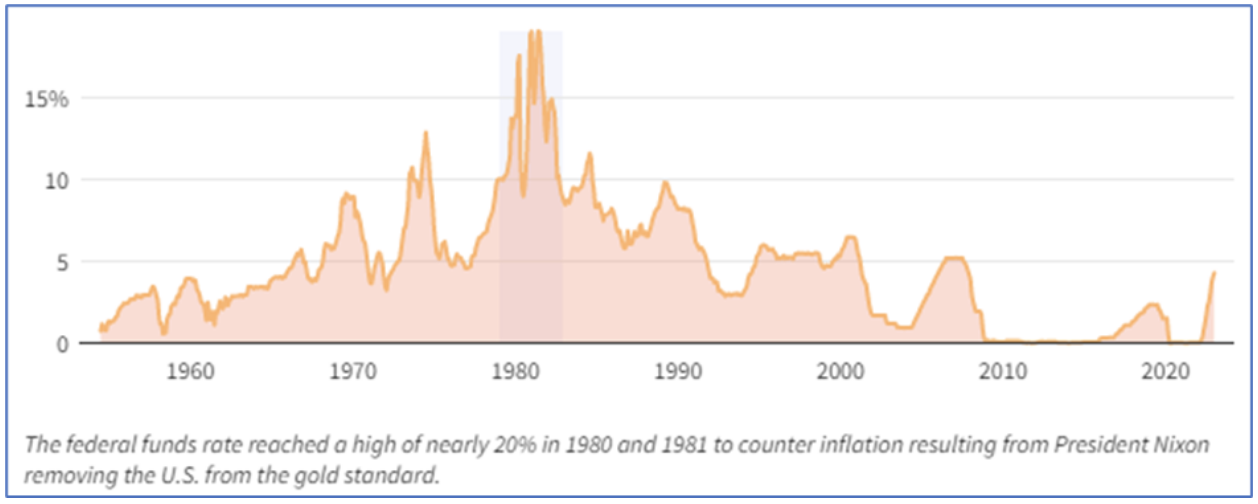

Last year, when the Federal Reserve realized that the inflation, which was earlier thought to be “transitory,” might be feeding on itself and soon spiral out of control, it acted swiftly to respond with an aggressive interest rate hike cycle, one of the quickest on record.

As a result, we have gone from living in a world of virtually free money, marked by a target federal funds rate of 0% to 0.25%, for more than 12 years since the global financial crisis to a world of constricted credit, with a target rate at 4.50% to 4.75%, the highest since 2007.

Right on cue, the market and economy responded to the end of the era of easy money with withdrawal tantrums. Although the Fed has been able to bring down CPI inflation from a 40-year high of 9.1% in June 2022 to 6.4% in January 2023, it has come at the cost of increased market volatility, stressed margins due to increased borrowing costs, and bank runs due to bond price devaluations.

Given that the federal funds rate appears to be nothing short of a force of nature for the capital markets and the economy at large, its deeper understanding would serve market participants well.

What is the Federal Funds Rate?

The federal funds rate is the interest rate that banks charge other institutions for lending excess cash to them from their reserve balances on an overnight basis.

Legally, all banks are required to maintain a percentage of their deposits as a reserve in an account at a Federal Reserve bank. This mandated amount is known as the reserve requirement, and compliance of a bank is determined by averaging its end-of-the-day balances over two-week reserve maintenance periods.

Banks, which expect to have end-of-the-day balances greater than the reserve requirement, can lend the surplus to institutions that expect to have a shortfall.

The Federal Open Market Committee (FOMC) guides this overnight lending of excess cash among U.S. banks by setting the target interest rate as a range between an upper and lower limit. This target interest rate is called the federal funds rate.

How is it Determined?

The FOMC is the policy-making body of the Federal Reserve. It is constituted by the members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining 11 Reserve Bank presidents.

The FOMC meets eight times a year to set the target federal funds rate, based on the prevailing economic conditions, as part of its monetary policy designed to serve its dual mandate of ensuring maximum economic growth and employment while keeping inflation under control.

