Introduction

Visa’s worldwide industry leading payments technology, dominance in the credit transaction space, secular growth towards cashless societies, Visa Europe acquisition, growing dividends, share buybacks and accelerating revenue and EPS growth culminate into a compelling investment case as a great long-term portfolio holding. As many countries make a secular transition towards cashless societies, the credit card transaction space will continue to reap the rewards of this trend via swipe fees and other services. Globally, Visa has been at the forefront of this space, accounting for more than 45% and 68% of all credit card and debit card transactions, respectively. Visa Inc. (NYSE:V) has it eyes set on capturing more market share from competitors such as Mastercard and more notably American Express in recent months via securing long-term branded credit card relationships with Costco, Fidelity and USAA. Visa has recently signed a partnership with PayPal which allows U.S. merchants with a Visa payWave reader to accept PayPal as a form of payment thus leveraging Visa’s payments network while benefiting Visa and merchants alike. Visa is unique in that it does not take on any financial liability as it serves as an intermediary to process payment transactions and capturing a fee for its payments technology/network. I feel that Visa is a great long-term holding that offers growth and stability independent of banks and/or interest rates.

The Unique Business Model

Visa is not a bank or financial institution thus does not take on any financial liability. Visa does not issue credit or debit cards nor do they extend lines of credit. Visa serves as an intermediary between the merchant and banks at the point of purchase in processing transactions. Visa provides financial institutions with Visa-branded payment solutions that they utilize to offer credit, debit and prepaid cards. In 2015, Visa’s global network processed 100 billion transactions with a total volume of $6.8 trillion dollars. As payments are processed, Visa charges a transaction fee therefore as payments volume increases Visa’s revenue increases. This financial model is immune from traditional credit defaults and thus may be a great way to gain exposure to a financial-like company without the financial risk or interest rate risk involved with banks.

Visa Europe acquisition and Added clients

Per Visa, the acquisition of Visa Europe creates one global company that further extends Visa’s payment solutions leadership while adding 3,000 European issuers, over 500 million card accounts and more than €1.5 trillion in payments volumes. The transaction consists of upfront €16.5 billion with the potential for an additional €4.7 billion payable following the fourth anniversary of closing, for a total value of up to €21.2 billion. The upfront costs of €11.5 billion consist of cash and Visa stock valued at €5 billion. The transaction capitalizes on strong growth opportunities in a highly desirable region. It positions the combined Visa to create value through increased scale, efficiencies realized by the integration of both businesses, and benefits related to Visa Europe’s transition from an association to a for-profit enterprise. Visa Europe was a membership association of over 3,700 European banks and other payment service providers that operated Visa-branded products and services across 38 countries. Visa Europe is the largest transaction processor in Europe, responsible for processing more than 18 billion transactions annually. There are more than 500 million Visa cards in Europe, and €1 in every €6 spent in Europe is on a Visa card. The acquisition of Visa Europe was completed earlier this year in June. In terms of financial implications, benefits from revenue synergies, cost savings and increased repurchases of stock will begin in fiscal full-year 2017. Visa expects the transaction to be accretive to adjusted EPS fiscal year 2017 in the low single-digit range. Following the completion of integration, the transaction is expected to be accretive to adjusted EPS in the high single-digit range by fiscal full-year 2020.

Future growth opportunities with this combined company are meaningful and significant. Per Visa, in Europe, an estimated 37 percent, or USD $3.3 trillion, of personal consumption expenditure is still accomplished via cash and check. Europe has also been an early adopter of mobile payments, which analysts predict will see strong growth in the future. Visa has aggressively launched new mobile payment partnerships, platforms and products that will enable faster growth and adoption of mobile payments in Europe. This includes new tokenization services, support for digital wallets and wearables, strategic investments in other enabling technologies, e-commerce and P2P payment capabilities, as well as the opening of several global innovation centers.

In addition to the Visa Europe acquisition, Visa has managed to wrestle domestic market share away from rivals by out-competing for major contracts with Costco, USAA and Fidelity. As part of the Costco transition, around 11.4 million co-branded American Express Costco cards were moved over to Citi during the switch, said Richard Galanti, Costco's chief financial officer. This makes up "just under 7.5 million accounts." Since the June 20 switch, "1.1 million members have applied for the new card and over 730,000 new accounts have been activated," said Galanti, adding this makes for slightly over 1 million additional Citi Visa cards in circulation. "It's still early. We launched only 14 weeks ago, but so far, we're beating our initial expectations in terms of conversion, usage and new sign-ups to the card." The Fidelity has over 500 million card holders that have been converted to Visa from American Express this year and Fidelity hopes that the new partnership will attract new card holders. USAA is the 10th largest credit and debit card issuers in the U.S. and recently converted over to Visa from Mastercard. USAA processed $26 billion on its cards for purchases in 2014. Taken together, the Visa Europe acquisition and major client wins will enable sustained and durable growth now and into the future.

Accelerating Revenue, Share Buybacks and Dividends

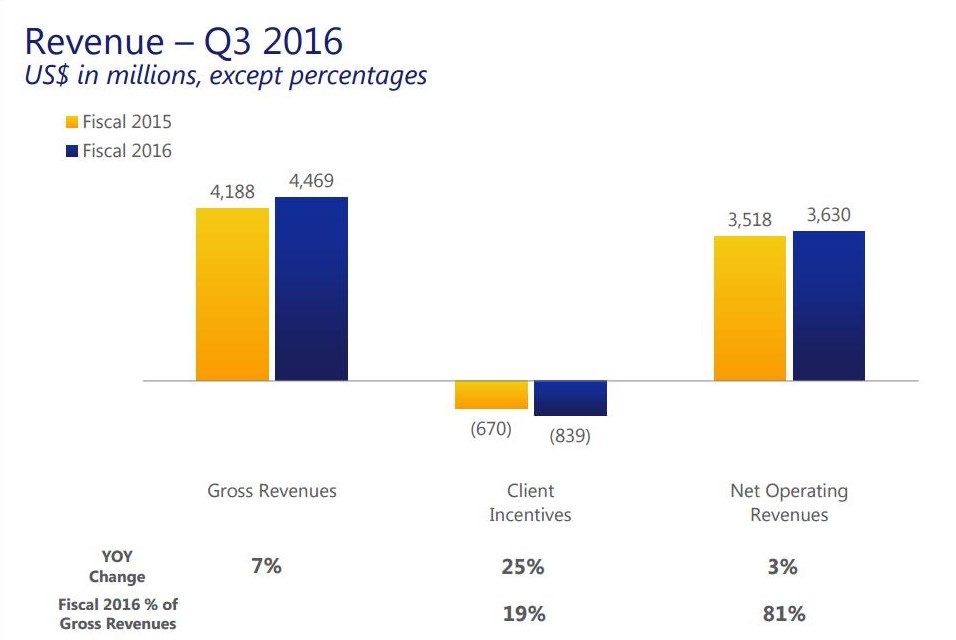

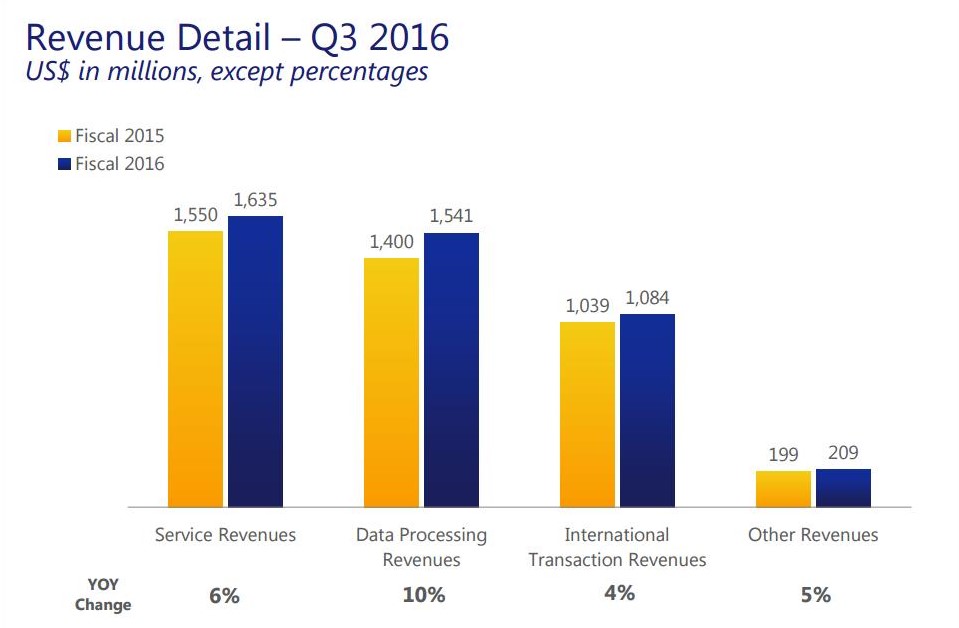

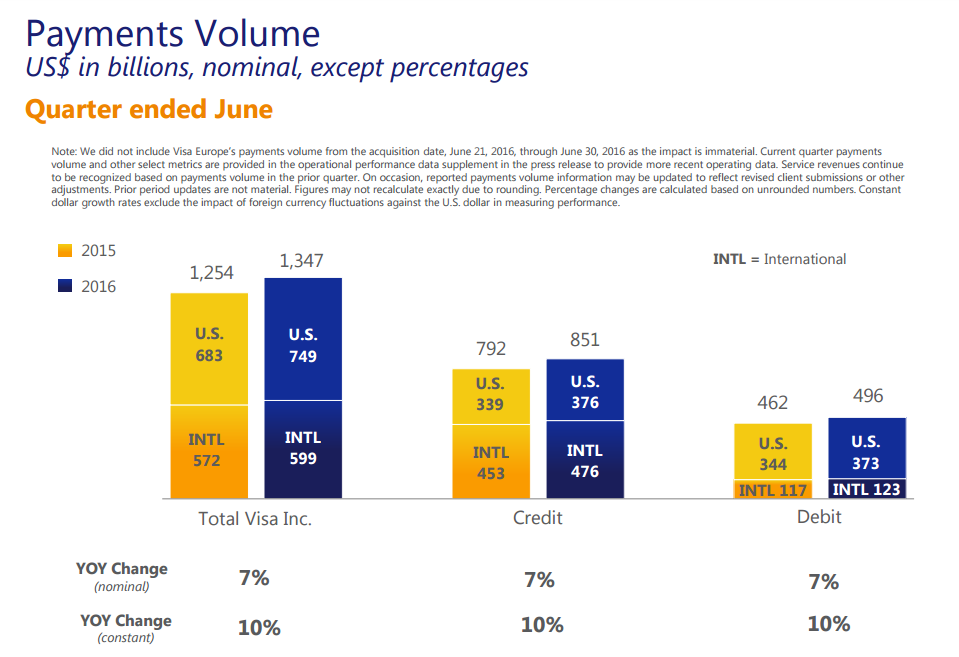

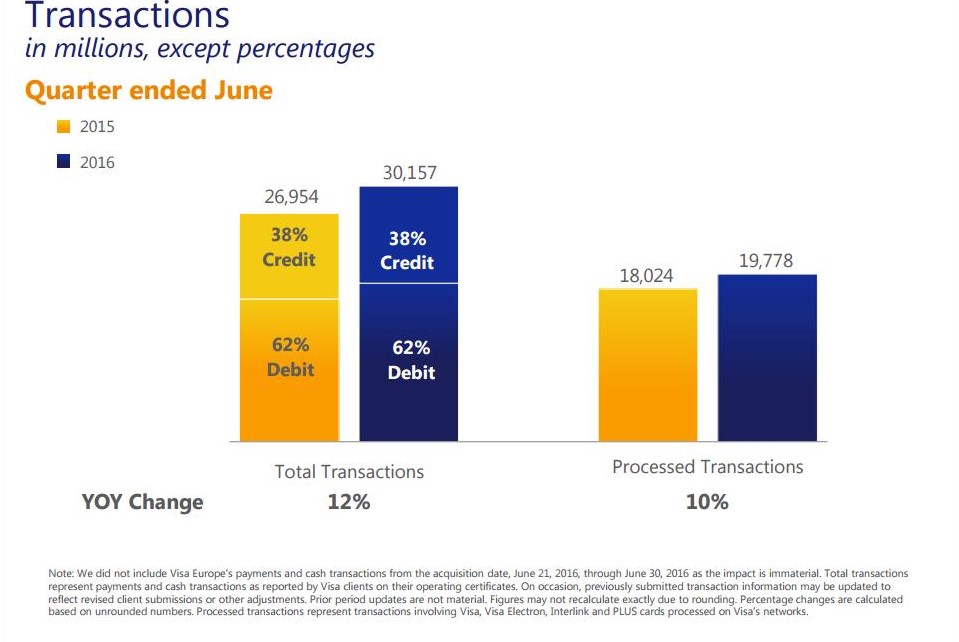

