Pipeline companies have a high barrier to entry with an expensive network of pipes to maintain making them safe from outside competition. And since energy will always be in demand, there's more stability than most energy stocks possess.

A pipeline LP with a strong dividend and healthy growth prospects

Targa Resources Partners LP (NGLS) is a $6 billion midstream oil and natural gas energy company that operates throughout North America. The company has spent a billion in capital investments to expand its growth with another $2 billion planned for the future as well making this LP a very active company committed to long-term value.

The stock hasn't done well so far this year – down 28% year-to-date and down 45% in the past 12 months. The company has missed earnings for the last two quarters amidst a difficult environment for MLP's earlier this year but now the company looks poised to move higher.

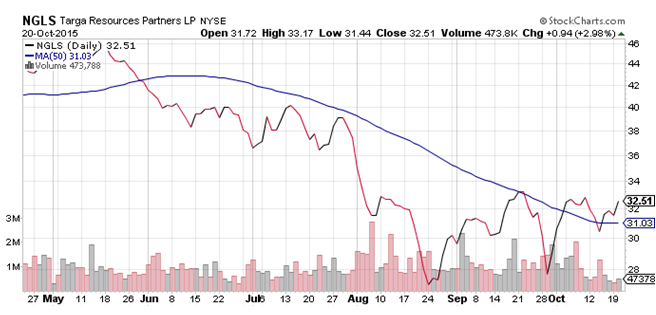

If we take a look at Targa's chart, we can see some bullish indicators.

Chart courtesy of StockCharts.com

The stock closed north of the 50-day moving average just this month and has mostly stayed above it sending a bullish signal to investors. It also appears to have bounced off its earlier lows and should be moving higher and building up positive momentum up to the end of 2015 as well.

Since those couple of difficult quarters, things have turned around quite a bit for the pipeline company. In fact, current quarter earnings estimates have gone up for $0.64 per share to $0.65 per share and full year earnings estimates were raised from $1.87 to $1.91.

Arguably, the biggest appeal of Targa's stock is the hefty 10% dividend yield. As an LP, the company must pass through the majority of its profits on to shareholders which tends to make MLP's and LP's high dividend paying stocks to own. Targa's yield is roughly five times the yield on the 10-year Treasury and the average yield from dividend paying stocks in the S&P 500 making this stock a great choice for income-oriented investors.

From a value perspective, Targa holds plenty of appeal. It trades much cheaper at 20.8 than the pipeline industry average of 35.5. Distribution growth has been positive since its IPO at 12% annually proving that management has taken steps to ensure the company has a steadily increasing profit base. Targa has also done a good job managing its backlog with around $750 spent this year on growth projects and between $350 million to $500 million next year. In total, the company has about $4 billion in the pipeline for fee-based projects that will help boost distribution growth making this company a solid choice in the MLP space.

Given the companies current earnings projections of $1.91 per share, this stock should be trading at around $39 per share. Along with a 10% dividend yield, that gives investors a potential gain of about 30%.

Check back to see my next post!

Best,

Daniel Cross

INO.com Contributor - Equities

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

Thanks for the heads up!