Crude prices bottomed in the current price cycle during the third week of June. Subsequently, there has been a surge to the highest crude prices in two years. My theory is that the market has priced-in a geopolitical risk premium given the de-certification of the Iran nuclear deal by President Trump as signaled by the White House on October 5th.

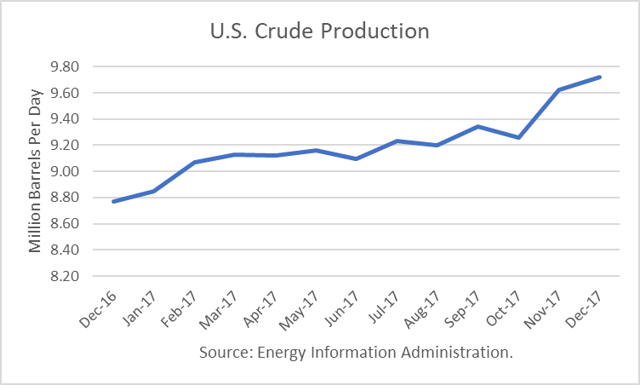

Another factor has emerged. It has become increasingly clear that the DOE’s estimates of weekly U.S. crude production have overestimated the actual monthly figures, as reported two months in arrears. The errors since April have been large. Some have concluded that American shale oil production is not as big of a countermeasure to rising oil prices as had been believed.

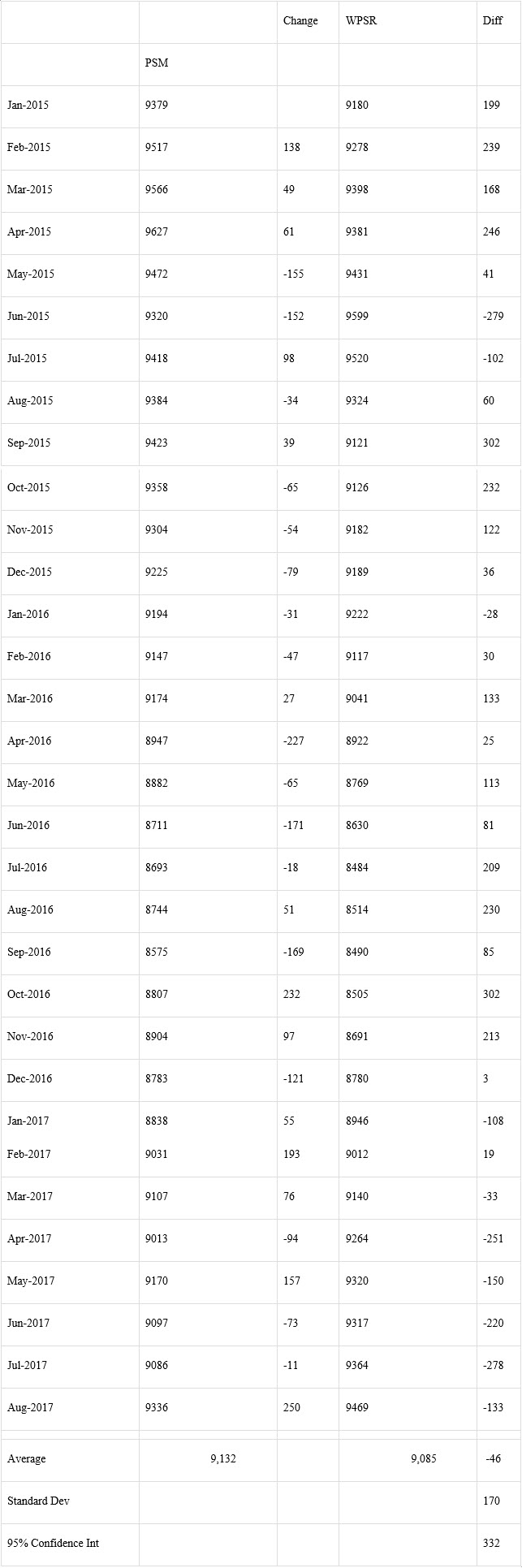

U.S. Crude Production

A closer look at the underlying production data reveals that an underperformance of shale oil production was not a major cause of the overestimation of weekly production. Unscheduled maintenance in the Gulf of Mexico (GOM) and other variations also contributed to a lull in production.

GOM production experienced unscheduled maintenance in April through June, had normal maintenance in August and September, and was impacted by Hurricane Nate in October. The DOE projects a return to levels seen in January through March during November and December.

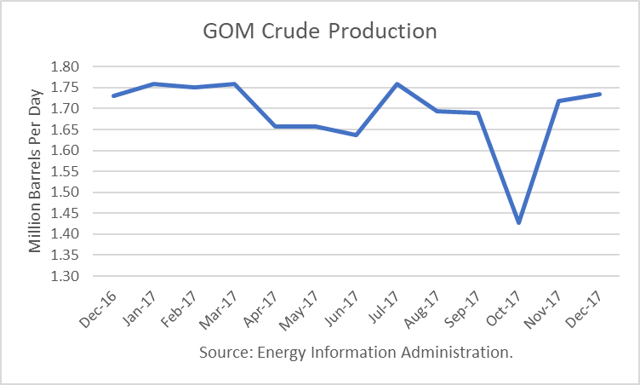

Other variations in Alaskan and non-shale oil production also affected total production.

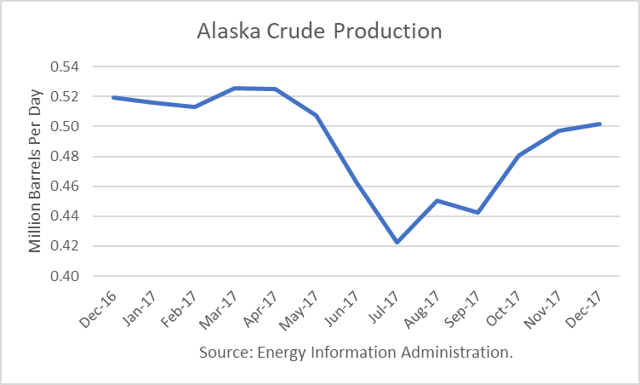

But according to DOE estimates, shale production growth has been fairly consistent, though off, some most likely due to a lagged effect of lower prices experienced in March through June.

In their Short-Term Energy Outlook (STEO) for November, the DOE projects stronger growth in production for November and December, as maintenance issues dissipate. For the first week of November, it estimated crude production at 9.620 million barrels per day (mmbd), the highest one-week figure in the database going back to 1983.

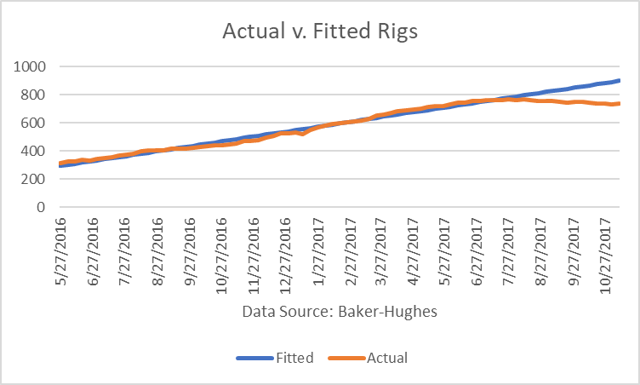

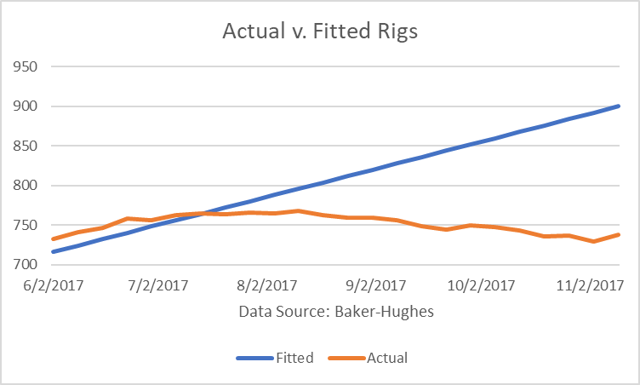

U.S. Rig Count

The Baker-Hughes oil-directed rig count had bottomed in May 2016, following the collapse in oil prices. Since then, it had been in recovery mood until August 2017. Lately, it has been dropping off, giving the market greater confidence that future shale production growth would not perform as has been expected.

However, with the rise in prices since June 2017, the rig count responded (with a lag) in the week ending November 10th with a rise of 9 to 738. Though only a one-week change, this development may signal the start of a new upward surge in rigs.

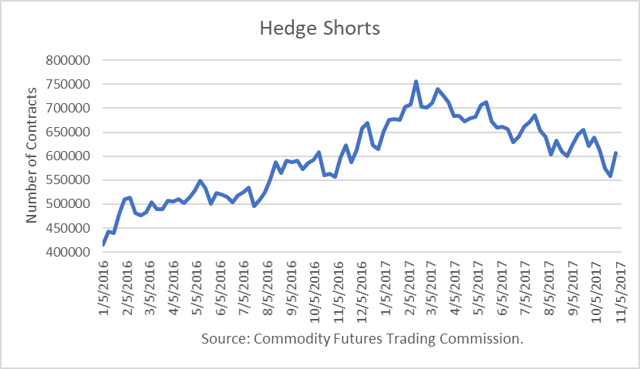

Producer Hedging

U.S. producer hedging had played a role as a substantial headwind to any sustained or significant oil price recovery. Hedge shorts had, in fact, increase significantly over the period from June 2014 through the spring of 2017.

But since mid-July 2017, producers have liquidated (bought) over 100 million barrels of its hedges back. The buying frenzy was particularly strong between the weeks ending September 19th and October 24th. But in the week ending October 31st, producers sold 48 million barrels. Perhaps crude futures prices are now high enough to induce much more hedging.

World Oil Outlook

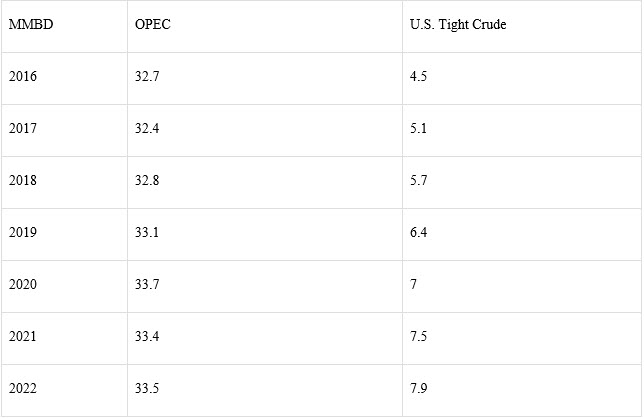

According to OPEC’s annual World Oil Outlook (“WOO”), it projects U.S. tight crude production will rise every year through 2022. At the same time, it projects the demand for its crude to be constrained not only through 2018 but for the next five years.

Last March, Saudi Energy Minister Khalid al-Falih addressed an industry conference in Houston (click here for full transcript).

Khalid Al-Falih: 'I am optimistic about the global market outlook in the weeks and months ahead' © Bloomberg

In the speech he stated:

“Saudi Arabia will not allow itself to be used by others. My colleagues have heard that privately, and I am saying it publicly. This is for the benefit of all and needs to be achieved by the contributions of all," he said. "But this time around, we made it clear that we will not bear the burden of 'free rides,' and both groups are reinforcing one another through voluntary management of their production."

He made it clear that the production cuts were designed as a short-term tool, not a long-term strategy.

“…History has also demonstrated that intervention in response to structural shifts is largely ineffective, and I believe we've learned that lesson. That's why Saudi Arabia does not support OPEC intervening to alleviate the impacts of long-term structural imbalances, as opposed to addressing short-term aberrations such as financial crises, economic recessions, unforeseen supply disruptions, or the like."

And so his statements and OPEC’s outlook begs the question of whether KSA would favor limiting OPEC production over the next five years (as implied by demand) while allowing shale oil producers to capture a significant growth in market share.

Conclusions

The recovery in oil prices, which had its highest close on Monday, has created a euphoria among investors and columnists who had lost a great deal of their capital in oil equities since 2014 or were proven to be wrong as prognosticators. A good example of the latter was an article published Monday announcing that the bull trend in oil prices "had just begun."

The upcoming OPEC meeting and a showdown between the U.S. and Iran on the nuclear deal can keep prices from dropping much through year-end. But assuming the U.S.-Iran issue is resolved peacefully, and the seasonal decline in demand takes hold in January, coupled with inventory builds, producer hedging, higher rig counts, and rising shale oil production, the price bubble is likely to burst.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

The price needs to increase AND demand needs to shrink if we aren't going to drive ourselves into extinction.

Since the price rally has occurred, which apparently caught the bears flat-footed, the IEA has rushed to the rescue with another of their patently pessimistic forecasts, the likes of which have been proven to historically be strong on underestimating demand and overestimating supply. But it makes for good bear bait. The fact is from 2007 to 2017 global demand went from 86.3 mmbopd to 98.2 mmbopd, or about 1.2 mmbopd/year increase average. We'll be at 100 mmbopd demand by the end of 2018 and will probably need north of 110 mmbopd by 2027. That's not coming out of thin air and it isn't going to materialize for $45 -$50/bbl, either. The American oil industry is running in place at the aforementioned prices and it isn't going to add the kind of supply we'll need out of the goodness of their hearts. Oil prices are going up because they have to go up to incentivize the work it will take, and the profit it will take, to reach those production numbers in the future.