Harnessing options allows one to define risk, leverage a minimal amount of capital, and maximize return on investment. Options enable smooth and consistent portfolio appreciation without predicting how the market will move. Options enables one to generate consistent monthly income in a high probability manner in both bear and bull market scenarios. This can be accomplished since options can be structured to allow a margin of downside and upside stock movement while collecting income in the process.

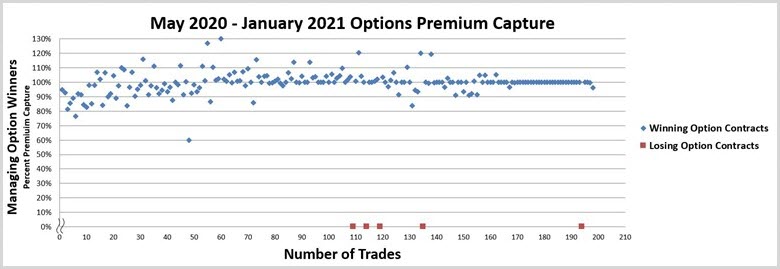

An agile options-based portfolio is essential to navigate pockets of volatility and mitigate market downdrafts. The recent September correction, October nosedive, and election volatility into November are prime examples of why risk management is paramount. Over the past ~9 months (May-January), 190 trades were placed and closed. An options win rate of 97% was achieved with an average ROI per winning trade of 7.7% and an overall option premium capture of 82% while matching returns of the broader market and outperforming during market downswings. An options-based portfolio's performance demonstrates the durability and resiliency of options trading to drive portfolio results with substantially less risk. The risk mitigation element is crucial, considering markets are richly valued as measured by any historical metric and technically breaking through its upper Bollinger band (Figures 1 - 6). An iron condor options strategy is a great way to reduce overall capital at risk when deploying options to drive portfolio results.

Options-Based Results

Figure 1 – Overall option metrics from May 2020 – January 10th, 2021

Figure 2 – Overall option metrics from May 2020 – January 10th, 2021

Figure 3 – Overall option options premium capture from May 2020 – January 10th, 2021

Figure 4 – Overall options return on investment from May 2020 – January 10th, 2021

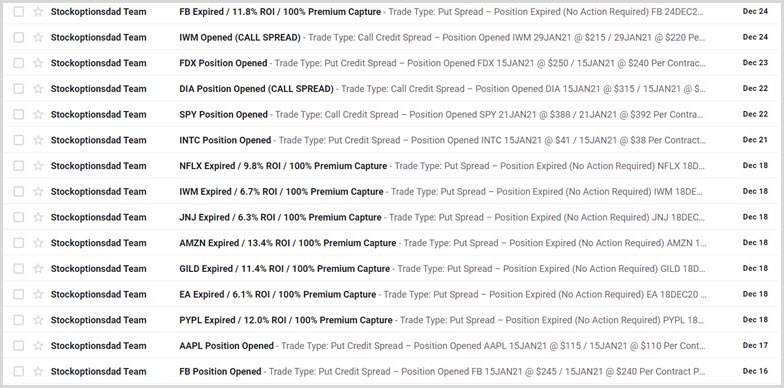

Figure 5 – Examples via email and text

Basic Framework - Iron Condors

An iron condor strategy is an ideal way to define risk and reduce the amount of total capital at risk by over 50%. This reduction in capital requirements can minimize risk and maximize returns in options trading. This strategy involves combining both a call spread and a put spread. Hence, selling a call option and buying a call option while collecting credit and selling a put option and buying a put option while collecting additional credit. When combined, premium credits are collected on the call spread and the put spread for a collective premium credit. When selling the call/put spreads, the premium is collected and simultaneously using some of that premium income to buy a call/put option at a further out-of-the-money strike price. The net result will be a credit on the four-leg trade with defined risk since the purchase of the call/put option legs serves as protection on either side of the trade.

Defined Risk Iron Condors

An iron condor is a type of options trade that risk-defines your trade and involves selling a call spread and a put spread. Let's review the iron condor as an example below.

Iron Condors - Call Spread Side

You agree to sell shares at the lower out-of-the-money strike until the contract's expiration. You also bought the right to buy the shares at the higher out-of-the-money strike to protect and define your risk. A portion of the premium income received from selling the lower strike was used to buy an out-of-the-money higher strike option. The difference in premium received and premium paid out for the protection is your net premium income. The difference between your strikes will be your max loss, less the net premium received.

Iron Condors - Put Spread Side

You agree to buy shares at the higher out-of-the-money strike until the contract's expiration. You also bought the right to sell the shares at the lower out-of-the-money strike to protect and define your risk. A portion of the premium income received from selling the higher strike was used to buy an out-of-the-money lower strike option. The difference in premium received and premium paid out for the protection is your net premium income. The difference between your strikes will be your max loss, less the net premium received.

