Leveraging covered call options in opportunistic scenarios may augment overall portfolio returns while mitigating risk. Options are a form of derivative trading that traders can utilize in order to initiate a short or long position via the sale or purchase of contracts. In the event of a covered call, this is accomplished by leveraging the shares one currently owns by selling a call contract against those shares for a premium. Traders may also initiate a short or long position via the purchase of option contracts to the underlying security. An option is a contract which gives the buyer of the contract the right, but not the obligation, to buy or sell an underlying security at a specified price on or before a specified date. The seller has the obligation to buy or sell the underlying security if the buyer exercises the option. An option that gives the owner the right to buy the security at a specific price is referred to as a call (bullish); an option that gives the right of the owner to sell the security at a specific price is referred to as a put (bearish). I will provide an overview of how a covered call is utilized and executed. Further details focusing on optimizing stock leverage (covered calls) and the ability to sell these types of options in a conservative way to generate cash in one’s portfolio will follow.

A few characteristics to keep in mind for covered call options trading

1. Strike Price: Price at which you can buy the stock (buyer of the call option) or the price at which you must sell the stock (seller of call option).

2. Expiration Date: Date on which the option expires

3. Premium: Price one pays when he/she buys an option and the price one receives when he/she sells an option.

4. Time Premium: The further out the contract expires, the greater the premium one will have to pay in order to secure a given strike price. The greater the volatility, the greater the time premium.

5. Intrinsic Value: The value of the underlying security on the open market, if the price moves above the strike price prior to expiration the option will increase in lock-step.

The covered call example

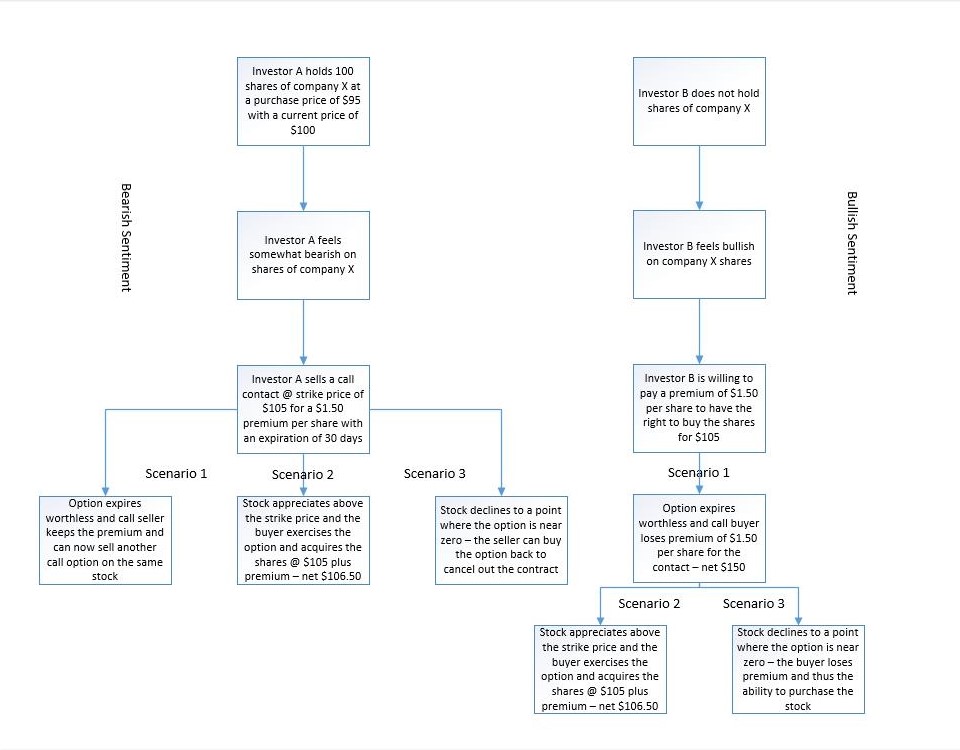

If a stock trades at $100 per share on the open market and one buys its call option at a $105 strike price, he has the right to purchase the stock for $105 regardless of the stock price between purchase and expiration. If the stock rises to $150, he still has the right to buy the stock for $105 prior to expiration. Since the payoff of purchased call options increases as the stock price rises, buying call options is considered bullish as notated in the introduction. In this case, the buyer believes the stock will increase in the near-term and buys the right to purchase the stock below where the buyer believes the stock price will be in the near term. When the price of the underlying stock surpasses the strike price, the option is said to be "in the money" and at this point the buyer may exercise the option contract. Conversely, if the stock falls to below $105, the buyer will not exercise the option, since he would have to pay $105 per share when he can buy the stock on the open market for less. If this occurs, the option expires worthless, and the option seller keeps the premium in the form of cash as profit. Since the payoff for sold call options increases as the stock price falls, selling call options is considered bearish as indicated in the introduction. The seller believes the stock will trade sideways or move to the downside over the near term and thus is willing to leverage his shares while collecting premiums. A comprehensive overview is depicted in Figure 1, illustrating the example discussed above (Figure 1).

Figure 1 – Fictional sequence of events and overview of a covered call and its possible outcomes

Option expires worthless

As outlined above in Figure 1, three fates of the covered call can come into in play. Remaining consistent with the example of stock X, the owner of stock X sells a covered call at a strike price of $105. Per my hypothetical example above, the owner initiated his/her position at $95 and thus has already captured an unrealized gain of 5.3% as the stock currently trades at $100. If the share price fluctuates but remains below $105 throughout the contract time span, the option will not be exercised. In this case, the buyer of the call would be able to buy the shares on the open market for a lower price than the $105 plus $1.50 premium. This scenario will result in the option seller keeping the shares of company X and keeping the premium. Effectively this will decrease the option seller’s share price by $1.50, or put another way, will provide the option seller with a 1.5% yield from its current price in cash. These option contracts are typically weekly, biweekly and monthly. This $1.50 premium is typical for an out-of-money covered monthly call contract. On a monthly basis this translates into an 18% return in cash assuming the shares are not called away.

Option is exercised

Since the owner is selling the option at a strike price of $105 this potentially adds an additional 5% from its current price if the option is called. Factoring in the premium of $1.50 per share this brings the total option return of 6.5% ($5.00 away from the strike plus $1.50 for the premium). From the original purchase price of $95 and the current price of $100 for the option, the seller has an opportunity to realize a 12% gain via the option if the shares are called ($10.00 to strike and $1.50 premium). If the shares of company X appreciate above the strike price, then the option seller misses out on any appreciation beyond the 12% return, and shares will be called away.

Buy to close the option

If the stock of company X decreases during the contract time span, not only will the intrinsic value of the option decrease, but the time value will also evaporate. The further away the stock price is from the strike price the lower the option value. If the option decreases from $1.50 to $0.25, the option seller can buy to close the contract for $0.25 and capture the spread of $1.25 while canceling any right the buyer had to purchase his/her shares. Now these shares are back to the owner as well as the $1.25 spread in net cash.

Conclusion

The covered call option is a conservative way to utilize options to mitigate risk, generate cash via premiums and augment portfolio returns. The basic framework and keys to selling covered calls is outlined above. The next piece will focus on more specific examples and criteria regarding selling covered calls and optimizing stock leverage. This is a powerful way to accentuate portfolio returns if the stock of interest decreases in value, trades sideways or trends upward (without crossing the strike price threshold) as the premium will be kept despite any of these outcomes. To offset the risk of losing out on potential appreciation, the option seller is paid a cash premium that is deposited into the option seller’s account and never relinquished. Taken together, the owner of an underlying security can leverage his/her shares in a meaningful manner to mitigate risk and augment portfolio returns. This can be performed in a conservative manner as long as the options are sold far beyond the current price (out-of-the-money). This exercise can be repeated on a monthly basis for small yields that can be very impactful to any portfolio over the long-term.

Thanks for reading,

The INO.com Team

Disclosure: The author is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Please feel free to comment and provide feedback, the author values all responses.