The UK economy, it seems, has been a study in opposites. It has swung from having been the fastest to the slowest, from experiencing high growth and then sluggishness, from moving from a high inflation environment to a low inflation environment. The UK economy is the great dichotomy, comprised of fading expectations and the bursting of optimistic sentiment that together carves the path of the Pound Sterling, a path that is as shaky now as it ever was and which, it seems, has been broken just this week.

Sterling Not Coming Back?

Looking at the chart below, we can tell much about the governing dynamics of Sterling buyers and sellers. Dips in the Sterling trade vs the Dollar were plentiful; back in 2009, when the crisis was at its climax, back in 2010, when UK growth was pegged as just “sluggish,” and then back in 2013, when it seemed the UK economy had finally lost all steam. Yet each and every time Sterling buyers emerged; in fact, not only did they emerge and crowd back into what they deemed an undervalued currency, but each time they emerged at a higher point, painting a picture of a fragile but steadily ascending path for the Pound vs the Dollar. Yet as the latest point on the chart shows, at this point in time the buyers have not re-emerged, letting the Pound break its ascending path. Why, this time in particular, are Sterling buyers not coming back?

Source: Netdania.com

BoE Turns Dovish

Until this week, it had appeared that the Pound Sterling might still have had some potential for a rebound; UK growth was still rather firm, unemployment was falling and wages were growing, which meant that there was still the chance of a sudden uptick in inflation that could eventually allow for a Sterling comeback. It is those expectations that kept the currency afloat, at least to some degree. But it was the Bank of England’s Governor, Mark Carney, who eventually broke Sterling’s back and spooked buyers. The Governor had reiterated that the next move in rates would probably be to the upside and that, thus far, there were no signs that UK shoppers were postponing purchases which would have ruled out a severe deflationary circle. Despite those “assurances,” the BoE Governor had predicted that UK inflation would run close to 0% for most of the year and that, in a sense, put the last nail into the coffin for a rate hike for 2015. Given the probability that a BoE rate hike won’t be forthcoming this year while a Federal Reserve rate hike more than likely is, the divergence is simply too great for Sterling buyers to bear and it has left their collective spirits “broken,” with little hope of any bounce.

Not Just About Oil

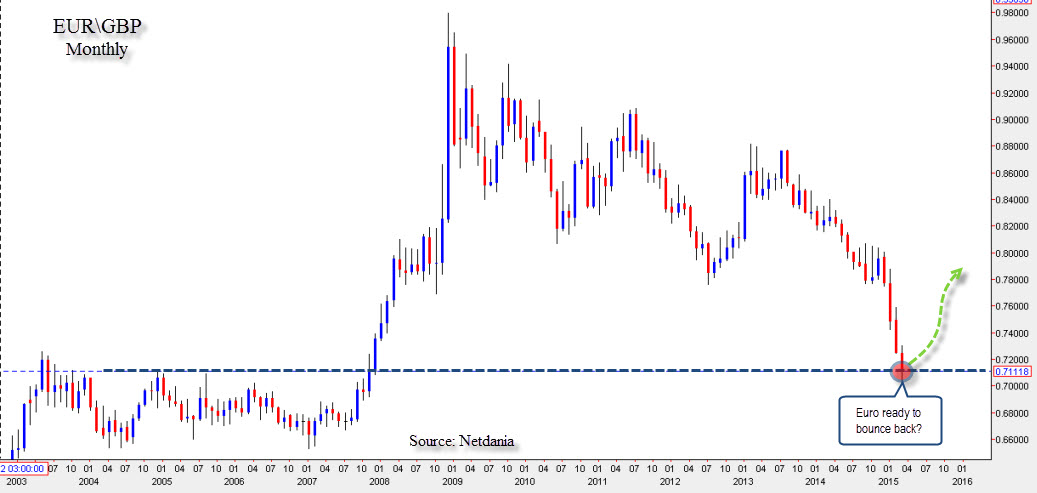

So what broke the Sterling? What caused inflation to slide? Some analysts would point out that the plunge in inflation is a global phenomenon, largely due to the collapse in Oil prices which, as of late, have closed below $50 a barrel. Yet, when it comes to the UK there is one more factor and it is related, ironically, not to Sterling’s weakness but to Sterling’s strength. As the EUR/GBP chart shows below while Sterling was soft against the Dollar it was surging against the Euro, by 15.58% to be exact. What does this have to do with the UK’s inflation? The bulk of imports coming to UK are imported from the Eurozone, and as Sterling has surged vs the Euro, the UK is effectively importing at much lower prices. This means, essentially, that the UK is literally “importing” deflation (which is falling inflation). In the same way a country can import inflation from abroad it can also import deflation; it is, ironically, this deflation which had lead the BoE to postpone its decision to raise interest rates.

Source: Netdania.com

Sterling Beaten, Not Broken

While the Sterling has certainly taken a hard hit this week, there are several things to take note. The first is that March is not over; with Unemployment and Inflation data due out within the next two weeks expectations of a rate hike do still exist. Granted, while a rate hike would likely not be as imminent as June it could still happen later in 2015, say, December, provided the data supports one; i.e. if unemployment falls below 5.7%, if wage growth accelerates, and if core inflation continues to tick up. The second, of course, are the external factors. If the Euro begins to climb a bit higher after being hit so hard, deflationary pressures could stabilize and leave space for an upward surprise to UK inflation, presuming (again) that unemployment falls, wages grow and core inflation holds, all of which means that Sterling buyers could come back. Yet one must not delude oneself; Sterling is as close now to breaking its ascending path as it has been in nearly six years, yet with two weeks still to go in March surprises could await. Therefore, only once March ends, with all the data in and the charts read, will it be a time to decide whether or not Sterling has been broken, or just beaten, and if the Pound Sterling is poised to collapse to its 2009 lows or is on the cusp of yet another rebound, all of which will eventually be told by the charts.

Look for my post next week.

Best,

Lior Alkalay

INO.com Contributor - Forex

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.