Introduction

Share buybacks can serve as an effective way to drive shareholder value via returning capital to shareholders by repurchasing its own stock. Share buybacks are primarily driven by companies that strongly feel their shares are undervalued based on current fundamentals, future growth prospects and cash on hand. Taken together, executive boards approve share buyback programs based on these attributes in concert with undervaluation on the open market. Additionally, the company of interest feels a sense of bullishness and confidence on the future and sustainability of their business.

Theoretically, repurchasing and retiring shares satisfies many shareholder friendly objectives:

1) Reducing the number of shares tilts the supply and demand curve thereby removing shares will decrease supply and in turn increase demand and drive the share price higher

2) Earnings per share increase since earnings are now dividend over fewer shares

3) If share buybacks are coupled with a dividend, the dividend yield may increase if the aggregate quarterly payout amount remains unchanged thus; as a result the payout will be divided over fewer shares.

I'll be using The PowerShares Buyback Achievers ETF (PKW) as a proxy for this analysis. PKW focuses on U.S. companies that have reduced their shares outstanding by at least 5% in the previous year and weights these holdings by market capitalization, subject to a 5% cap within the ETF portfolio. PKW may present an opportunistic niche in which to invest and potentially capitalize on a cohort of companies that engage in aggressive buyback programs, particularly in these volatile markets.

This article belongs to a three-part series focusing on navigating volatile markets while focusing on high-quality companies that pay out dividends or engage in aggressive share buybacks. This series is primarily focused on these attributes utilizing ETFs as proxies to exemplify the mitigation of downside risk while being well positioned in bull markets.

High-Level Overview

• Share buybacks can serve as an effective way to drive shareholder value via returning capital in the form of repurchasing stock

• PKW may present an opportunistic niche in which to invest and potentially capitalize on companies that engage in aggressive buyback programs

• Since inception approximately 9 years prior, PKW has provided nearly triple the return of the S&P 500 and Dow Jones

Since inception, the share buyback cohort has boasted impressive performance

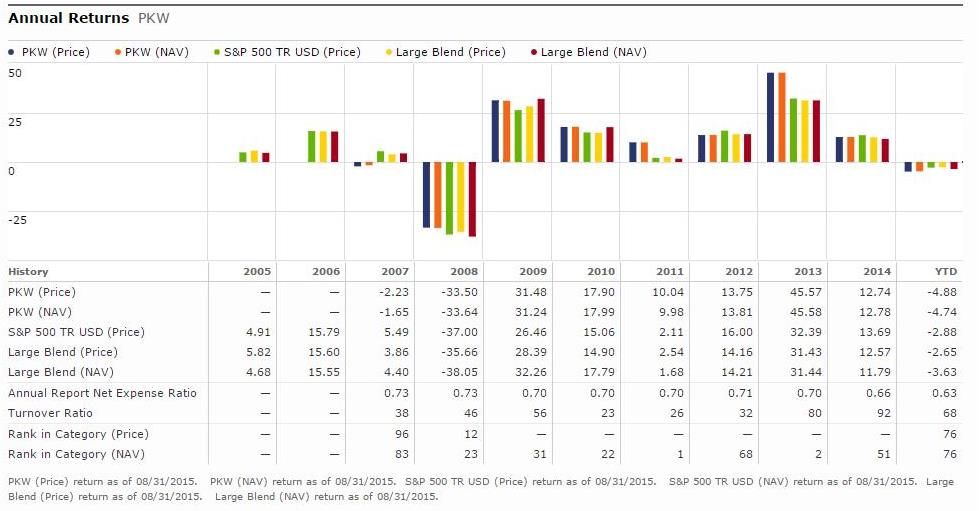

The annual returns of PKW have been impressive when compared to the broader indices (S&P 500 and the Dow Jones). Since inception, PKW has outperformed both the S&P 500 and Dow Jones by a wide margin. From 2007 thus far through 2015 the S&P 500 and Dow Jones posted cumulative returns of 36% and 31%, respectively while PKW racked up a return of 80% over the same period. This greater nearly three-fold return is largely attributable to the previous 5-year time period as the divergence in return is largely observed from 2010 through 2015 throughout the recent multi-year bull market (Figure 1). Prior to 2010, the two indices and PKW largely moved in lock-step. Since 2007, PKW has boasted average annual returns of 10.1% while the S&P 500 and Dow Jones posted annual returns of 7.9% and 7.4%, respectively (Figures 2 and 3). Outpacing the S&P 500 and Dow Jones by an annual clip of 2.2% and 2.7% respectively may not seem significant however this translates into a 27.8% and 36.5% increase in annual returns. Narrowing this timeframe to the most recent 5-year period accentuates the returns of PKW relative to the S&P 500 and Dow Jones benchmarks. PKW posted an average annual return 15.4% in comparison to 12.3% and 10.5% for the S&P 500 and Dow Jones, respectively (Figures 2 and 3). Over the most recent 5-year time period, annual returns of PKW have outpaced the S&P 500 and Dow Jones indices by 3.1% and 4.9%, respectively (Figures 2 and 3).

Figure 1 – Google Finance comparison of cumulative returns over the past 8 years for PKW, Dow Jones and S&P 500

Figure 2 – Morningstar comparison of PKW and S&P 500 annual returns

Figure 3 – Morningstar comparison of PKW and Dow Jones annual returns

This trend has continued thus far into 2015, PKW has outperformed both the S&P 500 and Dow Jones significantly as depicted in figure 4.

