Every month, I release a new video for MarketClub members...

I cover everything from current market conditions and trading lessons learned (good and bad), to stocks on my watch list, questions I receive from members, and more.

Here is a sneak peek of my August Bonus Training Video.

Today’s theme is Bear Market ’22... shocker right?! Well, this one is a good one and I’m going to cover a lot so let’s jump in!

The good news is, we’re in a solid bear market rally and just flashed a monthly Trade Triangle in the big 3! I’ll look back at past bear market rallies and show you how the Trade Triangles have been an excellent indicator of changes and traps in the past (including getting you out before a 20% pullback in the most recent bear market). I’ll show you what I’m looking at and what to be cautious of.

Now full disclosure, even though we’ve seen these new Triangles issued, my gut tells me we haven’t seen the end of this bear market. But guess what? THE MARKET DOESNT CARE WHAT I THINK, so I trade what the market and signals tell me.

So, today we’ll do something we haven’t done in a while, look through some charts and scan for some trades! After all, the market is going up and as we’ve seen already the signals rarely, if ever, let us down!

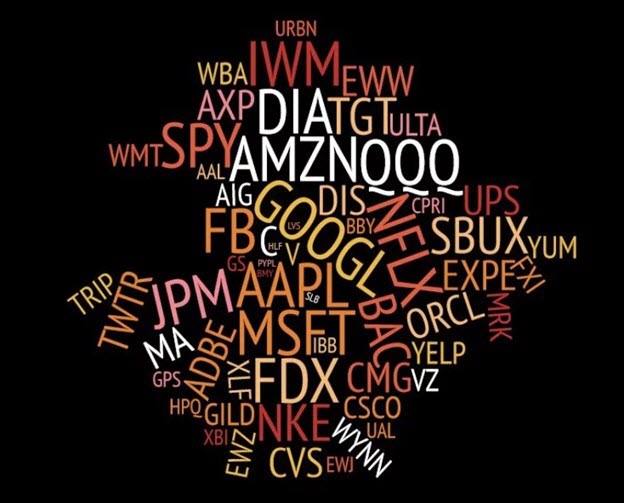

I’ll break down the Top Options list into 13 potential stocks to watch for options trades!

I’ll ALSO cover how to survive market corrections, the journey to a million dollars, the 3 skill sets to build wealth, and more. Continue reading "Sneak Peek: Bear Market '22"