By: Max D. - Max is a technical writer who regularly contributes financial topics to Farnsfield Research, and other investing blogs. Max spends his time running multiple companies in the financial sector. This allows him to have a constant finger on the pulse of the industry.

As millions of Americans file their income taxes prior to the April 15, 2015 deadline, traders must face the decision of how to report capital gains or loss according to IRS specifications. In the world of the New York Stock Exchange, a single trade, which may involve any number of stocks, can represent thousands of dollars. To reap the greatest amount of financial benefit from the passage of the Commodities Futures Modernization Act of 2000 and reduced tax rates of capital gains and losses, traders must understand how to properly report these securities and commodities on their tax return.

The Commodities Futures Modernization Act of 2000

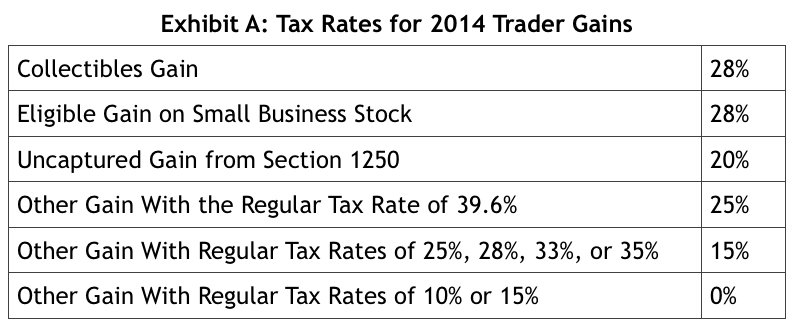

Following practices of purchasing and selling single security futures far in advance of routine business, the U.S. Congress enacted the Commodities Futures Act of 2000. Although the law expands over the course of 50+ pages, it affects securities futures and commodities futures in one unique way. If 10 or more securities or indices are grouped together, the entire grouping becomes a commodity--indices are one of the primary alternative investment strategies used by investors today, resulting in a lower tax rate. However, nine or fewer securities incur the traditional tax rates as shown in Exhibit A, located under Tax Rates for 2014.

Tax Rates for 2014

Independent of income earned through extraneous sources, such as employment or contractual work, the IRS sets a specific tax rate on capital gains, which includes gains from the sale of securities futures through mark-to-market accounting, when used in conjunction with "loss insurance," as well as commodities. Commodities futures gains have the option of splitting the gain into a 60% long-term rate at 15% or 40% at the routine short-term rate of 35% (maximum), which enables a trader to have a significant tax reduction for lower capital gains.

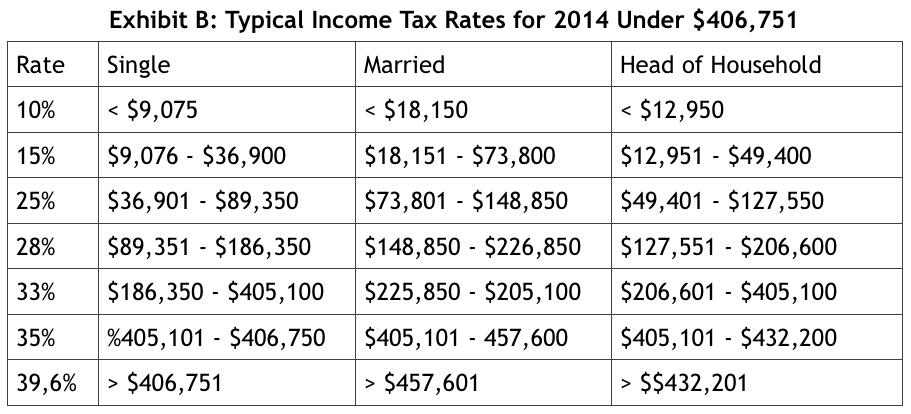

The above tax rates apply to the resulting capital gains of 60% of the long-term gain and 40% of the short-term gain amounts of commodities, which were included following the introduction of the Commodities Futures Modernization Act. Any gains from the sale of securities futures, which traders must figure according to Exhibit B, will be needed in order to determine the actual tax rate presented within Exhibit A.

By reviewing the applicable tax category that a traders total gains, if they were all reported as securities gains only, he or she will be able to identify the best ways to move these respective securities futures trades into commodities futures, which will enable the trader to take advantage of the tax rates in Exhibit A.

Key Points to Remember

> Tax rates for commodities futures are significantly less than gains from securities futures.

> The tax rate for income above $406,751 (when filing as "single") is nearly 40%.

> Traders have the potential to lower tax rates to 28%, at least, by choosing to trade a minimum of 10 securities futures, which moves the trade into a commodities category.

> Scenario: A trader makes $600,000 on the sale of 10 securities. The normal tax rate on this amount would have been $196,644.32. The single saving incurred by using a commodities futures tax break would have broken down to $15914.85.

Sources (table & data)

http://www.irs.gov/publications/p550/ch04.html#en_US_2013_publink100010737

http://www.irs.gov/publications/p550/ch04.html#en_US_2013_publink100010326

http://www.irs.gov/publications/p583/index.html