Now that 2014 is officially over, it is a good time to review your portfolio's performance. Whether you are a stock picker, day trader, mutual fund investor, commodities or currency guru; understanding how much you made or lost in the markets during the year is extremely important. But, just knowing whether or not you made money isn't enough; you need to know whether or not you outperformed the market itself or else all the time and money you spent researching, buy and selling, or paying an advisor was simply a waste.

In order to determine whether your complicating things and throwing money away you should be comparing your total portfolio returns to that of a specific index such as the S&P 500 or more specifically the SPDR S&P 500 ETF (SPY). By using the SPDR S&P 500 ETF as a benchmark, you can determine whether you beat or were beaten by the market. This information will then allow you to make a better financial decision about how and with whom you invest your money moving forward.

Let's get started

First let's start with how your portfolio performed? To get total portfolio return you need to calculate if your investments increased or decreased. Take all the individual stocks, bonds, mutual funds ETF's you own, add up the total value of the investments at the start of 2014 and subtract that by what they were worth at the end of the year. (That figure should include all dividends, capital gains from investments sold.) For example, if you started with $90,000 in investable assets on January 1, 2014 and on December 31, 2014 those assets were worth $104,500. Therefore the return would have been $14,500 for the year or a 16.1%.

Now compare that number with the SPDR S&P 500 ETF which rose 11.4% in 2014 pre-dividend or 13.27% with dividends calculated into the total return. The example above certainly would have beaten the SPDR S&P 500 ETF, meaning you didn’t waste time or money during 2014.

But, once you have your total return, determine what it costs you to make that return. Find all the fees and commissions you paid during the year. What did each trade cost you to make, most online brokerage accounts will charge you around $7.99 per trade. In addition to that, you want to be looking for fee's any that mutual funds or ETF's you own charged you for the year, again these will usually range from 0.1% to as high at 1.5% in most cases. In some cases you will not see the fees on a line item, and if you beat the market, than it’s a mood point since you paid for performance and received it. But, if you lost out to the market, than not only did you pay higher fees and commissions than you would have if you had simply purchased the SPDR S&P 500 ETF, which would have only cost you one commission of $7.99 when you purchased it and an annual fee of just 0.09%, but you wasted the opportunity of increasing your total portfolio and net worth.

The Power of Compounding Interest

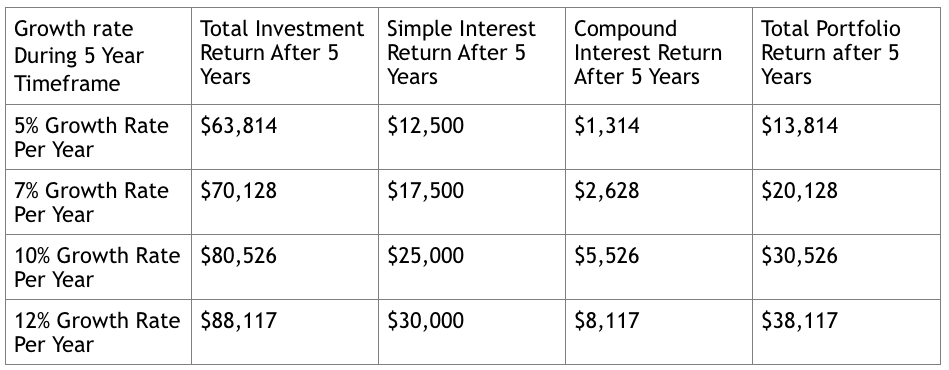

Now you may be thinking that a percentage point here and there doesn’t matter that much, but when you consider compounding returns over a long period of time, one or two percent can make a massive difference in total portfolio performance over a period of as little as five years.

The table below explains the difference just a few percent per year can make. The example is of a portfolio which started with $50,000 and no additional outside money was added to the account during the five years.

Figures based on Authors Calculations and simply for illustrational purposes

The difference in return between 10% and 12% over five years is more than $8,000, a rather large number. But, if we run this test out for a longer period of time, 20 years for example, the difference in returns of just 10% to 12% is mind blowing. Using the same number as above, $50,000 initial investment without adding new money during the 20 years a 10% return would grow to $336,375, with $186,375 of that being compounded interest. But when your investment grows at 12%, the total return becomes $482,315 and compounded interest is now $312,315. Just that 2% return would cause your money to grow by more than $100,000 over 20 years.

Final Thoughts

"So did you beat the market in 2014?"

If you did, congratulations! If you didn’t, you should be asking "why?" Then after figuring out your why, poor performance, high fees, whatever it may be, then determine if you could be getting a better return by simply buying and holding a S&P 500 index ETF.

Matt Thalman

INO.com Contributor - ETFs

Disclosure: This contributor has no positions in any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.