Figure 4 – Google finance comparison of 2015 YTD returns for PKW, Dow Jones and S&P 500

These data suggest that returns are significantly greater than the border indices when specifically focused on the cohort of companies that deploy capital primarily in the form of share buybacks and secondarily in the form of dividends. Taken together these data suggest that the cohort of companies that specifically focus on share buybacks to drive shareholder value outperform the broader indices in bull markets while potentially mitigating downside risk in bear markets as demonstrated thus far in 2015.

Driving shareholder value by combining share buybacks with dividends

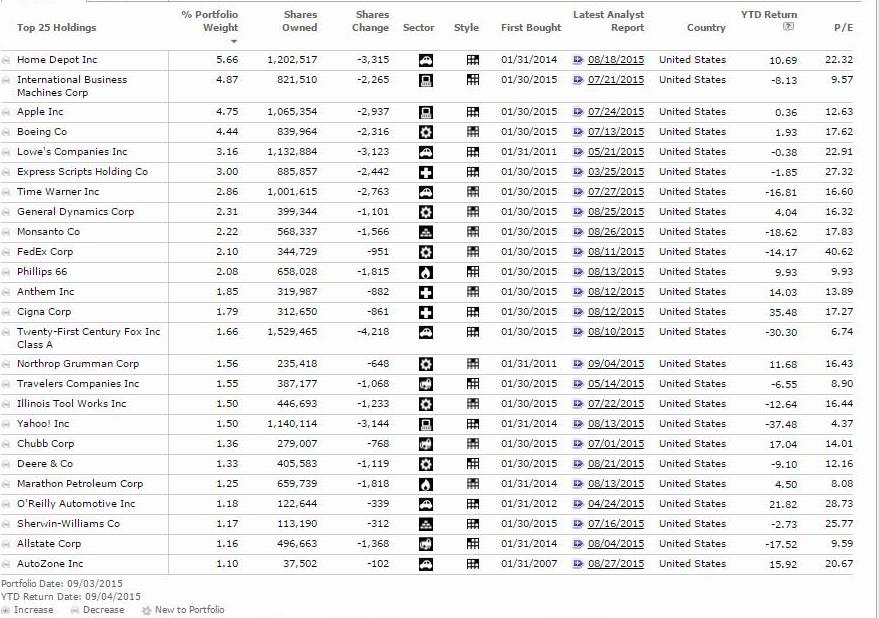

Share buybacks can be an effective alternative to paying dividends. However in some cases these programs are combined with dividend payouts. In this case, shareholders are doubly rewarded with capital returned in the form of share buybacks and a quarterly/semi-annual dividend distribution. Dividends coupled with share buybacks can serve as an effective synergy in returning value to shareholders; Apple and Home Depot are great examples of this dual capital return. PKW holdings consist of numerous companies that offer both share buybacks and dividends for maximum appreciation (Figure 5).

Figure 5 – Morningstar top 25 portfolio holdings for PKW

PKW holds stable large-cap stocks across all categories in growth, blend and value with strong cash positions for an overall category status of large value. Apple, Home Depot, International Business Machines, Boeing, Lowe's, Time Warner, Express Scripts and Monsanto comprise various holdings within the top ten. The top ten holdings comprise over a third of the entire portfolio by weight. All of these companies pay a divided with the exception of Express Scripts. Many other companies within the portfolio provide the same share buybacks and dividend combination for optimal capital return such as FedEx, Anthem, Northrop Grumman, Deere and Co., and Corning all of which pay a dividend with varying yields. Collectively, all the companies that comprise PKW translate into a current overall yield of 1.1%. This provides a competitive yield to augment the share buyback component of the ETF.

The counter argument against share buybacks

Not all companies that engage in share buyback programs are created equally and some companies have ulterior motives in initiating a repurchase program. Some leadership boards may want to increase earnings per share by purchasing and retiring shares to demonstrate an ostensibly growing business or to meet executive benchmarks, artificially. One substantive argument against share buybacks is the price itself in which the company purchases its shares. One can contend that the company of interest may be purchasing shares during inopportune times. This may occur when markets are at all-time highs, P/E ratios are higher than the historical average and PEG ratios are unfavorable at the current time. Taken together, this may potentially diminish the value of its purchases. Another substantive argument that is commonly held is the misuse of capital allocated towards these programs. Skeptics contend that these companies could better earmark capital in increasing dividends, R&D expenditures and/or acquiring competitors within its space. Considering there are share buyback companies that underperform the broader indices, it may prove to be difficult in identifying individual stocks in this area. Collective exposure across companies with varying market capitalizations via the PKW ETF may prove to be a compelling alternative.

Summary

Since inception approximately 9 years prior, PKW has provided nearly triple the return of the S&P 500 and Dow Jones. Many companies within the PKW portfolio provide the dual synergy of share buybacks coupled with dividend payouts for optimal capital return to shareholders. The third piece in this series will focus on this dual synergy and the high-quality companies that provide investors with these shareholder-friendly attributes. PKW offers a healthy rate of return with low to moderate risk exposure across the large value space. Considering the strong fundamentals and past performance with focusing on companies that return capital in the form of share buybacks and dividends, this ETF presents a compelling case to belong in any long portfolio.

Noah Kiedrowski

INO.com Contributor - Biotech

Disclosure: The author currently holds shares of Home Depot and Apple and is long both holdings. The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses.

What about TTFS? It's also a share buyback ETF?

Hi PAM

TTFS looks like another compelling share buyback ETF albeit focused more on mid-cap stocks. This could provide superior growth in bull markets as a result of its capitalization focus however it may not mitigate downswings as well as PKW with its focus on large-cap value stocks.

Thanks for reading and stay tuned for my third part in the series.

Noah