CVS Health (CVS) wasn't immune from the market declines that were inflicted by the COVID-19 downturn. Despite being in the traditional defensive healthcare space and confined to domestic operations, the stock has not been able to break out and participate in the broader raging bull market post-CVOID-19 lows. The combination of CVS Health (CVS) and Aetna was proving to be a success after initial skepticism by investors. CVS even posted a string of better than expected quarters in part attributable to the Aetna acquisition. CVS is generating large amounts of free cash flow, paying down debt, and returning value to shareholders in a variety of ways. To further boost long-term growth prospects, restore growth, and fend off potential competition, CVS combined with Aetna. This combination creates the first through-in-through healthcare company, combining CVS's pharmacies and PBM platform with Aetna's insurance business. The new CVS combines its existing pharmacy benefits manager (PBM) and retail pharmacies with the second-largest diversified healthcare company.

CVS has been in a perpetual stock slump with or without COVID-19 in the backdrop. CVS has been beaten down for years, plummeting by over 50% ($113 to $52) from its multi-year highs. The stock currently sits at a bleak ~$58 per share and struggling to hold on to any share price appreciation despite the positive string of recent earnings with plenty of runway left in its growth from its Aetna acquisition. This was a bold and hefty price tag to pay yet necessary to compete in the increasingly competitive healthcare space, changing marketplace conditions, and political backdrop with drug pricing pressures. CVS made a defensive yet necessary acquisition to enable the company to go back on the offensive. At current levels, CVS presents a compelling investment opportunity; however, it has been a value trap for years despite the company still being in the early stages of its CVS-Aetna combination, which will drive shareholder returns for years to come.

Challenging Backdrop

The pharmaceutical supply chain cohort, specifically CVS, has been unable to obtain a firm footing in the backdrop of consolidation within the sector, negative legislative undertones, drug pricing pressures, rising insurance costs, and a market that has lost patience with these stocks. These factors culminated in sub-par growth with a level of uncertainty as the sector continued to face headwinds from multiple directions. Many of the stocks that comprised this cohort presented compelling valuations in a very frothy market. This allure had been a value trap as these stocks continued to disappoint. It's no secret that these companies have been faced with several headwinds that have negatively impacted the growth and the changing marketplace conditions have plagued these stocks.

Getting started is easy! Test our tools with a 30-Day Trial.

The political backdrop has been a significant headwind for the entire pharmaceutical supply chain (i.e., drug manufacturers, pharmaceutical wholesalers, and pharmacies/pharmacy benefit managers). Exacerbating the political climate, the drug pricing debate continues to rage on throughout political and social media circles weighing on the sector. This backdrop erodes pricing power and margins of drugs that ultimately move from drug manufacturers to patients with insurers and other middlemen playing roles in the supply chain web. To address these headwinds and restore growth, companies have made bold moves such as CVS acquiring Aetna to form one of the largest healthcare companies. Making bold acquisitions to restore growth may be the most viable means to heed competitive threats (i.e., Amazon with Pill Pack) and fend off headwinds. CVS will play an instrumental role in the future of healthcare and will have a growth runway in front of the company as healthcare spending continues to rise. Now that growth has been restored at CVS with Aetna being fully integrated to yield a fully functional bumper-to-bumper healthcare colossus, the stock still hasn't broken out.

