Since the start of 2017, the Nikkei 225 has lagged in performance; with a 2.8% return since 2017 began, it lagged the S&P 500'S 2.8% RETURN, and it lagged its Asian peers, the Hang Sang and the South Korean KOSPI, which gained 16% and 16.7%, respectively, year to date. Despite all that lagging, however, the future trend for the Nikkei 225 might be the most promising. The reason? The BoJ’s monetary policy, and how it is trailing the performance of the Japanese economy.

BoJ Policy vs Reality

In a recent speech at the University of Oxford, Bank of Japan Governor Haruhiko Kuroda stressed that, despite the latest improvement in Japan’s economic performance, inflation (the rise in prices) is still far from the BoJ’s target of 2%. As the official statistic released from Japan’s statistic Bureau suggests, Kuroda is right. Japan’s headline inflation hit 0.4%, still persistently close to 0%. Add to that the risk of another sell-off in oil and the downside risk for Japanese inflation seems very present. Together, that makes it incumbent upon the Bank of Japan to keep its ultra-loose policy. Nonetheless, something about Japan’s official data doesn't add up.

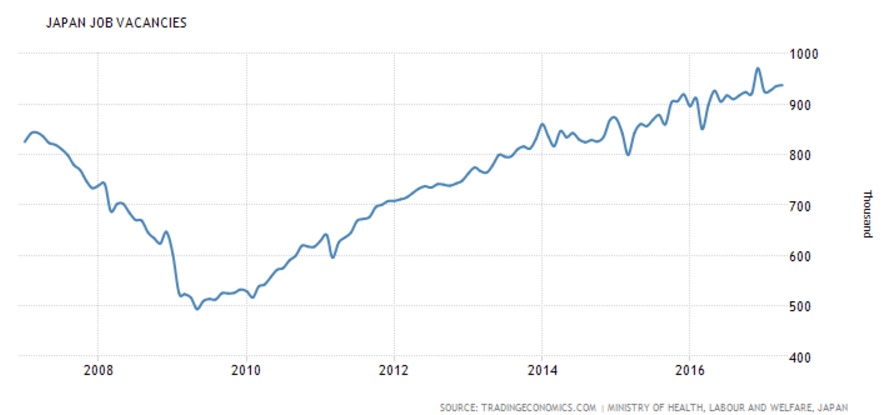

First and foremost, under scrutiny is the data coming out of the Japanese job market. According to the latest official data, Japanese wages rose by 0.5% in April on a year-over-year basis. Although this is an improvement from the 0% gain in March, it is still a rather stagnant growth rate in wages. And though it may jive with Japan’s low inflation rate, it does not sit well with other figures coming from the Japanese job market. The latest unemployment release points to a record low of 2.8% unemployment in Japan. Additionally, job vacancies figures show a steep rise in job vacancies. Job vacancies reached an all-time in December 2016, hitting 971 thousand job vacancies, and is currently holding firm above 900 thousand, with 937.80 thousand job vacancies in April.

Chart courtesy of Tradingeconomics

In other words, the Japanese job market is tight with an accelerated demand for workers even as the job market is already at full employment. The basics of supply and demand economics suggest that when demand is overwhelming high, supply prices are pressed upwards or, in this case, wages. But the official data shows that wages growth, while improving, is still rather stagnant. And those two contrasting facts just don't add up.

Meanwhile, an independent analysis by Morgan Stanley suggests, in fact, that it's not only that wages are rising in Japan, but at 2.2% annually, the fastest pace since the 1990s And that data sits perfectly with a tight job market. What that means is that Japan’s official data on wages is trailing the actual data and because the Bank of Japan uses official data to establish monetary policy, the BoJ’s policy is also trailing the real economy.

It’s true, given the latest revision of GDP growth in Q1 to 1.30% from 1.6%, the Japanese economy is far from overheating. Nonetheless, with a 1.3% growth rate alongside a surge above 50 in the readings from the Japan Manufacturing PMI and Japan Services PMI, and with wage growth accelerating above 2%, it’s clear the Japanese economy is on the right track. Certainly, Japan’s economy is not weak enough to warrant the BoJ’s continued -0.1% benchmark rate. And given Kuroda’s continued assertion that the BoJ inflation target is still distant, negative rates are set to persist. And when rates are too low for the real economy, investors flock into equities.

Nikkei Long View

Given that Japan’s monetary policy favors equities, it’s not unexpected that major Japanese indices, such as the Topix and Nikkei 225, are poised to gain. But how sustainable will those gains be? That depends largely on pricing. Is the current level of the Nikkei 225 already pricing in the dissonance between the BoJ’s monetary policy and the real economy?

The Nikkei 225 P/E ratio is 18, adjusted to the index weights, compared to a P/E of 24 for the S&P 500. Another important fact is the dividend yield of the stocks within the index. A weighted averaged, according to the index weight, suggests a dividend yield of 1.81%. That is compared to a 0.57% yield on Japanese 10-year government bonds. When the dividend yield for stocks is substantially higher than that of the 10-year government bond benchmark, it is a strong indication that stocks are relatively undervalued and, in this case, the index, and the stocks within the Nikkei 225 index.

Comparatively, in the US, the ratio is the opposite (which is itself worrying), with the US 10-year government yield is at 2.14% (at the time of this article) while the S&P 500 weighted dividend yield is at 1.95%.

That is all quite telling and suggests the Nikkei 225 valuation is reasonable compared to its peer, the S&P 500. Moreover, there is a precedent for this situation; from 2012 to 2015, when the S&P 500 the Fed’s monetary policy was too easy for the “real economy,” the S&P 500 had a remarkable run. Now, the Nikkei 225 is in the same situation, not pricing in the fact that the BoJ policy trails the “real economy.” Thus, the Nikkei 225 could be heading for another long bullish cycle.

Best,

Lior Alkalay

INO.com Contributor

Disclosure: This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.