Visa recently announced Q3 2016 results with net operating revenues of $3.6 billion (up 3% over prior year), cash and equivalents of $12.4 billion and free cash flow of $2.0 billion. Some major growth highlights from the most recent earnings announcement can be seen in Figures 1 through 4. In brief, gross revenue increased to $4.469 billion year-over-year or 7% increase (Figure 1). Visa posted growth across all revenue segments from Service, Data Processing, International Transaction and Other by 6%, 10%, 4% and 5%, respectively (Figure 2). In terms of payments volume, Visa posted a 7% growth rate overall with an identical growth rate for both credit and debit cards (Figure 3). Total transactions increased at a healthy rate of 10% across the business (Figure 4).

Figure 1 – Fiscal Q3 gross and net revenue figures

Figure 2 – Breakdown of growth across revenue streams

Figure 3 – Payments volume figures

Figure 4 – Total growth in transactions

Taken together, Visa’s growth continues at a healthy clip and with the addition of Visa Europe coming online and added domestic accounts such as Costco, Fidelity and USAA bodes well for durable and sustained growth for years to come.

In terms of dividends, Visa has increased its dividend payout annually since initiating a dividend in 2008 and throughout the years has layered in share buyback programs to drive shareholder value. Although the dividend yield is less than 1%, the company has increased its payout per share from $0.03 to $0.14 since 2008 or 367% increase with plenty of room to increase the dividend. The current payout ratio for Visa sits at ~20% thus leaving plenty of room for future dividend increases. In terms of share repurchases, during fiscal Q3 2016, Visa repurchased 21.7 million shares in the open market at an average price of $77.53 per share, using $1.7 billion of cash on hand. Visa also recently announced a $5 billion share repurchase authorization during its Q3 2016 earnings announcement.

Conclusion

Visa Inc. (NYSE:V) has a unique position in the financial industry where no financial liability is taken while capturing fees on over 100 billion transactions globally. As many countries make a secular transition towards cashless societies, the credit card transaction space will continue to reap the rewards of this trend via swipe fees and other Visa-branded solutions. Visa has made efforts to capture more market share with the recent addition of major customer accounts with Costco, Fidelity and USAA. Visa also has its eyes set globally with the Visa Europe acquisition which should immediately add to revenue and EPS once fully integrated. With healthy accelerating revenue, dividend increases, share buybacks and strategic partnerships/acquisitions Visa belongs in any long-term growth portfolio. Furthermore, Visa’s financial model is immune from traditional credit defaults and thus may be a great way to gain exposure to a financial-like company without the financial risk or interest rate risk involved with banks.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure:The author currently holds shares of Visa and the author is long Visa. The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses.