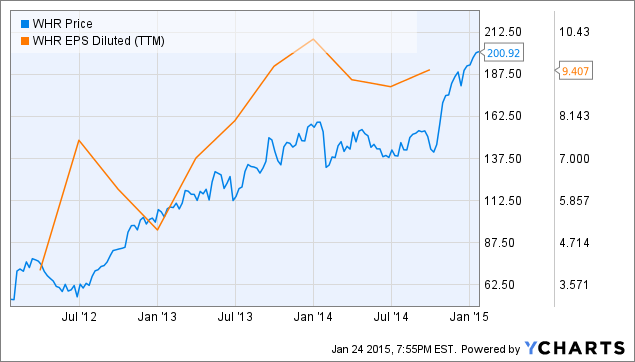

On January 12th, shares of Whirlpool Corp. (NYSE:WHR) crossed the $200/sh threshold for the first time ever. Now trading at $200.92/sh, the stock has risen by 44% in the last 4 months.

Chart courtesy of YCharts.com.

The rapid price rise is nothing new; Whirlpool’s stock is in the midst of an extended run of robust performance. Over the last 3 years, WHR has increased almost four-fold, climbing by 277% since being quoted at $53.33/sh on January 23rd, 2012. During that same period, the company’s earnings expanded by 137% to their current level of $9.41/sh.

Looking at these numbers alone, one might assume that the stock is due for a correction. Has its price climbed too quickly? Is the stock overvalued? I’d argue that WHR remains undervalued, and that investors can expect the stock to continue outperforming the market with ease.

Chart courtesy of YCharts.com.

With a P/E ratio of 21.4, the company’s earnings multiplier currently sits near its 10-year high point (see chart above). While this would typically imply that a stock is overvalued, Whirlpool’s rapid earnings growth makes it an exception. With YOY earnings growth projected to be 29% next year, Whirlpool has a forward P/E ratio of just 14, which lies near the midpoint of its long-term historical P/E range.

Additionally, with annual EPS growth projected to be 23% in the next 5 years, WHR has a PEG ratio of just 0.94. It’s an extreme rarity for a blue chip stock with a dominant market share in its respective industry to be trading at a PEG ratio below 1. To the delight of investors who think they’ve “missed out” on WHR’s large returns these past couple of years, its minuscule PEG ratio bears proof that the stock is still a strong buying opportunity. For a company of Whirlpool’s size ($15.6B market cap) and stature, its growth-based valuation tends to be the most accurate indicator of future price performance.

Assuming the company’s bottom line sustains the high level of growth that it’s projected to, Whirlpool’s shareholders are due to continue collecting a high return on their investment in the coming years. Furthermore, the company pays a quarterly dividend of $0.75/sh, or $3.00/sh on an annual basis. At the stock’s current price, this represents an annual dividend yield of 1.4%. Although the yield isn’t anything to write home about, it represents a guaranteed 1.4% cash return in addition to whatever gains the stock’s quickly-climbing price generates.

Why have earnings been growing so quickly?

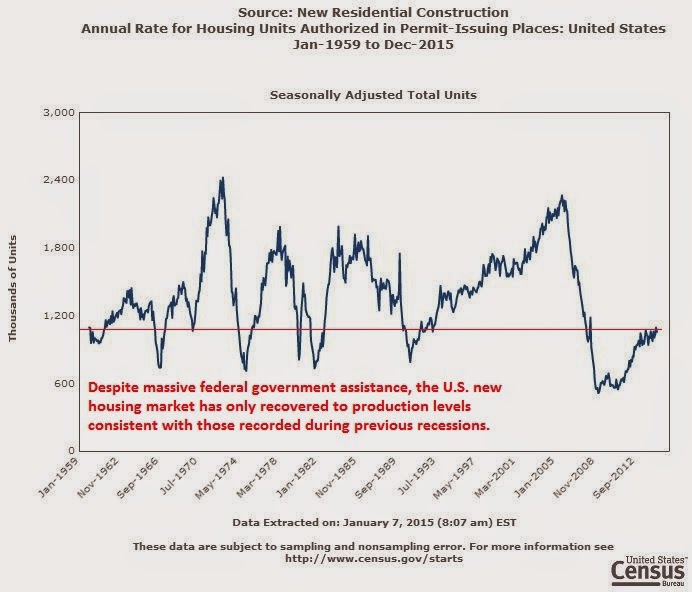

The majority (about half) of Whirlpool’s customer base is in the U.S., where the amount of newly built homes has increased rather quickly over the last 5 years.

Chart courtesy of the United States Census Bureau.

As you can see in the graph above, the amount of newly built houses has just about doubled from when the market hit its low point just a few years ago. This has been the largest contributing factor that’s propelling the company’s bottom line growth. Whirlpool is the world’s #1 home appliance maker, and all those newly built homes need to be filled with appliances. Naturally, this has created a lot of demand for the company’s products.

Whirlpool’s customer base has also enjoyed an increase in purchasing power. The low-interest rate environment has allowed people to finance their home purchases cheaply, thereby giving them excess capital to spend on home appliance purchases. Furthermore, the cheap price of oil has freed up capital in household budgets across the country, allowing consumers to allocate more capital towards home appliance purchases. Whirlpool will continue to be a large beneficiary of the pervading economic environment, so long as interest rates and oil prices remain low.

I expect those factors to continue in the coming years, namely the zero percent interest rate policy. Regardless of what the Fed has been “hinting,” the very fact that our central bank has hinted at a future rise in interest rates is a strong indicator that it won’t happen any time soon. Interest rates haven’t risen in over 8 years. In my view, any talk of the Fed’s “plans” is just a cop out to continue what they’ve been doing, without receiving any scrutiny for the long-term implications of continuing the zero percent interest rate policy indefinitely. After all, they are “planning” on raising them, right? Well, if they actually wanted to do it, they would’ve done it already. So it only seems logical that it’s here to stay.

With that said, I expect the bullish projections for Whirlpool’s earnings growth to be accurate. Over the last 3 years, Whirlpool’s EPS has swelled by 137%, or 33% annually. Going forward, the company has set ambitious expectations for its bottom line growth, targeting earnings per share to double by 2018. This represents an annual EPS growth rate of 19% over a 4-year period.

Conclusion

At a time when companies are returning more cash to shareholders – through stock buybacks and dividend payments – than ever before, Whirlpool is one of the few blue chips that’s actually reinvesting the bulk of its earnings into its business. This bodes extremely well for achieving sustainable growth in the long-term. I consider WHR to be one of the better opportunities on the market to go long on. For those who do so, considering how quickly the stock has risen lately, I recommend dollar cost-averaging your shares in order to hedge for the risk of any short-term corrections.

William Cikos

INO.com Contributor - Equities

Disclosure: This contributor has no positions in any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.