Iron Condors Breakdown

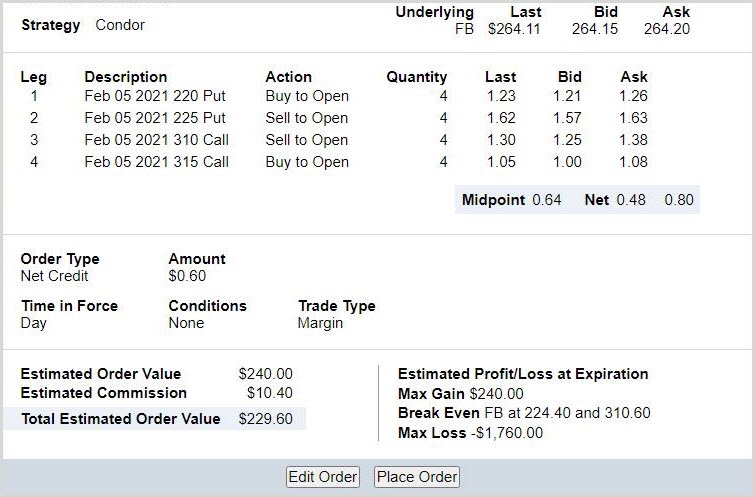

The call strike of $310 and put strike of $225 provide a margin of upside and downside of roughly 17.4% and 14.8%, respectively, from current levels since shares are currently trading at $264 per share. As long as the shares remain between the $310 and $225 by expiration, both spreads will expire worthless (Figure 6).

Figure 6 – Opening an iron condor via selling a call spread and put spread combination while taking in net premium income during the process. Capital requirement is equal to the strike widths, and maximum return is equal to the net premium received

50% Max Loss Reduction and Scenarios

An iron condor with the same expiration dates will expire together worthless with defined risk if the underlying security remains between the out-of-the-money call and put strikes ($225 and $315). If the option expires between the call strikes or put strikes, then losses will incur, and if the stock moves above or below your protection strikes, then a max loss will occur at expiration. A max loss is equal to one of the strike widths since the underlying security cannot expire on both the call and put side of the trade. Thus, max loss is equal to one strike width less the total premium received. This reduces max loss by over 50% relative to a regular call or put spread.

Example:

Selling an iron condor:

FB Call Credit Spread: 05FEB21 @ $310 / 05FEB21 @ $315

FB Put Credit Spread: 05FEB21 @ $225 / 05FEB21 @ $220

Per Contract Premium: Call Credit + Put Credit = $0.60

Required Capital Per Contract:

Call: ($315 - $310) = $500

Put: ($225 - $220) = $500

$500 call spread + $500 put spread - Net Premium of $60 = $940

Max Loss = $500 - $60 = $440 per contract

A. If the stock stays below $310 and above $225 at expiration, then you net the $60 in premium, and all four option legs co-expire worthless with 100% premium capture

B. If the stock trades above $310 or below $225, then you begin losing money, but the $315 and $220 strike legs cap any losses above $315 or below $220. If the stock falls between your strike width at ~$312 or ~$223, then a loss of $2 per share less the premium received of $0.60 per share will be your realized loss ($200 - $60 = $140 loss per contract).

C. If the stock trades above the call protection leg of $315 or the put protection leg of $220, losses are now capped at your strike width of $5 per share. If you were assigned at $310 or $225, you would then exercise your $315 or $220 strike option and buy shares at $315 or sell shares at $220 to cap losses at $5 per share less premium received of $60 resulting in a max loss of $440. Even if the stock was to rise to infinity or decline to zero, you have the right to buy shares at $315 or sell shares at $220, so any losses above $315 or below $220 are prevented.

Conclusion

The September correction, tail end October nosedive, and initial November volatility reinforces why appropriate risk management is essential. The risk mitigation element is essential, considering markets are richly valued as measured by any historical metric and technically breaking through its upper Bollinger band. An options-based approach provides a margin of safety while circumventing the impacts of drastic market moves and contains portfolio volatility. Despite market conditions, consistent monthly income was generated while keeping pace with the broader market returns and outperforming during periods of market weakness.

These Stocks Are Ready to Break Out

Over 5K stocks are trading on the U.S. and Canadian exchanges. While you may hear about the same companies over and over again, some of the biggest trading opportunities can come from "no-name" stocks.

See which stocks (some you may never have heard of) made it onto today's 50 top stocks ranked by their technical trend.

Sticking to the core fundamentals of options trading, one can leverage small amounts of capital, define risk, and maximize investment return. Following the 10 rules in options, trading has generated positive returns in all market conditions for the portfolio's options segment. The positive options returns were in sharp contrast to the overall market's negative returns in September and October. This demonstrates the durability and resiliency of an options-based portfolio to outperform during pockets of market turbulence. To this end, cash-on-hand, prolonged exposure to broad-based ETFs and options is an ideal mix to achieve the portfolio agility required to mitigate uncertainty and volatility expansion. Layering-in iron condors as part of an options strategy has many advantages, primarily because a max loss is reduced by over 50% compared to a normal call or put spread.

Thanks for reading,

The INO.com Team

Disclosure: The author holds shares in AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY and USO. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.