It’s been a challenging year thus far for the restaurant industry, with dollars typically allocated to entertainment and a Friday night out wrestling to steal priority from rising gas bills, elevated energy costs, and higher mortgage rates.

Some restaurants have resorted to discounting to drive traffic, while others have relied on menu innovation and limited-time offers vs. promotional activities to protect their already softening margins.

Those brands that are the most out of touch have continued to raise prices at a double-digit pace to ensure they maintain margins, with Chipotle (CMG) being one such offender. While this is likely to protect margins in the interim and allow the company to meet earnings estimates, it could backfire over the medium-term, with loyal customers feeling taken advantage of after being hit with consistent menu price increases in a recessionary environment.

Although this has made it difficult to invest in the sector, a few names are doing a great job navigating the current environment, and following recent share price weakness, they’ve slipped into undervalued territory.

One is a new breakfast chain that’s bucking the negative traffic trends in the casual dining space and enjoying industry-leading retention due to a key competitive advantage. The other is a pizza chain that’s enjoying strong unit growth, and while it’s having a tough year, annual EPS is forecasted to hit new all-time highs in FY2023 and FY2024.

Let’s take a look below:

First Watch Restaurant Group (FWRG)

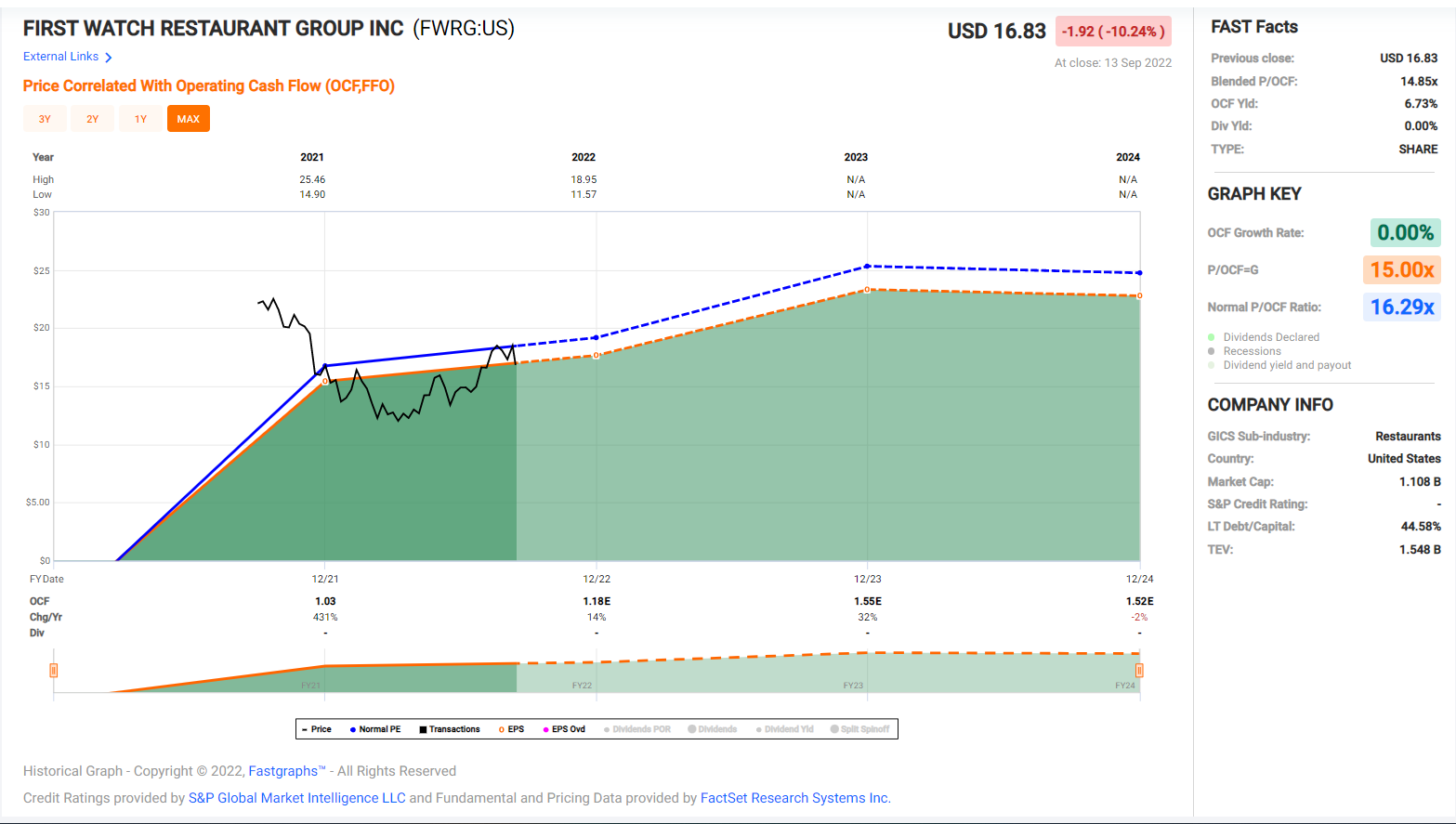

First Watch Restaurant Group (FWRG) is a brand with over 450 restaurants serving breakfast in the United States, with a unique model being open from just 7 AM to 2:30 PM.

This has allowed the company to evade the industry-wide staffing issues, with its team members able to maintain a work-life balance, which isn’t possible for most restaurant brands.

In addition to solid staffing metrics that led the industry average, the company released blowout results in Q2, reporting traffic growth of 8.1% vs. an industry that saw negative 4% traffic in the quarter.

This translated to 20% system-wide sales growth ($231.2MM) and 13.4% same-restaurant sales growth, which trounced analyst estimates. The only negative in the report was that commodity costs came in higher than expected, stealing the sales leverage and leading to a 400 basis point decline in restaurant operating profit.

That said, this is still a very respectable figure, and the contraction in margins was largely due to being so conservative with pricing since the pandemic began. With the benefit of an overdue 3.9% price increase in July, I expect much of this margin pressure to abate.

Despite this incredible sales performance in a quarter where traffic has been anemic, First Watch trades at a very reasonable valuation, sitting at just 10x FY2023 cash flow estimates. This might appear steep at first glance, but this business is growing units at a double-digit pace, making it one of the fastest-growing brands sector-wide.

