There was a lot of talk about potential host cities for the Olympics lately and the politics associated. That talk died down after Brazil was awarded the honor of hosting. You may be asking "how does that relate to trading"...well my friend Raul of the Shocked Investor is about to make that connection. He has been researching the Brazilian stocks and options recently and more importantly ones traded on American exchanges. Enjoy the article and be sure to leave a comment with your thoughts.

----------------------------------------------------------------------------------------------------------------

With Rio de Janeiro having just being awarded the Olympics 2016 there will be enormous activity and interest in Brazil. There will be tremendous investments made in the city and in the country. Whether the government itself makes a profit money-wise is a difficult proposition, and difficult to measure. However, the benefits to the country are long term and in many other indirect areas. Many companies and sectors will certainly boom and make considerable revenue. Over the next months and years we will dedicate considerable effort to dissecting these companies and sectors to pinpoint the winners. Also, in future posts, we will be talking about other companies, while not directly Brazilian ADRs, but that do most of their business - of profits - in Brazil. I know these companies and the market well, and have very good connections over there. Much more on this later. Also, please see another recent post on Brazil on September 23, with expert interviews on BNN TV.

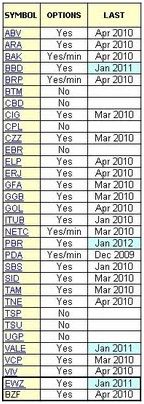

This article shows all the current Brazilian ADRs. These are securities that can be traded in North America, like regular stocks. Most have good volumes, and most of them have options as well. Some of the companies are very large and are among the biggest in the world. For example, ITUB has a market cap of over $90B, much higher than most banks in the world. VALE is at $120B, VIV $10B, ABV, $52B, BBD $61B, and so on.

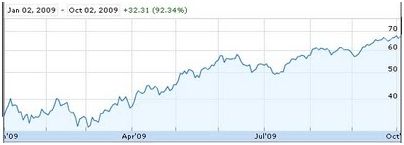

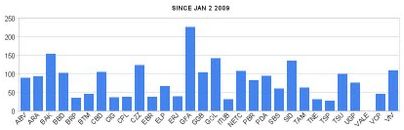

Two ETFs are also shown, EWZ for Brazilian stocks, and BZF which tracks the Brazilian currency. You will see that these stocks have gone up sharply this year. The EWZ is up over 93%, partly due to the appreciation of the Real and the drop of the U.S. Dollar. The top gainer year-to-date is a builder, whose shares (ADRS) have gone up nearly 200%. Other companies have gone up over 200% in the last 6 months. Their RSI values are stratospheric, so this is clearly a 'buyer beware' situation. If there is the long-awaited correction in the stock market and another safety flight to the U.S. Dollar occurs, these stocks could well be severely punished. There will be many opportunities for the patient investor.

----------------------------------------------------------------------------------------------------------------

This weekend, Brazil just reported an 8th consecutive increase in industrial production:

----------------------------------------------------------------------------------------------------------------

The economy is not immune to the global crisis. However, the increase of its internal market, as well as its diversification of exports (China is now its largest export market) has certainly helped its resiliency. Overall production in 2009, however, is still down 12% compared with 2008.

Most of these companies with ADRs are world-class and leaders in their field. Names such as Petrobras, Vale do Rio Doce do not need introduction. Most are extremely reputable and well-managed companies.

We also maintain sites that track live all ADRs in Latin-America, as well as all global currency ETFs and ETNs. Click on the links to view intra-day prices and YTD charts.

COMPANIES AND ETFS, AND THEIR SECTORS

Note that all the Brazilian companies in the S&P Latin American 40 index are included in the group above. All these companies also trade in the Bovespa, Sao Paulo's stock exchange (4th largest in the world).

List of ADRs, ETFs, company names, and their sectors:

----------------------------------------------------------------------------------------------------------------

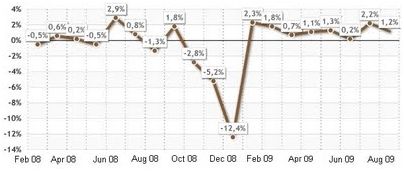

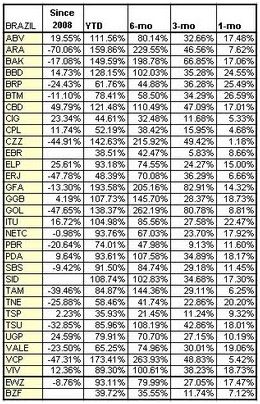

PERFORMANCE

Performance since Jan 2008, Jan 2009, last 6 months, 3 months, and 1 month:

YTD Chart:

----------------------------------------------------------------------------------------------------------------

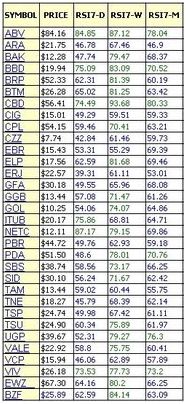

RSI VALUES

Below is the current table of RSI7 values (daily, weekly, and monthy) for all Brazilian ADRS plus the ETFs. The average values for the ADRs are:

daily: 58.2

weekly: 72.5

monthly: 64.6

The weekly is overbought, the monthly almost, and the daily is quite high. Note that for EWZ the values are 64/80/76, slightly higher than the average of all the companies. The top holdings of the ETF are included in the above list, but it's not a perfect match.

Note that sell alerts were triggered for ELP and PDA. These are the RSI7s:

----------------------------------------------------------------------------------------------------------------

As you can see, many of the stocks are clearly overbought.

----------------------------------------------------------------------------------------------------------------

PRICE/EARNINGS RATIO

The table below shows the trailing and forward Price/Earnings ratios from various sources.

----------------------------------------------------------------------------------------------------------------

AVAILABILITY OF OPTIONS

The use of stock options is very important to reduce cost basis (by selling calls and puts) as well as for protection. In addition, options and LEAPS (long term options) allow for leverage on the stock price. If you believe these stocks will continue to rise into the far future, then buying LEAPS can be quite attractive. Selling them (or short term options) allows for good income generation. There are many other strategies that can be used with options. With regards to the Brazilian ADRs, these strategies will be discussed in more detail in future posts.

----------------------------------------------------------------------------------------------------------------

COMPANY ANALYSIS & DETAILS

This section lists all companies, provides a business description, summary of financials, and analyst recomendations where available.

ABV, Ambev

Companhia de Bebidas das Americas – AmBev engages in the production, distribution, and sale of beer, draft beer, malt, carbonated soft drinks, and other non-alcoholic and non-carbonated products in the Americas. It also sells bottled water, isotonics, and ready-to-drink teas. The company primarily offers its products under the Skol, Brahma, and Antarctica brand names. Companhia de Bebidas das Americas has a licensing agreement with Anheuser-Busch, Inc. to produce, bottle, sell, and distribute Budweiser products in Canada. It distributes its products through third-party distributors and direct distribution centers. The company was founded in 1888 and is headquartered in Sao Paulo, Brazil. Companhia de Bebidas das Americas – AmBev is a subsidiary of Interbrew International B.V.

Market Cap (intraday): 51.84B

Enterprise Value (3-Oct-09): 54.37B

Trailing P/E (ttm, intraday): 24.49

Forward P/E (fye 31-Dec-10): 15.14

PEG Ratio (5 yr expected): 1.24

Price/Sales (ttm): 4.06

Price/Book (mrq): 4.22

Enterprise Value/Revenue (ttm): 4.34

Enterprise Value/EBITDA (ttm): 9.957

ARA, Aracruz

As of August 26, 2009, Aracruz Celulose S.A. was acquired by Votorantim Celulose e Papel S.A. (please see VCP), creating Fibria. Aracruz Celulose S.A. engages in the production and sale of bleached hardwood kraft market pulp. It produces eucalyptus pulp, a hardwood pulp used by paper manufacturers to produce various products, including premium tissue, printing and writing papers, liquid packaging board, and specialty papers. Aracruz sells its products in North America, Western Europe, Asia, and Brazil. The company was founded in 1967 and is headquartered in Aracruz, Brazil.

Market Cap (intraday): 22.42B

Enterprise Value (3-Oct-09): 26.39B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): 18.28

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 10.82

Price/Book (mrq): 24.63

Enterprise Value/Revenue (ttm): 13.09

Enterprise Value/EBITDA (ttm): 47.582

BAK, Braskem

Braskem S.A., together with its subsidiaries, operates as an integrated petrochemical cracker and thermoplastics producer primarily in Brazil. It offers olefins, such as ethylene, polymer and chemical grade propylene, butadiene, isoprene, and butene-1; aromatics comprising benzene, toluene, para-xylene, ortho-xylene, and mixed xylene; caprolactam, cyclohexane, cyclohexanone, and ammonium sulfate; automotive gasoline and liquefied petroleum gas; and methyl tertiary butyl ether, solvent C9, and pyrolysis C9 primarily for manufacturing intermediate second generation petrochemical products. The company also produces electric power, steam, compressed air, and purified drinking and demineralized water. In addition, it offers polyethylene and polypropylene for use in consumer and industrial applications, such as plastic films for food and industrial packaging, bottles, shopping bags and other consumer goods containers, automotive parts, and household appliances. Further, the company engages in producing suspension polyvinylchloride (PVC) for the manufacture of pipes, fittings, laminated products, shoes, sheeting, flooring, cable insulation, electrical conduit, packaging, and medical applications; paste PVC for producing toys, synthetic leather, flooring materials, bottle caps and seals, automobile corrosion prevention treatments, and wallpaper coatings; ethylene dichloride for the manufacture of PVC; and caustic soda for aluminum, pulp and paper, petrochemicals and other chemicals, soaps and detergents, and waste treatment plants applications. Additionally, it distributes chemical and petrochemical products comprising solvents, such as aliphatic, aromatic, synthetic, and ecological solvents; polymers; and general purpose chemicals, which include process oils, chemical intermediates, blends, specialty chemicals, pharmaceuticals, and santoprene. The company, formerly known as Copene Petroquimica do Nordeste S.A., was founded in 1972 and is headquartered in Camacari, Brazil.

Market Cap (intraday): 6.37B

Enterprise Value (3-Oct-09): 10.54B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): 29.95

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 0.7

Price/Book (mrq): 2.24

Enterprise Value/Revenue (ttm): 1.17

Enterprise Value/EBITDA (ttm): 8.5

BBD, Bradesco

Banco Bradesco S.A. provides a range of banking and financial products and services to individuals, small to mid-sized companies, and local and international corporations and institutions. It operates in two segments, Banking, and Insurance, Pension Plans, and Certificated Savings Plans. The Banking segment comprises deposit taking activities, including checking accounts, investment deposit accounts, traditional savings accounts, time deposits, and interbank deposits; individual and corporate banking services, credit operations, real estate financing, agricultural loans, leasing operations, credit and debit card services, leasing operations, investment banking, international banking, asset management, and consortium services. The Insurance, Pension Plans, and Certificated Savings Plans segment offers various products and services, including life and personal accident and occasional events insurance; health and dental care insurance; automobile insurance; property and casualty insurance; individual and corporate pension plans; certified savings plans; and pension investment contracts. As of December 31, 2008, Banco Bradesco S.A. operated a network of 3,359 branches; 29,218 ATMs; and 3,738 special banking service posts and outlets in Brazil. It also operated five branches and seven subsidiaries in New York, London, the Cayman Islands, the Bahamas, Japan, Hong Kong, Argentina, and Luxembourg. The company was formerly known as Banco Brasileiro de Descontos S.A. Banco Bradesco S.A. was founded in 1943 and is headquartered in Osasco, Brazil.

Market Cap (intraday): 61.21B

Enterprise Value (3-Oct-09): 101.36B

Trailing P/E (ttm, intraday): 19.55

Forward P/E (fye 31-Dec-10): 13.85

PEG Ratio (5 yr expected): 1.58

Price/Sales (ttm): 1.97

Price/Book (mrq): 2.85

Enterprise Value/Revenue (ttm): 3.35

Enterprise Value/EBITDA (ttm): N/A

BRP, Brasil Telecom S.A.

Brasil Telecom Participacoes S.A., through its subsidiaries, provides telecommunications services in Brazil. The company offers fixed-line telecommunications services, including local and long-distance, network usage, and public telephones services; mobile telecommunications services; and data transmission services, as well as operates an Internet portal under the brand name ‘iG’. It also provides traffic transportation services; value-added services, such as voicemail, caller ID, and directory assistance; and voice services to corporate customers. The company’s local fixed-line services include installation, monthly subscription, metered services, collect calls, and supplemental local services; and data transmission services comprise ADSL services and IP solutions, as well as the lease of dedicated digital and analog lines to other telecommunications services providers and ISPs, and corporate customers. As of December 31, 2008, it had approximately 8.1 million fixed lines in service; and 227,900 public telephones in service. The company was founded in 1998 and is based in Brasilia, Brazil. As of January 8, 2009, Brasil Telecom Participacoes S.A. operates as a subsidiary of Telemar Norte Leste S.A.

Market Cap (intraday): 3.79B

Enterprise Value (3-Oct-09): 5.45B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): N/A

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 0.59

Price/Book (mrq): 1.23

Enterprise Value/Revenue (ttm): 0.88

Enterprise Value/EBITDA (ttm): 4.78

BTM, Brasil Telecom

Brasil Telecom S.A., through its subsidiaries, provides telecommunications services for residential customers and governmental agencies, as well as small, medium, and large companies in Brazil. The company offers local fixed-line services, including installation, monthly subscription, metered services, collect calls, in dialing, and supplemental local services; domestic and international long distance services; fixed line to fixed line services; mobile long distance services; mobile telecommunication services; and data transmission services. It also provides broadband services, such as high-speed Internet access; Internet service provider services; commercial data transmission services comprising industrial exploitation of dedicated lines, dedicated line, and frame relay; public telephone services; and traffic transportation services. In addition, the company offers value-added services, which include voice, text, and data applications consisting of voicemail and caller ID, as well as other services, such as personalization, short message service subscription, chat, mobile television, location-based, mobile banking, mobile search, email, and instant messaging; and provides private telecommunication services through local optical fiber digital networks. Further, it provides call center services for third parties, including customer service, outbound and inbound telemarketing, training, support, consulting, and related services; and operates an Internet portal. As of December 31, 2008, Brasil Telecom had approximately 227,900 public telephones, and its access network served approximately 8.1 million fixed-line subscribers and approximately 1.8 million asymmetric digital subscriber line subscribers. The company was founded in 1963 and is headquartered in Brasília, Brazil.

Market Cap (intraday): 4.78M

Enterprise Value (3-Oct-09): 1.80B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): N/A

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 0

Price/Book (mrq): 0

Enterprise Value/Revenue (ttm): 0.29

Enterprise Value/EBITDA (ttm): 1.763

CBD, Companhia Brasileira de Distribuicao

Companhia Brasileira de Distribuicao operates as a retailer of food, clothing, home appliances, and other products through its chain of hypermarkets, supermarkets, and specialized and department stores primarily in Brazil. The company operates its stores under the names Pao de Acucar, CompreBem, Extra, Extra Eletro, Extra Perto, Extra Facil, Sendas, and Assai. As of December 31, 2008, it operated 597 stores. The company was founded in 1948 and is based in Sao Paulo, Brazil.

Market Cap (intraday): 13.37M

Enterprise Value (3-Oct-09): 1.11B

Trailing P/E (ttm, intraday): 0.06

Forward P/E (fye 31-Dec-10): 24.85

PEG Ratio (5 yr expected): 1.51

Price/Sales (ttm): 0

Price/Book (mrq): 0

Enterprise Value/Revenue (ttm): 0.1

Enterprise Value/EBITDA (ttm): 1.378

CIG, Cemig

Companhia Energetica de Minas Gerais (CEMIG) is a Brazil-based company involved in the energy sector. It is mainly engaged in the generation, transmission and distribution of electric energy for industrial, residential, commercial and rural consumption. The Company is also engaged in other businesses, such as natural gas distribution in Minas Gerais through Companhia de Gas de Minas Gerais (Gasmig); telecommunications through Empresa de Infovias SA, which provides fiber-optics and coaxial cable network installed along its transmission and distribution lines; national and international consulting business through Efficientia SA, which provides energy solutions for the implementation and management of systems for electricity sector, among others. In 2009, the Company is due to start operating abroad, through its subsidiary Transchile Charrua Transmision SA, in the Chilean unit LT Charrua – Nueva Temuco.

Debt/Equity Ratio 0.33

Gross Margin NA

Net Profit Margin -11.59%

Total Shares Outstanding 620.4M

Market Capitalization 9.31B

Earnings/Share -0.66

12-May-09 JP Morgan, Upgrade To: Overweight

15-Dec-08 Standpoint, Initiated: Buy

CPL, CPFL Energia

CPFL Energia S.A., through its subsidiaries, engages in the generation, distribution, and sale of electric energy. The company serves residential, industrial, and commercial customers in Brazil. As of December 31, 2008, it distributed electricity to approximately 6.4 million customers and had an installed capacity of approximately 1,704 megawatts. The company was founded in 1998 and is headquartered in Sao Paulo, Brazil.

Market Cap (intraday): 8.66B

Enterprise Value (3-Oct-09): 12.20B

Trailing P/E (ttm, intraday): 12.31

Forward P/E (fye 31-Dec-10): 20.06

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 1.52

Price/Book (mrq): 3.01

Enterprise Value/Revenue (ttm): 2.19

Enterprise Value/EBITDA (ttm): 7.609

21-Jul-08 HSBC Securities, Downgrade To: Neutral

29-Feb-08 Bear Stearns, Downgrade To: Peer Perform

CZZ, Cosan

Cosan Limited, through its subsidiaries, engages in the production and sale of sugar and ethanol in Brazil and internationally. The company also involves in the distribution of oil products, including ethanol, lubricants, and aviation fuel, as well as the operation of convenience stores through a network of 1,500 service stations in Brazil. It offers a range of sugar products comprising raw, organic, crystal, and refined sugars. The company sells sugar to wholesale distributors, food manufacturers, and retail super markets under the Da Barra brand. Its principal ethanol product is fuel ethanol, which is used as an automotive fuel and as an additive in gasoline. The company also produces and sells hydrous and anhydrous, and industrial ethanol; and sells liquid and gas ethanol products, which are used primarily in the production of paint and cosmetics, and alcoholic beverages for industrial clients. In addition, it involves in selling cogeneration of electricity and diesel. Cosan Limited was incorporated in 2007 and is based in Sao Paulo, Brazil.

Market Cap (intraday): 2.10B

Enterprise Value (3-Oct-09): 4.45B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Mar-11): N/A

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 0.56

Price/Book (mrq): 1.15

Enterprise Value/Revenue (ttm): 1.21

Enterprise Value/EBITDA (ttm): 14.224

24-Aug-09 Standpoint Research, Initiated: Buy

EBR: Centrais Eletricas Brasileiras S.A

Centrais Eletricas Brasileiras S.A. – Eletrobras primarily engages in the generation, distribution, transmission, and commercialization of electric power; and construction and operation of nuclear power plants in Brazil. The company also assists Brazil's Ministry of Mining and Energy in designing the country's policy for the energy sector; provides guarantees and acquires debentures of companies and holders of public electric power services; grants loans and guarantees for technical and scientific research institutions; promotes and supports research in the power sector in connection with the generation, transmission, and distribution of electric power, as well as studies involving the exploitation of watershed for various purposes; contributes to the education of technical staff and qualified workers required by the Brazilian electric power sector through specialized training programs or assists national educational institutions or provides scholarships or signs agreements with foreign institutions that promote the development of specialized technical personnel; and co-operates technically and administratively with companies in which it holds interests, and with the agency of the Ministry of Mining and Energy. In addition, it manages incentive program for alternative sources of electric power, a program of the federal government that aims to enhance the diversification of the Brazilian energy model and search for regional solutions based on renewable electric power sources produced by independent agents. The company is headquartered in Rio de Janeiro, Brazil.

Market Cap (intraday): 16.92B

Enterprise Value (3-Oct-09): 19.89B

Trailing P/E (ttm, intraday): 9.71

Forward P/E (fye 31-Dec-10): 17.74

PEG Ratio (5 yr expected): 0.8

Price/Sales (ttm): 1.1

Price/Book (mrq): 0.36

Enterprise Value/Revenue (ttm): 1.3

Enterprise Value/EBITDA (ttm): 6.24

ELP, Copel

Companhia Paranaense de Energia – COPEL, through its subsidiaries, engages in the generation, transmission, distribution, and sale of electricity for industrial, residential, commercial, and rural and other customers in Brazil. It generates hydroelectric and thermoelectric power. As of December 31, 2008, it operated 17 hydroelectric plants and 1 thermoelectric plant, with a total installed capacity of 4,549.6 megawatts. The company also provides corporate and international long-distance telecommunications services to telecommunication companies, supermarkets, universities, banks, Internet service providers, and television networks. As of December 31, 2008, it owned and operated 1,835.2 kilometers (km) of transmission lines and 179,187.6 km of distribution lines. In addition, the company engages in the distribution of natural gas through pipes to industries, thermoelectric plants, cogeneration plants, businesses, gas stations, and residences. Companhia Paranaense de Energia – COPEL was founded in 1954 and is headquartered in Curitiba, Brazil.

Market Cap (intraday): 4.81B

Enterprise Value (3-Oct-09): 4.83B

Trailing P/E (ttm, intraday): 8.34

Forward P/E (fye 31-Dec-10): N/A

PEG Ratio (5 yr expected): 1.74

Price/Sales (ttm): 1.54

Price/Book (mrq): 0.98

Enterprise Value/Revenue (ttm): 1.57

Enterprise Value/EBITDA (ttm): 4.629

ERJ, Embraer

Embraer – Empresa Brasileira de Aeronautica S.A., together with its subsidiaries, engages in the development, production, and sale of jet and turboprop aircraft for civil and defense aviation, and aircraft for agricultural use worldwide. It operates in four segments: Commercial Aviation, Defense and Government, Executive Aviation, and Aviation Services. The Commercial Aviation segment develops, produces, and sells commercial jets, as well as supplies support services. The Defense and Government segment designs, develops, manufactures, and supports a range of integrated solutions for the defense and government market. Its products include training/light attack aircraft, C4ISR (command and control, intelligence, surveillance, and reconnaissance) systems, aerial surveillance platforms, and transport airplanes. The Executive Aviation segment develops, produces, and sells executive jets, as well as provides support services. This segment markets executive jets to companies, including fractional ownership companies, charter companies and air-taxi companies, and high-net-worth individuals. The Aviation Services segment provides after-sales customer support services; and manufactures and markets spare parts for the fleets of its commercial, executive, and defense and government customers. The company also sells or leases used aircraft; provides structural parts, and mechanical and hydraulic systems; and manufactures general aviation propeller aircraft, such as executive planes and crop dusters. It has a strategic alliance with European Aerospace and Defense Group. The company was formerly known as Rio Han Empreendimentos e Participacoes S.A. Embraer was founded in 1969 and is headquartered in Sao Jose dos Campos, Brazil

Market Cap (intraday): 4.08B

Enterprise Value (3-Oct-09): 4.59B

Trailing P/E (ttm, intraday): 17.12

Forward P/E (fye 31-Dec-10) 1: 9.77

PEG Ratio (5 yr expected): 6.6

Price/Sales (ttm): 0.58

Price/Book (mrq): 1.32

Enterprise Value/Revenue (ttm): 0.66

Enterprise Value/EBITDA (ttm): 4.967

GFA, Gafisa

Gafisa S.A. operates as a homebuilder in Brazil. It engages in the development of residential buildings, including luxury buildings, comprising swimming pools, gyms, visitor parking, and other amenities for upper-income customers; buildings for middle-income customers; and entry-level housing for lower-income customers. The company also develops land subdivisions, and other mid-level and commercial buildings; and provides construction services, such as residential and commercial projects building services to third parties. It serves development and construction service clients. Gafisa S.A. was founded in 1997 and is headquartered in Sao Paulo, Brazil.

Market Cap (intraday): 3.93B

Enterprise Value (3-Oct-09): 4.45B

Trailing P/E (ttm, intraday): 60.85

Forward P/E (fye 31-Dec-10): 12.47

PEG Ratio (5 yr expected): 0.48

Price/Sales (ttm): 3.05

Price/Book (mrq): 3.86

Enterprise Value/Revenue (ttm): 3.85

Enterprise Value/EBITDA (ttm): 53.024

GGB, Gerdau

Gerdau S.A., through its subsidiaries, engages in the production and sale of steel products in Brazil and internationally. The company offers crude steel products, which include billets that are used to manufacture wire rods, rebars, and merchant bars; blooms for use in the manufacture of springs, forged parts, heavy structural shapes, and seamless tubes; and slabs, which are used in the steel industry for the rolling of various flat rolled products, as well as to produce hot and cold rolled coils, heavy slabs, and profiles. Its long rolled products include rebars, merchant bars, and profiles, which are used in construction and manufacturing industries; and drawn products comprise barbed and barbless fence wire, galvanized wire, fences, concrete reinforcing wire mesh, nails, and clamps for manufacturing, construction, and agricultural sectors. The company also offers specialty and stainless steel products used in tools and machinery, chains, fasteners, railroad spikes, and special coil steel, as well as special sections, such as grader blades, smelter bars, light rails, super light I-beams, and elevator guide rails. In addition, it provides flat products, such as hot and cold steel coils, heavy plates, and profiles; and resells flat steel products manufactured by other Brazilian steel producers. The company, through its interest in Dona Francisca Energetica S.A., operates hydroelectric power plant with a nominal capacity of 125 megawatts located in Agudo, Rio Grande do Sul state. It has a strategic partnership with Corporación Centroamericana del Acero S.A. The company was founded in 1901 and is headquartered in Porto Alegre, Brazil. Gerdau S.A. is a subsidiary of Metalurgica Gerdau S.A.

Market Cap (intraday)5: 19.09B

Enterprise Value (3-Oct-09): 26.22B

Trailing P/E (ttm, intraday): 32.78

Forward P/E (fye 31-Dec-10): 12.22

PEG Ratio (5 yr expected): 2.81

Price/Sales (ttm): 0.92

Price/Book (mrq): 1.79

Enterprise Value/Revenue (ttm): 1.33

Enterprise Value/EBITDA (ttm): 6.998

15-Jun-09 Deutsche Securities, Upgrade to:Hold

6-Apr-09 Deutsche Securities, Downgrade tp: Sell

6-Mar-09 JP Morgan, Downgrade to: Neutral

GOL, Gol Linhas Aereas

Gol Linhas Aereas Inteligentes S.A. provides air transportation services for passengers, cargo, and mail bags in Brazil and South America. The company operates domestic and international flights. As of April 3, 2009, it offered approximately 800 daily flights to 49 destinations connecting various cities in Brazil and 10 destinations in South America. Gol Linhas Aereas Inteligentes S.A. was founded in 2001 and is based in Sao Paulo, Brazil

Market Cap (intraday): 2.32B

Enterprise Value (3-Oct-09): 3.84B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): 12.06