It is important to note that the federal funds rate, set and meant to serve as guideposts, can’t be imposed by the FOMC. The actual interest rate between banks is negotiated, and the weighted average of interest rates across all transactions of this type is known as the effective federal funds rate.

However, the Federal Reserve influences the effective federal funds rate through open market operations, which involve buying and selling government securities to adjust the money supply in the banking system. Interest rates are inversely proportional to the amount of money in the system.

Why is the Federal Funds Rate Important?

Fabled investor Warren Buffett once said, "interest rates are to asset prices what gravity is to the apple.” He further added that they “power everything in the economic universe.”

Here are a few ways the federal funds rate influences our economic prospects, directly or otherwise:

- By determining the cost of money in the U.S. economy, the Federal Reserve tries to strike a balance between economic growth and demand-driven inflation. A low rate increases the economy's liquidity, making borrowing cheaper and stimulating growth.

- However, when excessive growth and subsequent inflation threaten to reduce purchasing power, the Fed can raise interest rates to slow inflation and return growth to more sustainable levels.

- Since interest rates are used to discount future cash flows while determining the value of the assets, low-interest rates inflate asset prices, while high-interest rates deflate them. This could be the reason for the downward volatility currently witnessed in the capital markets.

- Asset price inflation in an environment of low or decreasing interest rates makes holders of those assets feel richer and willing to spend more which acts as an added tailwind for the economy.

- Low-interest rates make borrowing cheap and encourage businesses to invest in facilities and equipment, which stimulates economic growth. The low cost of capital ensures that businesses operate with healthy margins and look more profitable.

- Falling interest rates make returns from safe investments look paltry and incentivize investors to seek out riskier investments while demanding a modest premium for taking on additional risk. This increases the inflow of funds into equities and other speculative asset classes (cryptocurrencies, SPACs, “growth” companies, etc.), creating asset bubbles.

- An environment of high or increasing interest rates stimulates investors' “risk off” mindset and makes returns from safe investments look more attractive. Hence investors demand higher returns and risk premiums from riskier investments leading to an outflow of funds and the subsequent bursting of bubbles created earlier.

- When the Federal Reserve increases the fed funds rate, it typically increases interest rates throughout the economy, strengthening the dollar. This makes imports cheaper but ends up hurting exports.

- On the other hand, the currency's weakness, costlier imports, but more profitable exports are characteristic of a decreasing or low interest-rate environment.

How to Take Advantage When the Fed Raises Rates?

Investors, speculators, and consumers can benefit or limit losses from increases in the fed funds rate in various ways, depending on their risk appetite and investment horizon. Some possible ways are:

- Investing in U.S. dollar-denominated assets, such as Treasury bills, bonds, certificates of deposit, or money market funds. The higher yields attract investment capital from investors abroad seeking higher returns on bonds and interest-rate products.

- Investing in short-term interest-rate products, such as floating-rate notes, adjustable-rate mortgages, or bank loans. These products have interest rates that adjust periodically based on benchmark rates, such as the fed funds rate. Hence, when the fed funds rate increases, these products also increase their interest rates, which means higher income for investors.

- Shorting long-term-interest-rate products, such as fixed-rate bonds or mortgages. These products have fixed interest rates that do not change over time, which means their prices decline to raise their yields when interest rates rise. Investors who expect interest rates to rise can sell these products at a higher price and buy them back at a lower price later, making a profit from the markdowns.

- Using credit cards wisely. When the Fed raises interest rates, credit card debt becomes more expensive since the interest charged by credit card companies usually moves in lockstep with the federal funds rate. However, reward programs that offer cash back to borrowers who pay off their dues in full every month also become more valuable.

- Taking advantage of higher savings rates. Higher interest rates mean higher returns on savings accounts, certificates of deposit, or money market accounts. Savers could shop for the best rates and lock in their deposits for longer terms to earn more interest.

Best,

The MarketClub Team

su*****@in*.com