It’s been a tough year for investors in the Gold Miners Index (GDX), with the ETF shedding 38% of its value since its April highs.

It’s been a tough year for investors, with the ETF shedding more than 45% from its multi-year highs. A gold price decline exacerbated this tumble. For the weakest producers, this is a concern.

While this has led to many investors steering clear of the sector, some miners are now at their lowest multiples since the 2015 bear market bottom, when margins were half what they are today. Many miners were carrying considerable amounts of debt.

Today, this same group of producers will enter Q4 2022 in net cash positions, are paying out dividends double that of the S&P-500 (SPY), and are much more disciplined, learning from past mistakes. To summarize, I see this as a rare opportunity to buy a few high-quality businesses.

Let’s take a look at three stand-out names below:

Agnico Eagle (AEM)

Agnico Eagle Mines (AEM) is the world’s 3rd largest gold producer, on track to produce approximately 3.3MM ounces of gold this year. This significant growth from ~2.0MM ounces in 2021 is related to the merger of equals with Kirkland Lake Gold (KL), which saw the company add three of the world’s most profitable mines to its portfolio (now 11 mines total).

Notably, the company did not sacrifice from a jurisdictional safety standpoint when considering this transaction, adding three mines in two of the most attractive jurisdictions globally: Canada and Australia.

Normally, the large producers do not make great investments. This is because they struggle to grow production and reserves per share. The lack of growth is not their fault and is not due to poor management.

Instead, it’s because major discoveries are becoming rarer, and their size makes it hard to grow organically, with 100,000 - 200,000 ounce per annum operations not really moving the needle.

However, AEM is in a unique situation, having multiple opportunities to grow production within its portfolio and four development projects in the wings where it could also grow production. So, if the company can execute successfully, it could see production increase to 4.5MM ounces per annum by 2029.

AEM’s potential for a 35% production growth rate (2029 vs. 2022) means that it should be able to grow cash flow and earnings per share each year regardless of whether the gold price chooses to cooperate or not, a key differentiator.

Meanwhile, its operating costs should average $950/oz (2023-2026), making it one of the few producers that could withstand a drop to $1,400/oz in the gold price.

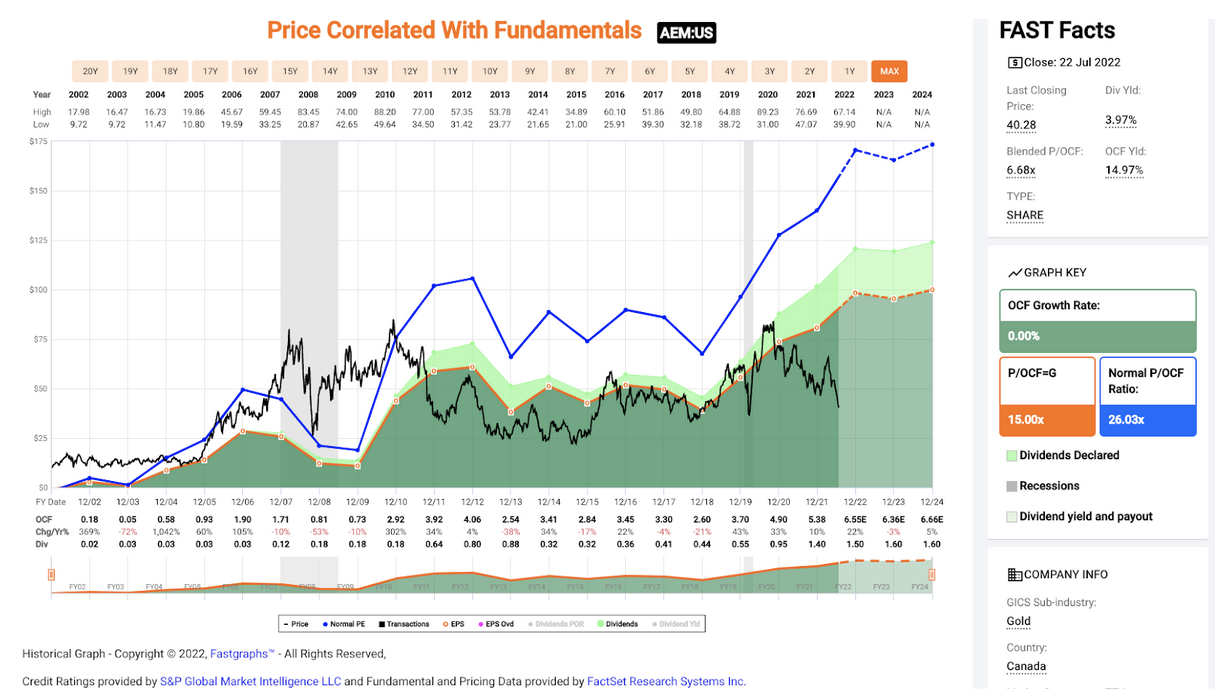

Despite this unique position, the stock is trading at its lowest levels since 2015, at a valuation reserved for a producer with a weak balance sheet and slim margins. This is not the case at all, though, with AEM set to end the year in a net cash position and being one of the highest-margin producers sector-wide.

As shown above, AEM has historically traded at 26x cash flow and currently trades at less than 7x FY2022 cash flow estimates.

Even if we use a more conservative multiple of 13x cash flow, a 50% discount to the historical multiple, AEM would command a valuation of $78.00 per share, which also assumes more conservative cash flow per share estimates ($6.00 per share). Hence, I see this pullback in the stock as a gift, with it rarely ever being this cheap over the past decade.

Kinross Gold (KGC)

Kinross Gold (KGC) is a mid-cap gold producer with multiple mines in the Americas, as well as the massive Tasiast Mine in Mauritania.

Like Agnico, Kinross has been punished over the past year and is down a whopping 70% from its highs. This under-performance is partially due to having to sell its Russian assets in a 50% off sale following the invasion of Ukraine.

Although this padded the company’s balance sheet with $300MM in cash and an additional $200MM from its Chirano Mine sale, it put a severe dent in what Kinross was touting as a growth profile post-2022 (400,000 fewer ounces of annual production related to its sales).

While this is a downgrade from the previous investment thesis (20%+ growth at slightly lower costs), the sell-off in the stock looks to be overdone. This is because with Kinross shedding its Russian exposure, it should be able to command a P/NAV and cash flow multiple that’s closer to that of its peer group vs. the discounted valuation it was stuck with previously.

So, even though Kinross has seen a $1.1 billion decline in net asset value [NAV] from its sales, it will be partially made up for with an increase in its P/NAV multiple.

In addition, the company is now a lot more attractive to prospective investors (aside from its lacking growth), with more than half of future production coming from Tier-1 jurisdictions (United States, Canada, Chile).

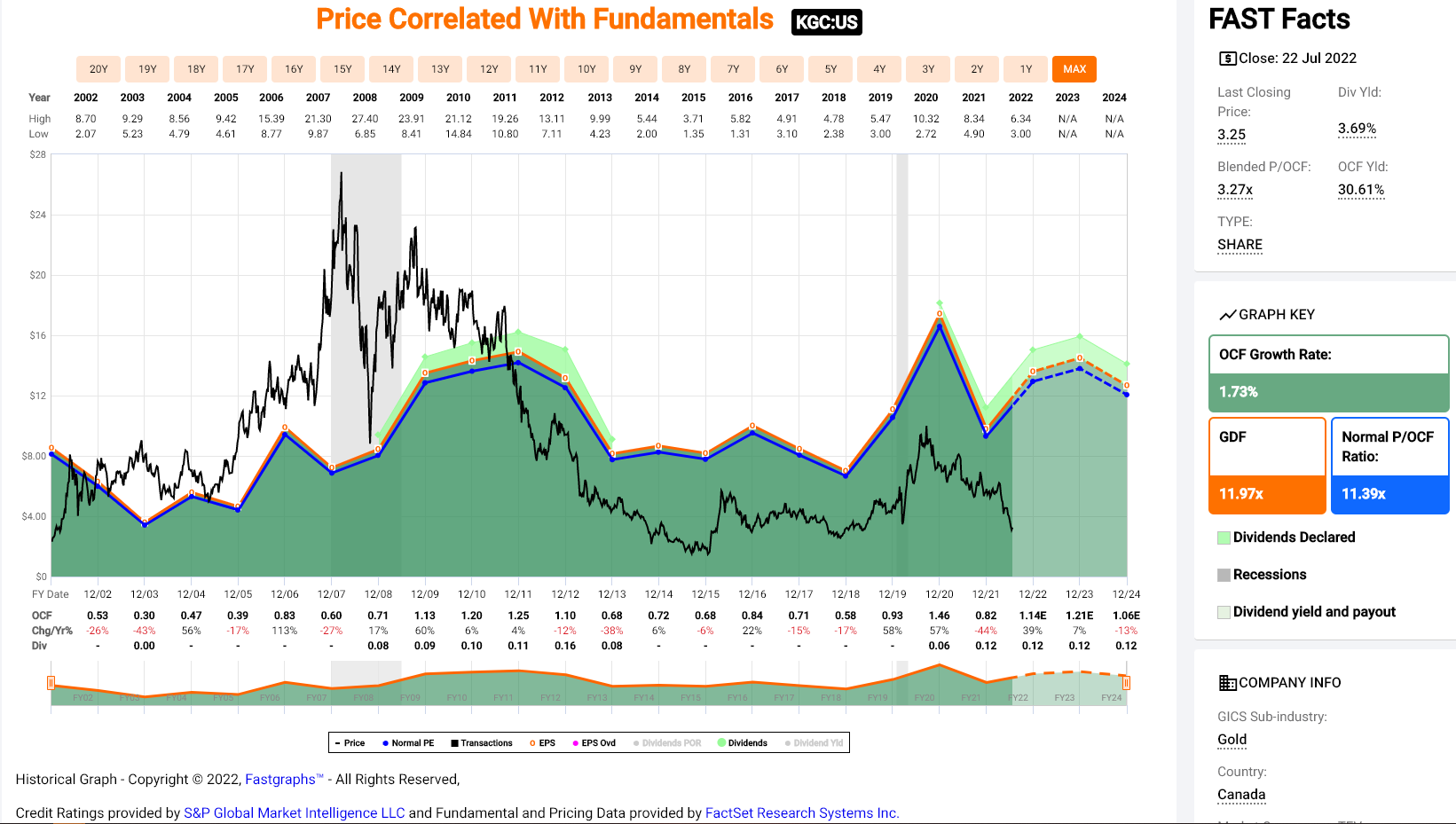

Looking at the chart above, we can see that KGC has historically traded at 11x cash flow, but its 10-year average has been closer to 6x cash flow. Currently, the stock trades at just 3.25x FY2022 cash flow estimates, and this assumes that cash flow per share comes in at just $1.00.

So, while there are certainly more attractive names out there to own, given Kinross’ mediocre long-term track record, this is an opportunity to buy a decent business at a very attractive price. To summarize, I see this pullback below $3.30 as a rare buying opportunity, and I would not be surprised to see the stock trade above $5.00 in the next 12 months.

Eldorado Gold (EGO)

The final name worth keeping an eye on is Eldorado Gold (EGO), a much riskier and more speculative name given that it’s a smaller producer in some less favorable jurisdictions (Greece, Turkey).

However, the stock is now down more than 50% from its highs and trading at one of its cheapest valuations in years. Based on FY2022 guidance, Eldorado Gold expects to produce over 450,000 ounces of gold, with the potential to grow production to more than 500,000 ounces at sub $1,100/oz costs by 2025. This base case scenario is not all that attractive, even if Eldorado is very reasonably valued at just ~3.0x FY2022 cash flow estimates.

However, in addition to its current operating portfolio, Eldorado owns the Skouries gold-copper Project in Greece, a mine capable of producing more than 160,000 ounces of gold per annum between 2025-2035. While this isn’t that significant of a production profile, the cost profile will be industry-leading, with all-in sustaining costs after by-product credits expected to come in at less than $100/oz.

This would help Eldorado to transform itself from a 450,000-ounce per annum producer at $1,100/oz costs to a ~650,000-ounce per annum producer at sub $900/oz costs, which should lead to a re-rating in the stock. So, with the stock down over 55% from its highs just four months ago, this violent correction looks like a buying opportunity. However, this is not a stock for risk-averse investors, given its sub $1.2BB market cap.

Once every few years, a fat pitch arrives in the gold sector, offering an opportunity to invest in gold miners that are trading at levels where they could potentially double over the next two years. This opportunity looks to have arisen, and AEM looks like the lowest-risk way to play this opportunity at $40.00 per share.

Disclosure: I am long AEM, KGC, GLD

Taylor Dart

INO.com Contributor

Disclaimer: This article is the opinion of the contributor themselves. Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.