By: Josh Sparrow of Street Authority

The name Bill Ackman carries more weight now than it did a year ago.

2014 was a rough year for most hedge fund managers. The average fund returned just 2% and the first six months of the year saw 461 hedge funds close shop.

Yet Ackman's fund, Pershing Square Holdings, returned an astounding 40.4% in 2014 and went from managing around $11.5 billion assets at the start of the year to more than $18 billion currently.

Ackman was named top dog in Bloomberg's 2014 ranking of the world's best hedge fund managers.

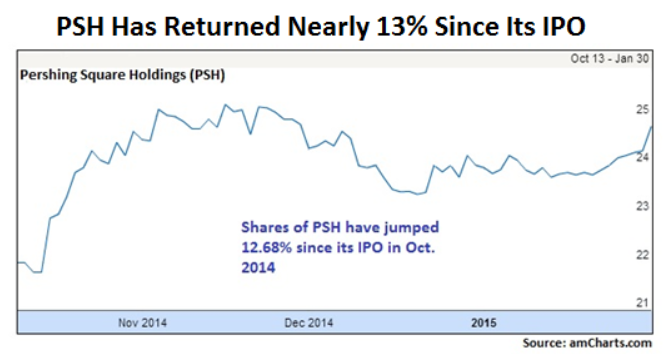

And that success helped make Pershing Square Holdings' (AMS: PSH) recent IPO that much more successful. The firm's October IPO -- which opened on the Euronext Amsterdam exchange -- was one of Europe's largest in 2014, at $2.7 billion.

Investors who bought shares of the company at the time of its IPO have already seen a nice 12.7% gain in just a few months.

In the company's first letter-to-shareholders, Ackman laid out what he believes to be the company's primary competitive advantages. He wrote, "When compared with other investment holding or operating companies, PSH benefits by its favorable tax structure and long-term track record."

Pershing Square operates out of Guernsey, a small island located off the coast of France. There, the company is "not exposed entity-level taxation." This is a big advantage as the company is able to bypass a 35% profit-tax imposed on many U.S. corporations.

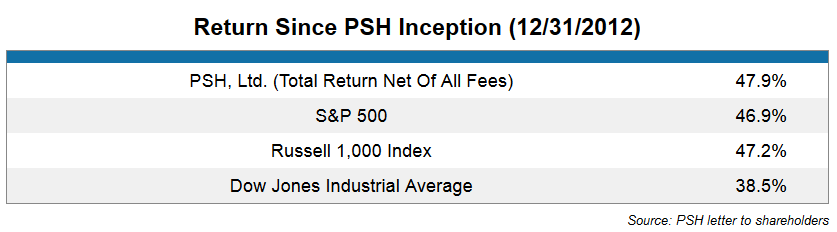

As for its track record, PSH has certainly earned its stripes -- especially when compared to major U.S. indices

As you may know, the average investor can't invest directly into a hedge fund. So when you take into account Pershing Square's unique position -- and the fact that the firm trades at a 10% discount to book value -- it's no wonder Bill Ackman believes his firm's stock is the markets "best kept secret."

But while the stock's recent performance may be an enticing factor for some investors, the difficulty to invest on foreign exchanges without racking up major fees could be enough to detract many others. Still, if you fall into this latter category, then that doesn't mean you can't profit from PSH's success.

Looking into the company's holdings can lead you to some alternative investments to help boost your own portfolio.

Here are my three favorites from Ackman's portfolio:

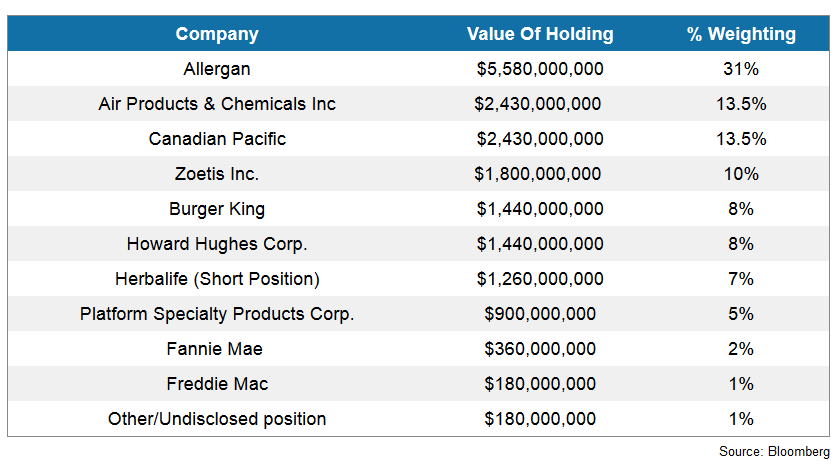

Air Products Chemicals, Inc. (NYSE: APD)

APD owns the only major hydrogen pipeline in the Canadian oil sands and supplies hydrogen to 90% of the U.S. Gulf Coast refiners, putting it in the perfect position to profit from any future North American oil and gas production.

The $34.1 billion company has grown its revenues four out of the last five years, generating $10.4 billion in sales during its 2014 fiscal year. And net margins are at roughly 26% -- more than 50% higher than the industry average.

For income investors, APD also boasts a strong 65.8% payout ratio, having shelled out nearly $630 million in dividends in 2014.

These factors combined have all helped contribute to the company's near 41% return over the last year.

Zoetis, Inc. (NYSE: ZTS)

Zoetis, a global leader in the animal healthcare industry, spun off from its parent company, Pfizer, in 2013. Since then, the $21.6 billion company has earned a near 20% market share in its industry, giving it a wide moat over its competition.

These days, it is common for pet owners to view their animal companions as members of the family. And these strong bonds help drastically increase the amount of money owners are willing to spend on pet healthcare costs.

Zoetis increased both revenue and profit margins every year since being founded in 2009. Revenue over the trailing twelve months is $4.7 billion, a 71% increase in five years. While net margins are 11.9% over the same period -- nearly three-times higher than the industry average.

That's helped the firm deliver a 39% gain to investors since its spin-off, including a 42.4% jump in the last year alone.

Canadian Pacific Railway Ltd (NYSE: CP)

It may seem like an odd time to look at Canadian Pacific. The railroad company operating roughly 14,800 miles of track across Canada and the Midwestern United States has seen its stock take a hit recently with the plunge in oil prices.

The company's share price is currently down 11% over the last three months. But as Ackman noted, the recent pullback created a unique buying opportunity for investors.

CP now trades at a 21.7 price-to-earnings ratio, which is less than the industry average of 23.4. Revenue for Q4 2014 came in around $1.6 billion, on pace with the three quarters prior.

CP has been on a tear since hiring a new CEO in 2012, delivering a 59% return to shareholders. Once oil prices inevitably start to tick back up, CP investors should see the stock return to form. And now is a great time to buy shares at a discount.

Risks To Consider: Investing in a hedge fund like PSH can be inherently risky due to the overall nature of the business.

Action To Take -- For investors with a high risk tolerance, PSH has performed well since its IPO and trades on a European exchange where a weaker Euro may help bolster the stock's value. Alternatively, APD, ZTS and CP each offer investors a unique way to take advantage of PSH's success without committing to the risk and hassle of investing in a hedge fund being traded on a foreign exchange

In the past year, Street Authority recommendations on individual stocks have gained +72%, +26% and +60% all in less than six months... and recently, their trades could have made you +26% in 42 days and +42% in less than one month. Click here to get the free trading advisory -- Trade of the Week.