PEG Ratio (5 yr expected): 0.5

Price/Sales (ttm): 0.64

Price/Book (mrq): 2.06

Enterprise Value/Revenue (ttm): 1.1

Enterprise Value/EBITDA (ttm): 15.427

25-Aug-09 Argus, Upgrade to: Buy

22-Jul-09 Credit Suisse, Upgrade to: Outperform

3-Apr-09 JP Morgan, Downgrade to:Underweight

23-Mar-09 UBS, Downgrade to: Neutral

13-Jan-09 Citigroup, Downgrade to: Sell

ITUB, Itau Unibanco

Itau Unibanco Holding S.A., together with its subsidiaries, provides various credit and other financial services to individuals, small and medium-sized companies, and large corporations in Brazil and internationally. The company’s deposit products include demand, savings, time, and other deposits. Its loan portfolio comprises commercial, real estate, lease financing, government, agricultural, and personal loans. Itau Unibanco Holding also offers fund management, portfolio management, brokerage, and custody services; credit cards; automobile, life, and property and casualty insurance products, as well as private retirement plans and capitalization plans; wholesale banking services to large corporations; consumer credit transactions and payroll advance, vehicle financing, and credit card transactions; and investment banking and advisory services. In addition, the company provides financial products, such as trade financing, loans from multilateral credit agencies, off-shore loans, international cash management services, foreign exchange, letters of credit, guarantees required in international bidding processes, derivatives for hedging or proprietary trading purposes, structured transactions, and international capital markets offerings. As of December 31, 2008, it operated 2,715 branches, 734 customer site branches, and 22,868 automated teller machines. The company was formerly known as Banco Itau Holding Financeira S.A. and changed its name to Itau Unibanco Holding S.A. in April 2009. The company was founded in 1944 and is headquartered in Sao Paulo, Brazil. Itau Unibanco Holding S.A. is a subsidiary of Itau Unibanco Participacoes S.A

Market Cap (intraday): 91.14B

Enterprise Value (3-Oct-09): 181.96B

Trailing P/E (ttm, intraday): 17.74

Forward P/E (fye 31-Dec-10) 1: 14.51

PEG Ratio (5 yr expected): 3.03

Price/Sales (ttm): 4.41

Price/Book (mrq): 3.39

Enterprise Value/Revenue (ttm): 8.95

Enterprise Value/EBITDA (ttm): N/A

NETC, Net

Net Servicos de Comunicacao SA (Net Servicos) is a multiservice holding company engaged in the pay-television and broadband Internet industries in Brazil. As of December 31, 2008, the Company had 3.2 million connected subscribers in 91 cities in Brazil, including Sao Paulo and Rio de Janeiro. The Company’s principal services include pay-television and pay-per-view programming under the NET brand name, digital cable under the NET Digital brand name, high-definition cable television combined with digital video recorder under the NET Digital HD MAX brand name, broadband Internet service under the NET Virtua brand name and fixed line telephony service under the NET Fone Via Embratel brand name. As of December 31, 2008, the Company’s advanced network of coaxial and fiber-optic cable covered over 47,000 kilometers and passed approximately 10.2 million homes. On December 29, 2008, the Company completed the acquisition of BIGTV, whereby BIGTV became a wholly owned subsidiary of Net Servicos.

Debt/Equity Ratio 0.53

Gross Margin 51.49%

Net Profit Margin 2.65%

Total Shares Outstanding 342.9M

Market Capitalization 4.15B

Earnings/Share 0.1

8-Sep-09 Barclays Capital, Initiated: Equal Weight

6-Jan-09 Citigroup, Initiated: Buy

PBR, Petrobras

Petroleo Brasileiro SA-Petrobras is an integrated oil and gas company. During the year ended December 31, 2008, the Company’s average domestic daily hydrocarbons production was 2,176 thousand barrels of oil equivalent per day (mboe/d). Approximately 84% of its proved reserves are in fields in the offshore Campos Basin. The Company operates the refining capacity in Brazil. The Company’s domestic refining capacity is 1,942 thousand barrels per day (mbbl/d). Its domestic refining production is 1,787 mbbl/d and sales of oil products to domestic markets is 1,748 mbbl/d. The Company is also involved in the production of petrochemicals and fertilizers. The Company distributes oil products through its own BR network of retailers and to wholesalers. During 2008, the Company increased its stake in the Sierra Chata and Parva Negra blocks to 45.55% and 100%, respectively, and acquired a 13.72% stake in the El Tordillo and La Tapera-Puesto Quiroga blocks.

Debt/Equity Ratio 0.44

Gross Margin 40.28%

Net Profit Margin 14.94%

Total Shares Outstanding 4.4 B

Market Capitalization 196.19 B

Earnings/Share 3.37

10-Jul-09 UBS, Upgrade to: Buy

21-May-09 Standpoint Research, Downgrade to: Hold

27-Mar-09 Deutsche Securities, Downgrade to: Hold

12-Feb-09 Citigroup, Downgrade to: Hold

PDA, Brazil Foods

BRF - Brasil Foods S.A., through its subsidiaries, engages in the production and sale of poultry, pork, beef cuts, milk, dairy products, and processed food products in Brazil and internationally. Its products include frozen whole and cut chickens, partridges, and quail; and frozen pork and beef cuts, such as loins and ribs, and whole carcasses. The company’s processed foods comprise specialty meats, including sausages, ham products, bologna, frankfurters, salamis, and bacon, as well as chicken sausages, chicken hot dogs, and chicken bologna; frozen processed poultry, beef, and pork products consisting of hamburgers, steaks, breaded meat products, kibes, and meatballs, as well as soy-based hamburgers and breaded products; and marinated and seasoned chickens, roosters, and turkeys. In addition, it offers pasteurized and UHT milk, as well as flavored milks, yogurts, fruit juices, soybean-based drinks, cheeses, and desserts; and frozen prepared entrees, which comprise lasagnas and pizzas, cheese bread, and pies and pastries, as well as frozen vegetables, such as broccoli, cauliflower, peas, French beans, French fries, and cassava fries; and margarine under Doriana, Delicata, and Claybom brand names. Further, the company produces animal feed for poultry and hogs; and a line of pet food for dogs under the Balance and Supper brands, as well as a range of soy-based products, including soy meal and refined soy flour. It sells its products under Perdigao, Chester, Batavo, Elege, and Turma da Monica brand names in Brazil; Fazenda brand in the Russian Federation; Borella brand in Saudi Arabia; and Perdix brand internationally. BRF - Brasil Foods S.A. has a strategic alliance with Unilever Brazil Ltda. to manage the Becel and Becel ProActiv brands of margarine in Brazil. The company was formerly known as Perdigao S.A. and changed its name to BRF - Brasil Foods S.A. on July 8, 2009. BRF - Brasil Foods S.A. was founded in 1900 and is headquartered in Sao Paulo, Brazil.

Market Cap (intraday)5: 9.26B

Enterprise Value (3-Oct-09): 11.10B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): 18.66

PEG Ratio (5 yr expected): 1.54

Price/Sales (ttm): 1.44

Price/Book (mrq): 2.35

Enterprise Value/Revenue (ttm): 1.74

Enterprise Value/EBITDA (ttm): 21.69

SBS, Sabesp

Companhia de Saneamento Basico do Estado de Sao Paulo provides basic and environmental sanitation services in the Greater Sao Paulo metropolitan area, Brazil. The company plans, executes, and operates water, sewage, and industrial wastewater systems. It provides water and sewage services to residential, consumer, commercial, industrial, and condominium customers, as well as small and medium-sized companies in 366 municipalities. The company also supplies water on a wholesale basis to 6 municipalities and treats sewage serving approximately 26 million people. In addition, it operates in urban rainwater drainage and management, urban cleaning and solid waste management, and power generation and energy activities markets. The company was founded in 1954 and is headquartered in Sao Paulo, Brazil.

Market Cap (intraday): 35.29M(*)

Enterprise Value (3-Oct-09): 3.27B

Trailing P/E (ttm, intraday): 0.06

Forward P/E (fye 31-Dec-10) 1: 8.02

PEG Ratio (5 yr expected): 2.22

Price/Sales (ttm): 0.01

Price/Book (mrq): 0.01

Enterprise Value/Revenue (ttm): 0.89

Enterprise Value/EBITDA (ttm): 2.109

29-Jul-09 Standpoint Research, Initiated: Buy

SID, Companhia Siderurgica Nacional

Companhia Siderurgica Nacional primarily operates as an integrated steel producer in Brazil. The company principally produces carbon steel and various steel products. Its products include slabs, which are semi-finished products used for processing hot-rolled, cold-rolled, or coated coils and sheet products; hot-rolled products that comprise heavy-gauge hot-rolled coils and sheets, and light-gauge hot-rolled coils and sheets; cold-rolled products, including cold-rolled coils and sheets; and galvanized products consisting of flat-rolled steel coated with zinc or a zinc-based alloy. The company also offers tin mill products, which consist of coated or uncoated flat-rolled low-carbon steel coils or sheets, such as low tin coated steel, tin free steel, and tin and black plate products. In addition, it owns iron ore, limestone, and dolomite mines in Minas Gerais, as well as maintains strategic investments in railroads and power supply companies. Further, the company engages in financial operations and trading, package production, cement production, trading of electricity, and investment funds, as well as the provision of maritime port services. Companhia Siderurgica Nacional sells its steel products as a raw material for various manufacturing industries, including the automotive, home appliance, packaging, construction, and steel processing industries primarily in Asia, North America, Latin America, and Europe. The company offers its products to customers directly through its sales force, as well as through distributors for subsequent resale. Companhia Siderurgica Nacional was founded in 1941 and is headquartered in Sao Paulo, Brazil.

Market Cap (intraday): 22.84B

Enterprise Value (3-Oct-09): 25.57B

Trailing P/E (ttm, intraday): 9.04

Forward P/E (fye 31-Dec-10): 13.62

PEG Ratio (5 yr expected): 1.36

Price/Sales (ttm): 3.23

Price/Book (mrq): 5.76

Enterprise Value/Revenue (ttm): 3.69

Enterprise Value/EBITDA (ttm): 9.453

TAM, Transportes Aereos Marilia

TAM S.A., through its subsidiaries, provides passenger and cargo air transportation services in Brazil and internationally. It offers flights serving various destinations in Brazil, and operates scheduled passenger and cargo air transport routes to 42 cities, as well as to 37 other domestic destinations through alliances with other airlines. The company also operates charter flights, as well as sells tourism packages and corporate events in Brazil and internationally. As of December 31, 2008, TAM operated a fleet of 129 aircrafts. It was formerly known as TAM—Companhia de Investimentos em Transportes and changed its name to TAM S.A. in September 2002. The company was founded in 1997 and is headquartered in Sao Paulo, Brazil. TAM S.A. is a subsidiary of TAM-Empreendimentos e Participacoes S.A.

Market Cap (intraday): 2.02B

Enterprise Value (3-Oct-09): 5.36B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): 9.08

PEG Ratio (5 yr expected): 0.35

Price/Sales (ttm): 0.32

Price/Book (mrq): 2.48

Enterprise Value/Revenue (ttm): 0.89

Enterprise Value/EBITDA (ttm): 8.188

29-Jul-09 Citigroup, Downgrade to: Hold

22-Jul-09 Credit Suisse, Upgrade to: Outperform

TNE, Tele Norte

Tele Norte Leste Participacoes S.A., together with its subsidiaries, provides telecommunication services primarily in Brazil. The company offers a range of integrated telecommunications services that include fixed-line and mobile telecommunications services; data transmission services, including broadband access services; and ISP services. It offers its integrated telecommunications services under the brand name ‘Oi’. The company also operates a fiber optic cable system that connects the United States, Bermuda, Brazil, and Venezuela, as well as operates an Internet portal under the brand name ‘iG’. In addition, the company offers traffic transportation services; public telephone services; and voice services. Further, it provides value-added services, including voicemail, caller ID, and other services, such as personalization, SMS subscription services, chat, mobile television, and location-based services and applications. As of December 31, 2008, the company provided satellite network that covered approximately 3,000 localities in 10 states, and offered voice and data services to approximately 4.5 million persons and approximately 650,000 terminals; mobile network consisting of 5,025 active radio base stations; and 24.4 million mobile subscribers. The company was founded in 1998 and is headquartered in Rio de Janeiro, Brazil.

Market Cap (intraday): 6.99B

Enterprise Value (3-Oct-09): 19.13B

Trailing P/E (ttm, intraday): 61.93

Forward P/E (fye 31-Dec-10) 1: 12.18

PEG Ratio (5 yr expected): N/A

Price/Sales (ttm): 0.51

Price/Book (mrq): 1.5

Enterprise Value/Revenue (ttm): 1.4

Enterprise Value/EBITDA (ttm): 5.136

4-Jun-09 Deutsche Securities Downgrade to: Hold

TSP, Telesp

Telecomunicações de São Paulo S.A. – TELESP, through its subsidiaries, provides fixed-line telecommunications services to residential and commercial customers in the state of Sao Paulo, Brazil. Its services include local services, such as installation, activation, monthly subscription, measured service, and public telephones; intraregional, interregional, and international long-distance services; data services, including broadband and other data link services; pay TV services through direct to home satellite technology and land based wireless technology multi channel multipoint distribution services; and network services, including interconnection and the leasing of facilities. The company also offers multimedia communication services, such as audio, data, voice and other sounds, images, texts, and other information; and Internet access services, as well as sells handsets and other telephone equipment. In addition, it provides interconnection services to cellular service providers and other fixed telecommunications companies, as well as interactive banking services and electronic mail services. The company offers its services through person-to-person sales, telesales, Internet, door-to-door sales, and indirect channels. As of December 31, 2008, its telephone network included approximately 11.7 million fixed lines in service, including residential, commercial, and public telephone lines, as well as served approximately 2.5 million broadband clients and 0.5 million pay TV clients. The company, formerly known as Telesp Participacoes S.A. – TelespPar, was founded in 1998 and is headquartered in Sao Paulo, Brazil. Telecomunicacoes de Sao Paulo S.A. – TELESP is a subsidiary of Telefonica S.A.

Market Cap (intraday): 12.51B

Enterprise Value (3-Oct-09): 13.85B

Trailing P/E (ttm, intraday): 9.55

Forward P/E (fye 31-Dec-10): 10.22

PEG Ratio (5 yr expected): 54.75

Price/Sales (ttm): 1.37

Price/Book (mrq): 2.07

Enterprise Value/Revenue (ttm): 1.53

Enterprise Value/EBITDA (ttm): 3.922

8-Sep-09 Barclays Capital, Initiated: Underweight

13-May-09 Oscar Gruss,, Downgrade to: Hold

5-Feb-09 HSBC Securities, Upgrade to: Overweight

6-Jan-09 Citigroup, Initiated: Sell

TSU, Tim

TIM Participacoes S.A., through its subsidiaries, provides mobile telecommunications services primarily using global system for mobile communication technology in Brazil. The company provides various prepaid plans and long distance services, as well as offers various value-added services, including short message services or text messaging, multimedia messaging services, push-mail, video call, turbo mail, WAP downloads, Web browsing, business data solutions, songs, games, TV access, voice mail, conference calling, chats, and other content and services. In addition, TIM Participacoes provides interconnection services to fixed line and mobile service providers. Further, it offers co-billing services to other telecommunication service providers; sells a range of mobile handsets through its dealer network, which includes its own stores, exclusive franchises, authorized dealers, and department stores. TIM Participacoes was formerly known as Tele Celular Sul Participações S.A. and changed its name to TIM Participacoes S.A. in August 2004. The company was founded in 1998 and is headquartered in Rio de Janeiro, Brazil. TIM Participacoes S.A. is a subsidiary of TIM Brasil Serviços e Participações S.A.

Market Cap (intraday): 5.83M

Enterprise Value (3-Oct-09): 1.58B

Trailing P/E (ttm, intraday): 0.05

Forward P/E (fye 31-Dec-10): 20.41

PEG Ratio (5 yr expected): 6.33

Price/Sales (ttm): 0

Price/Book (mrq): 0

Enterprise Value/Revenue (ttm): 0.21

Enterprise Value/EBITDA (ttm): 0.889

8-Sep-09 Barclays Capital, Initiated: Equal Weight

6-Aug-09 Oscar Gruss, Upgrade to: Hold

24-Jul-09 JP Morgan, Upgrade to: Neutral

7-May-09 Oscar Gruss, Downgrade to: Reduce

UGP, Ultrapar

Ultrapar Holdings Inc., through its subsidiaries, engages in the distribution of liquefied petroleum gas, and light fuel and lubricants. The company sells bottled and bulk LPG to residential, commercial, and industrial markets directly, as well as through its retail stores and independent dealers; and distributes gasoline, ethanol, diesel, NGV, fuel oil, kerosene, and lubricants directly, as well as through a network of approximately 3,469 service stations. It also engages in the production and sale of chemicals and petrochemical products, such as ethylene oxide, ethylene glycols, ethanolamines, glycol ethers, and methyl-ethyl-ketone, as well as specialty chemicals that are used in detergents, crop protection chemicals, cosmetics, foods, textiles, leather, oil field chemicals, packaging, paints, and varnishes. In addition, the company offers integrated logistics services for special bulk cargo; and storage for liquid bulk in South America, as well as provides multimodal transportation, ship loading and unloading, operation of pipelines, logistics programming, and installation engineering services. As of December 31, 2008, it operated a fleet of approximately 580 trucks. Further, the company involves in petroleum refining business. It sells its products in Brazil, Latin America, the Far East, Europe, and North America. The company was founded in 1937 and is headquartered in Sao Paulo, Brazil.

Market Cap (intraday): 5.31B

Enterprise Value (3-Oct-09): 6.64B

Trailing P/E (ttm, intraday): 25.76

Forward P/E (fye 31-Dec-10): 15.8

PEG Ratio (5 yr expected): 1.28

Price/Sales (ttm): 0.3

Price/Book (mrq): 1.93

Enterprise Value/Revenue (ttm): 0.38

Enterprise Value/EBITDA (ttm): 9.891

VALE, Vale

Companhia Vale do Rio Doce, through its subsidiaries, operates as a diversified metals and mining company worldwide. The company produces iron ore and iron ore pellets, nickel, manganese ore, ferroalloys, and kaolin. It also engages in producing bauxite, alumina, aluminum, copper, metallurgical and thermal coal, metallurgical coke and methanol, cobalt, potash, and other non-ferrous minerals, as well as precious metals, including platinum-group metals, gold, and silver. In addition, the company operates logistics systems in Brazil, including railroads, maritime terminals, and a port. Further, it engages in hydroelectric power generation and steel production. The company was founded in 1942 and is headquartered in Rio de Janeiro, Brazil.

Market Cap (intraday): 119.47B

Enterprise Value (3-Oct-09): 132.96B

Trailing P/E (ttm, intraday): 14.92

Forward P/E (fye 31-Dec-10): 15.28

PEG Ratio (5 yr expected): 111.25

Price/Sales (ttm): 3.36

Price/Book (mrq): 2.19

Enterprise Value/Revenue (ttm): 3.85

Enterprise Value/EBITDA (ttm): 8.966

25-Aug-09 HSBC Securities, Downgrade to: Underweight

4-Aug-09 Dahlman Rose, Upgrade to: Buy

12-Jun-09 BMO Capital Markets, Downgrade to: Market Perform

21-May-09 Dahlman Rose, Initiated: Hold

VCP, Votorantim

Note that VCP is merging with ARA creasting a new company called Fibria. Votorantim Celulose e Papel S.A., together with its subsidiaries, engages in the manufacture and marketing of pulp and paper products in North America, Latin America, Europe, and Asia/the Middle East/Oceania/Africa. The company’s product portfolio includes bleached eucalyptus kraft pulp, such as hardwood pulp. Its pulp products are used to manufacture a range of printing and writing paper products, including coated and uncoated printing and writing papers, thermal papers, carbonless papers, and other specialty papers. In addition, Votorantim Celulose involves in the distribution of graphic papers and products. The company was formerly known as Indústrias de Papel Simão S.A. and changed its name to Votorantim Celulose e Papel S.A. in January 1995. Votorantim Celulose e Papel S.A. is based in São Paulo, Brazil. The company operates as a subsidiary of Votorantim Participacoes S.A

Market Cap (intraday): 6.57B

Enterprise Value (3-Oct-09): 11.98B

Trailing P/E (ttm, intraday): N/A

Forward P/E (fye 31-Dec-10): 10.99

PEG Ratio (5 yr expected): 0.19

Price/Sales (ttm): 2.54

Price/Book (mrq): 1.33

Enterprise Value/Revenue (ttm): 4.73

Enterprise Value/EBITDA (ttm): 17.992

17-Jun-09 BMO Capital Markets, Upgrade to: Market Perform

10-Jun-09 Citigroup, Downgrade to: Sell

2-Jun-09 BMO Capital Markets, Downgrade to: Underperform

12-May-09 BMO Capital Markets, Downgrade to: Market Perform

5-Feb-09 BMO Capital Markets, Upgrade to: Market Perform

21-Jan-09 BMO Capital Markets, Downgrade to: Underperform

16-Jan-09 Deutsche Securities, Downgrade to: Hold

15-Jan-09 UBS, Downgrade to: Sell

VIV, Vivo

Vivo Participacoes S.A., through its subsidiaries, provides cellular telecommunications services in Brazil. It provides voice and ancillary services, including voicemail and voicemail notification, call forwarding, three-way calling, caller identification, short messaging, limitation on the number of used minutes, cellular chat room, and data service, such as wireless application protocol service. It also offers direct access to the Internet through Data cards, as well as provides multimedia message service and mobile execution environment, which enables the wireless devices to download applications and execute them on the mobile with a user interface that contains icons on the wireless device to identify the services, such as voice mail, downloads, and text messaging. In addition, the company offers roaming services through agreements with local cellular service providers in Brazil and other countries that allow its subscribers to make and receive calls while out of its concession areas; and interactivity services with radio and television providers. Further, it sells WCDMA GSM handsets and broadband cards compatible with WCDMA and CDMA EVDO technology. The company offers its products and services through its own stores, dealers, lottery shops, physical and online card distributors, drugstores, newspaper stands, book stores, bakeries, gas stations, bars, and restaurants. As of December 31, 2008, it operated 331 sales outlets in Brazil. Vivo Participacoes S.A. was formerly known as Telesp Celular Participacoes S.A. The company was founded in 1998 and is based in Sao Paulo, Brazil.

Market Cap (intraday): 9.77B

Enterprise Value (3-Oct-09): 12.46B

Trailing P/E (ttm, intraday): 26.52

Forward P/E (fye 31-Dec-10): 16.06

PEG Ratio (5 yr expected): 0.52

Price/Sales (ttm): 1.02

Price/Book (mrq): 1.94

Enterprise Value/Revenue (ttm): 1.36

Enterprise Value/EBITDA (ttm): 4.308

8-Sep-09 Barclays Capital, Initiated: Underweight

8-Jul-09 UBS, Upgrade to: Buy

EWZ Brazil ETF

Description: "The investment seeks to provide investment results that correspond generally to the price and yield performance of publicly traded securities in the Brazilian market, as measured by the MSCI Brazil index. The fund normally invests at least 95% of assets in the securities of its underlying index and in ADRs based on the securities in its underlying index. It uses a representative sampling strategy to try to track the index. The index consists of stocks traded primarily on the Bolsa de Valores de So Paulo. It is nondiversified".

The Brazil ETF top holdings' are all described above:

Petroleo Brasileiro SA (Preference) 12.05%

PETROBRAS -ON EJ 10.75%

VALE -PNA N1 8.67%

Itau Unibanco Banco Multiplo 7.87%

VALE S.A. ADS 6.47%

BRADESCO -PN ED N1 4.83%

Gerdau SA 3.61%

Ambev Cia De Bebid Pfd 2.95%

Cia Siderurgica Belgo-Mineira 2.77%

OGX PETROLEO-ON NM 2.26%

BZF, Brazilian Real ETF (Currency):

Decrition: "The investment seeks to achieve total returns reflective of both money market rates in Brazil available to foreign investors and changes in value of the Brazilian Real relative to the U.S. dollar. The fund normally invests in a combination of U.S. money market securities with forward currency contracts and currency swaps which are designed to create a position economically similar to a money market security denominated in Brazilian Real. The average portfolio maturity is 90 days or less. It does not purchase any money market securities with a remaining maturity of more than 397 calendar days. The fund is nondiversified."

Best,

The Shocked Investor was originally on a mission to uncover the dark truth about whether my money, and your money, had been invested in worthless asset-backed commercial papers. Since then his blog www.shockedinvestor.blogspot.com has taken a life of its own and discusses many other topics. He has over 20 years of investing experience and knows the Brazilian market well as he lived in the country for over 15 years.

Can I just say what a aid to search out someone who actually is aware of what theyre speaking about on the internet. You definitely know the best way to bring an issue to mild and make it important. More folks must read this and understand this aspect of the story. I cant imagine youre no more fashionable since you positively have the gift.

Great analysis on Brazalian stocks. Keep up the good work.

Looking forward for more analysis like this for other emerging markets like Russia, India, etc.

All well & good but a little late to thair party. that market

is way up from where any dood risk buying aera is. Al

Thank you very much for the comments.

I added an article on Braskem, which has signed a deal with Johnson and Johnson for the use of 'green' plastic in their Sundown products. The plastic, green polyethylene, is made of sugar cane, and is as good as that made of oil. It has the same appearance and properties of traditional plastics". And in the process, it captures CO2 from the atmosphere. BAK has gone up 182% this year. If you had never heard of it, the company has a market cap of $7B, and had annual sales of $9.4B. Artcile: http://shockedinvestor.blogspot.com/2009/10/braskem-signs-major-deal-to-sell-green.html

For anyone interested, I also have a site that tracks live all Latin-American ADRs: http://nexalogic.com/latin.html

I have an article coming up on BRF as well.

As for the stocks being frothy, I concur. If there is a pullback on the USD, watch out. Currencies are a mess at the moment.

Hi, Thanks for sharing this informative article. Your article is very useful. Data you have provided is very important.

Thank you.

Ditto on excellent article. Here is the question. With many of the stocks already at 90-170% since Mar and the news of the Olympics already digested. It would seem the contrarian move right now would be to either wait for a pullback or if more risky to short the highest runners. Any thoughts.

I have been in EWZ for some time and so bought at the high almost and rode it to the low and back again.

Loved the report, and it's spot on.

Here's a small example.........

BOUGHT: VIVAW 07/10/2009 3.40 SOLD: 08/07/2009 7.00

VIVJX 08/10/2009 2.50 10/02/2009 3.50

That is the power of options !!!!!!!

Keep up the Great Work !!!!

Adam,

I'm amazed! Thank you for getting this info out in one place. It will be a great help in our decision making. Thanks, too, to Kenny and Raul.

Congratulations! to kenny and adam. .david , from mexico city. so,something like autralia,cut be next?

Excellent breakdown of the companies. Its unfortunate that more retailers don't have ADRs yet, but you clearly demonstrate the excellent selection of companies out there.

BRF has a wider spread of smaller companies than EWZ, which is heavily geared toward VALE, PBR, the banks, and ABV.

ACO

Excellant study...........almost too much to digest on one reading.

THX, Gerryb

Excellent. Santander just IPO'ed down there today, new symbol BSBR as an ADR on the NYSE.

Wonderful article. Of these PBR and VALE are the best !

What a study of Brazil market!! Great work.

Adam, do you incorporate such thorough study when you generate triangles on charts?