CVS Enterprise Synergies

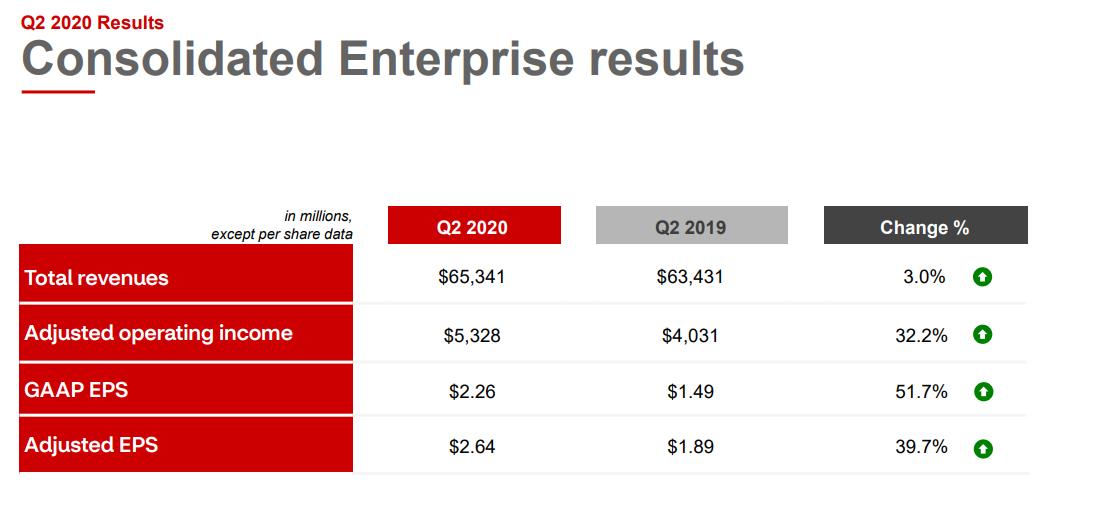

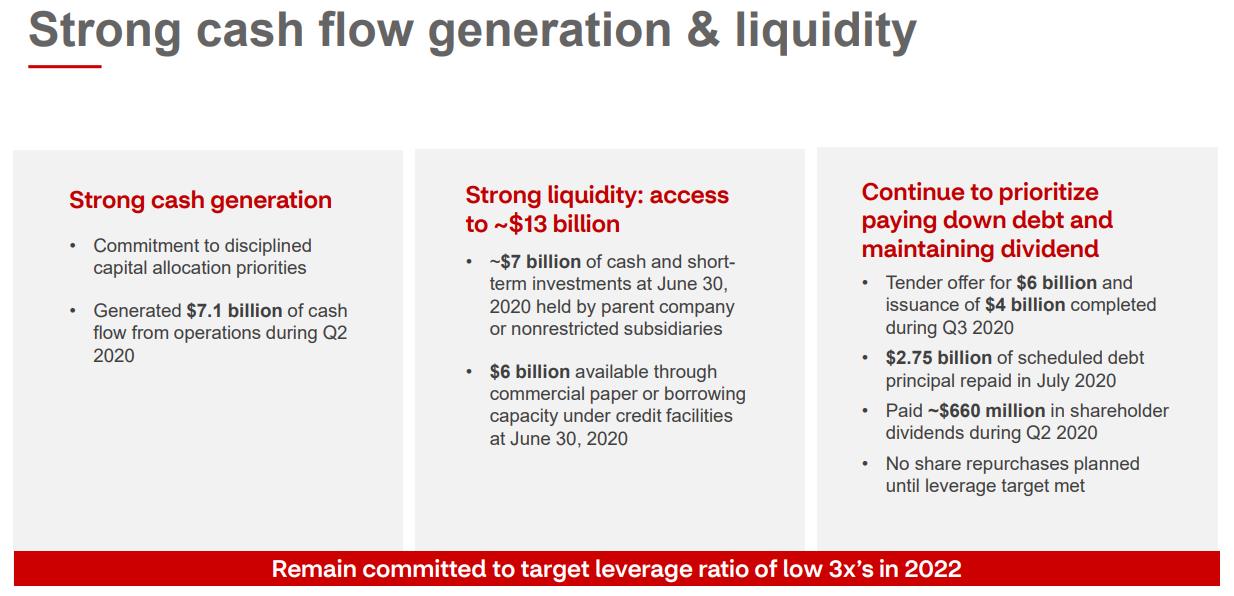

With the enterprise synergies via the Aetna combination, the newly formed CVS will continue to unlock value and growth over the long-term. This value creation will come through medical cost savings, membership expansion, customer retention, expanded customer value, and partnerships. This can already be seen from its recent string of quarterly reports (Figures 1 and 2).

"We're a health innovation company that is built to meet the evolving needs of the millions we serve every day. That's been made clear as we continue to navigate the health, social and economic impacts of COVID-19. Our earnings in this environment demonstrate the strength of our strategy and the power of our diversified business model. "We have a strong foundation of clinical expertise, data analytics, and digital capabilities, and unmatched consumer and community reach, which has allowed us to bring our strategy to life at an unprecedented time rapidly. The environment surrounding COVID-19 is accelerating our transformation, giving us new opportunities to demonstrate the power of our integrated offerings and the ability to deliver care to consumers in the community, in the home, and in the palm of their hand, which has never been more important. We have stayed true to our purpose of helping people on their path to better health, and we remain focused on creating value for all our stakeholders." CEO Larry Merlo

Figure 1 – Q2 2020 earnings highlights

Figure 2 – CVS paying down debt and generating strong cash flow

Summary

CVS Health (CVS) has been beaten down for years, plummeting by ~50% from its multi-year highs and has been a value trap along the way. CVS has been pressured from all directions, specifically with drug pricing pressures eroding margins and limiting margin expansion over time. A secular decline in brick and mortar retail has hindered foot traffic and same-store sales growth. To boost long-term growth prospects, restore growth, and fend off potential competition, CVS combined with Aetna. Now, this pharmaceutical supply chain heavyweight is not only surviving but competing and reviving its dominance in the marketplace now that its combination with Aetna has been fully integrated. The combination of CVS and Aetna is proving to be a success, as demonstrated by a string of better than expected quarters, partly attributable to the Aetna acquisition. CVS generates large amounts of free cash flow, paying down debt, and returning value to shareholders with continuing to pay out dividends. I feel CVS is early in its transformation and presents value coupled with a solid growth profile for the long term investor. Unfortunately, CVS has been a value trap throughout this transformation; however, I feel that it's a matter of time before the stock appreciates.

Noah Kiedrowski

INO.com Contributor

Disclosure: The author holds shares in AAL, AAPL, AMC, AMZN, AXP, DIA, GOOGL, JPM, KSS, MSFT, QQQ, SPY and USO. However, he may also engage in options trading in any of the underlying securities. The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses. The author is the founder of www.stockoptionsdad.com where options are a bet on where stocks won’t go, not where they will. Where high probability options trading for consistent income and risk mitigation thrives in both bull and bear markets. For more engaging, short duration options based content, visit stockoptionsdad’s YouTube channel.

Good to know. I was just about to sell CVS