Importantly, this growth is supported by growing average unit volumes, solid margins, and supportive staff, de-risking the growth profile vs. other brands. So, if this weakness in the stock persists, I would view any pullbacks below $14.40 (9.3x FY2023 cash flow) as a buying opportunity.

Papa John’s International (PZZA)

Papa John’s International (PZZA) is a mid-cap pizza chain in the restaurant space, and the company just came off a huge year, reporting record annual earnings per share of $3.43, a 145% increase from the year-ago period.

This was driven by impressive same-store sales growth, opportunistic share buybacks, and double-digit unit growth, an impressive feat for a company with over 5,000 restaurants globally (5,650 restaurants in 50 countries as of year-end 2021).

However, the company’s phenomenal year pinned it up against tough year-over-year comps, having to lap 145% earnings growth in a macro environment that’s much trickier to navigate. While the softened Q2 results were largely out of the company’s control, they came in below what the market was looking for, with revenue of just $522.7, a 5% increase over the year-ago period.

Meanwhile, although comparable sales in North America remained positive at 0.90%, International comparable sales dipped deeply into negative territory at (-) 8.0%.

While this is undoubtedly an ugly headline number, it’s important to contextualize the two figures. Although comp sales were down on a consolidated basis and fell sharply internationally, Papa John’s two-year stacked same-restaurant sales are sitting at 6.1% and 13.2%, respectively, with International (13.2%) having to lap a 21.2% growth rate in Q2 2022.

These are solid figures, but the deceleration combined with inflationary pressures that hit earnings (quarterly EPS: $0.74 vs. $0.93) has put a severe dent in the stock.

The good news is that this 42% correction has left PZZA trading well below its 10-year average earnings multiple of 35, and even if annual EPS sinks year-over-year, it will still be up over 120% vs. FY2020 levels. More importantly, it’s expected to hit new highs in FY2023 and FY2024 based on current estimates of $3.71 and $4.08, respectively.

Hence, I see this aberration in this strong earnings trend as a buying opportunity. That said, the ideal buy point for PZZA comes in at $77.00 or lower, where it would trade at ~21x FY2023 earnings estimates vs. what I believe to be a fair value of $110.00 per share, translating to a 30% discount to fair value.

While FWRG and PZZA may not be in low-risk buy zones, these are two names with strong growth that have loyal customer bases, boast strong unit growth, and are temporary victims of their success. This is because their strong FY2021 resulted in them being up against nearly insurmountable comps this year.

Still, I see the future as bright for both brands and meaningful earnings growth on the horizon post-2022, so I would view pullbacks below $14.50 on FWRG and $77.00 on PZZA as buying opportunities.

Taylor Dart

INO.com Contributor

Disclaimer: This article is the opinion of the contributor themselves. Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing.