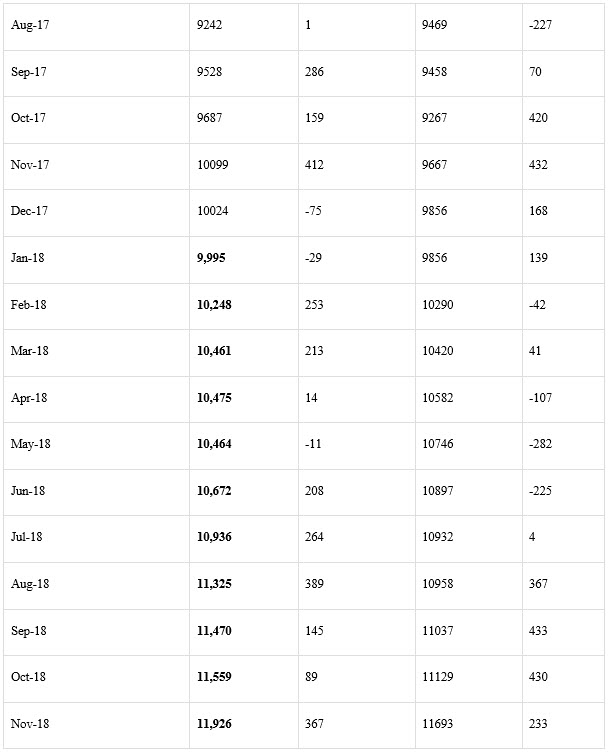

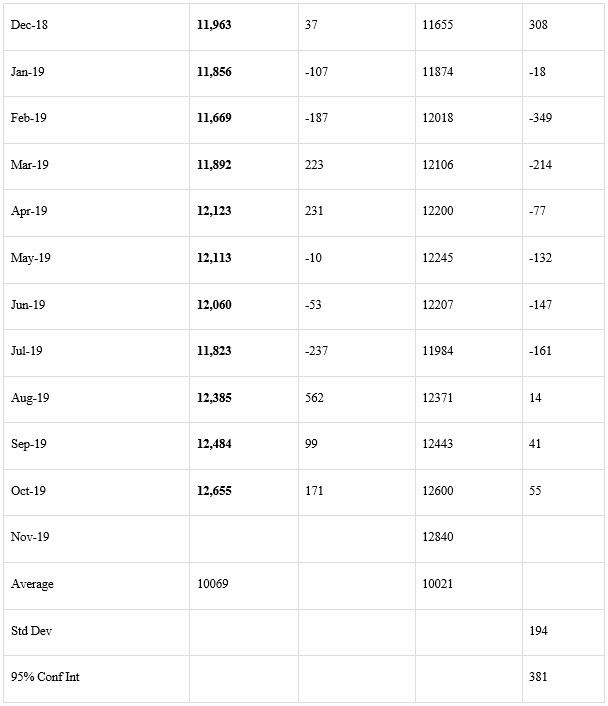

The Energy Information Administration reported that October crude oil production averaged 12.655 million barrels per day (mmbd), up 171,000 b/d from September. In addition, the September estimate was revised 21,000 b/d higher, and so the total gain was 192,000 b/d from the prior estimate.

Texas production reached a new high of 5.273 mmbd, up 53,000 b/d from September. Other gains were 70,000 b/d in North Dakota, 39,000 b/d in Colorado, and 26,000 b/d in Alaska.

The gain in North Dakota established a new high for the state. The Gulf of Mexico remained about 100,000 b/d below the August high.

Plains All American Pipeline LP’s (PAA) Cactus ll pipeline was expected to ship at full capacity, 670,000 b/d, beginning in September. EPIC Midstream’s crude oil pipeline began shipping 400,000 b/d. It is designed to ship 440,000 b/d from the Permian and another 150,000 b/d from the Eagle Ford.

Phillips 66 Partner’s Gray Oak pipeline is expected to ship an additional 900,000 b/d. It began shipments and is expected to be in full service by the end of the first quarter of 2020.

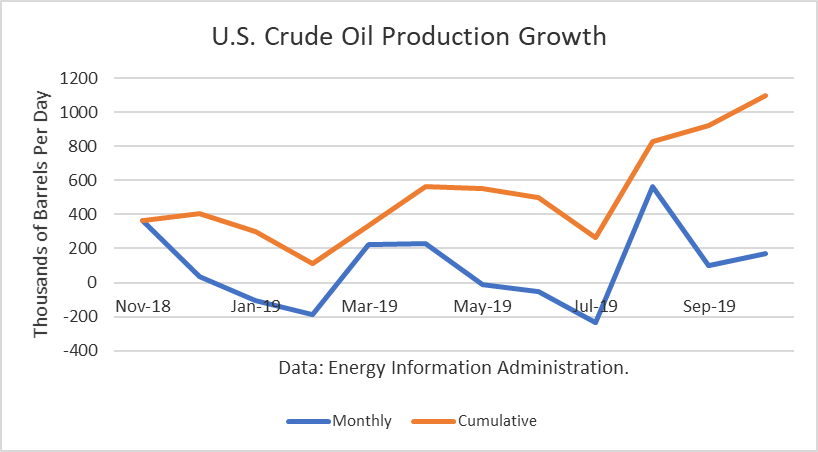

The gains from last November have amounted 1.096 million b/d. And this number only includes crude oil. Other supplies (liquids) that are part of the petroleum supply add to that. For October, that additional gain is about 600,000 b/d.

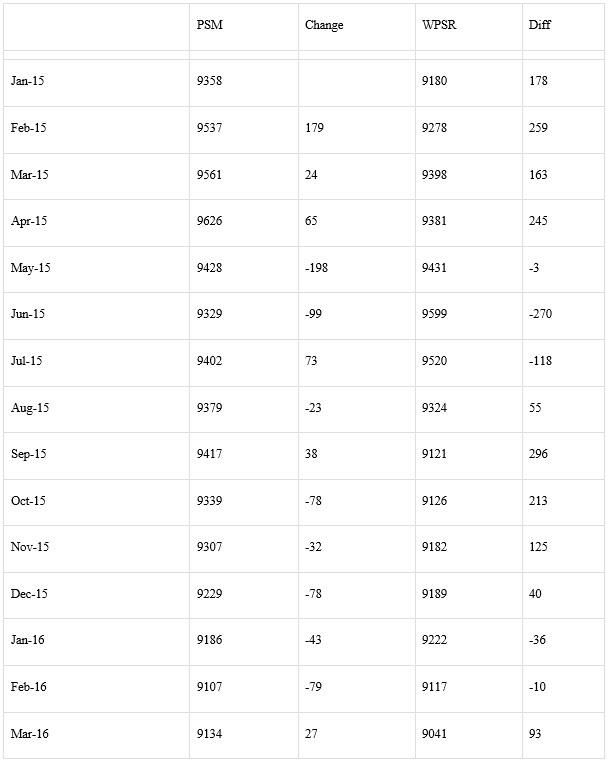

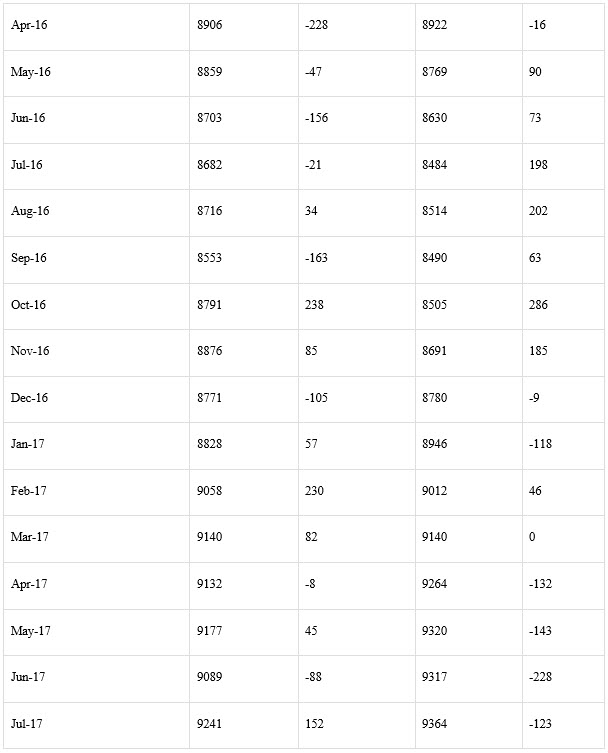

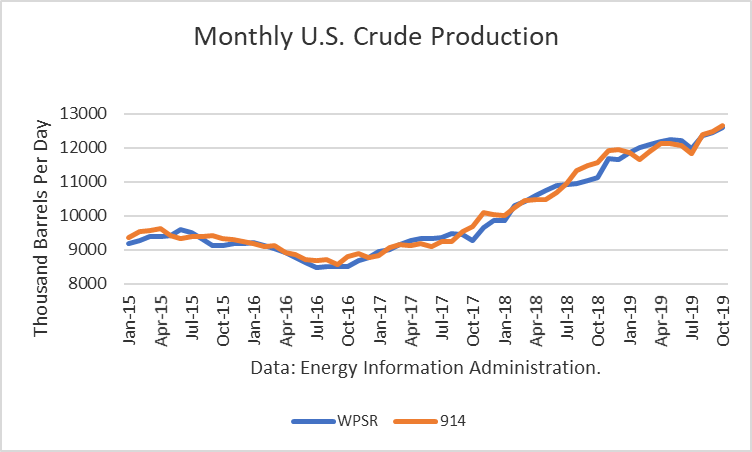

The EIA-914 Petroleum Supply Monthly (PSM) figure was 55,000 b/d higher than the weekly data reported by EIA in the Weekly Petroleum Supply Report (WPSR), averaged over the month, of 12.600 mmbd.

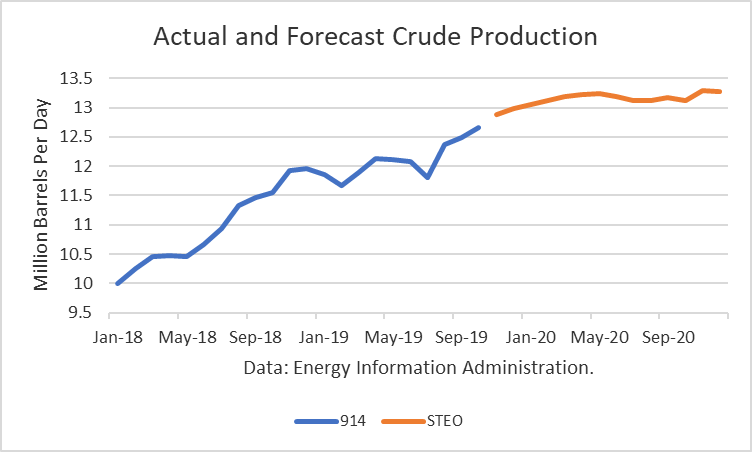

The October figure was about 93,000 b/d lower than 12.750 mmbd estimate for that month in the November Short-Term Outlook. The 100,000 b/d drop in the Gulf of Mexico from August accounts for all of that difference. And so that implies no need for another upward “rebenchmarking” to EIA’s model in future crude production levels at this time since the difference was not large enough to warrant it.

The EIA is projecting that 2019 production will exit the year at 12.99 mmbd. For 2020, the EIA is projecting an exit at 13.28 mmbd.

Conclusions

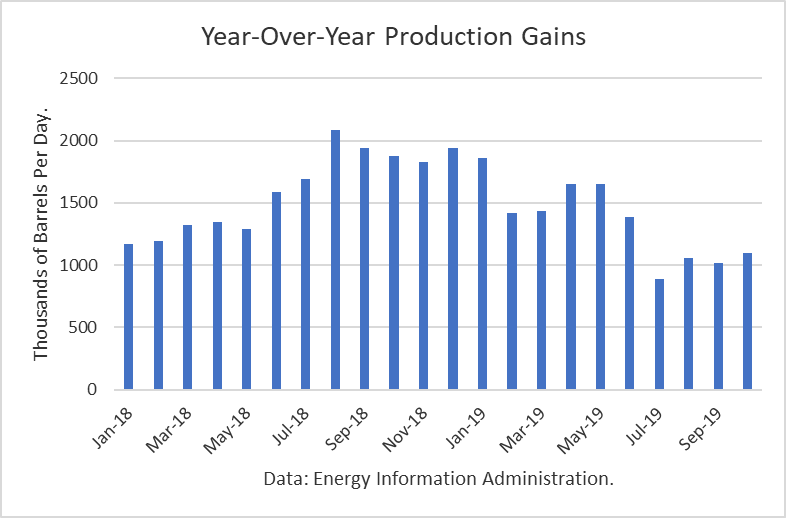

The strong gain in October adds to the rises in August and September, refuting the theory that U.S. production gains have slowed substantially. And gains in Texas owing to the opening of the three pipelines have yet to contribute the rise that I expect to see, once production costs have been effectively lowered, taking into account delivery costs to the U.S. Gulf. And with a rebound in the GOM of about 100,000 b/d, the narrative may change from one of slowing growth.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.