It’s been an ugly week for the major market averages, with the S&P 500 (SPY) continuing its violent decline from its Q1 highs. Prior to this week, the Gold Miners Index (GDX) was a sanctuary from the turbulence, but when the market heads past the 15% correction mark, few stocks are sheltered from the turbulence. While this has been painful for investors that chased miners in early Q2 near their highs, this is set up an excellent buying opportunity for patient investors. So let’s look at a few names in the GDX where the selling looks to be overdone:

Over the past month, we’ve seen several gold miners slide more than 25% from their highs, and in many cases, these corrections are entirely justified. This is because several producers have weak balance sheets and high costs, making them very sensitive to weakness in the metal price and rising interest rates. However, when it comes to names like SSR Mining (SSRM), Yamana Gold (AUY), and Barrick (GOLD), which are sitting in net cash positions or expect to be net-cash positive by Q4, the recent pullback makes little sense, especially given that they’re some of the best operators sector-wide.

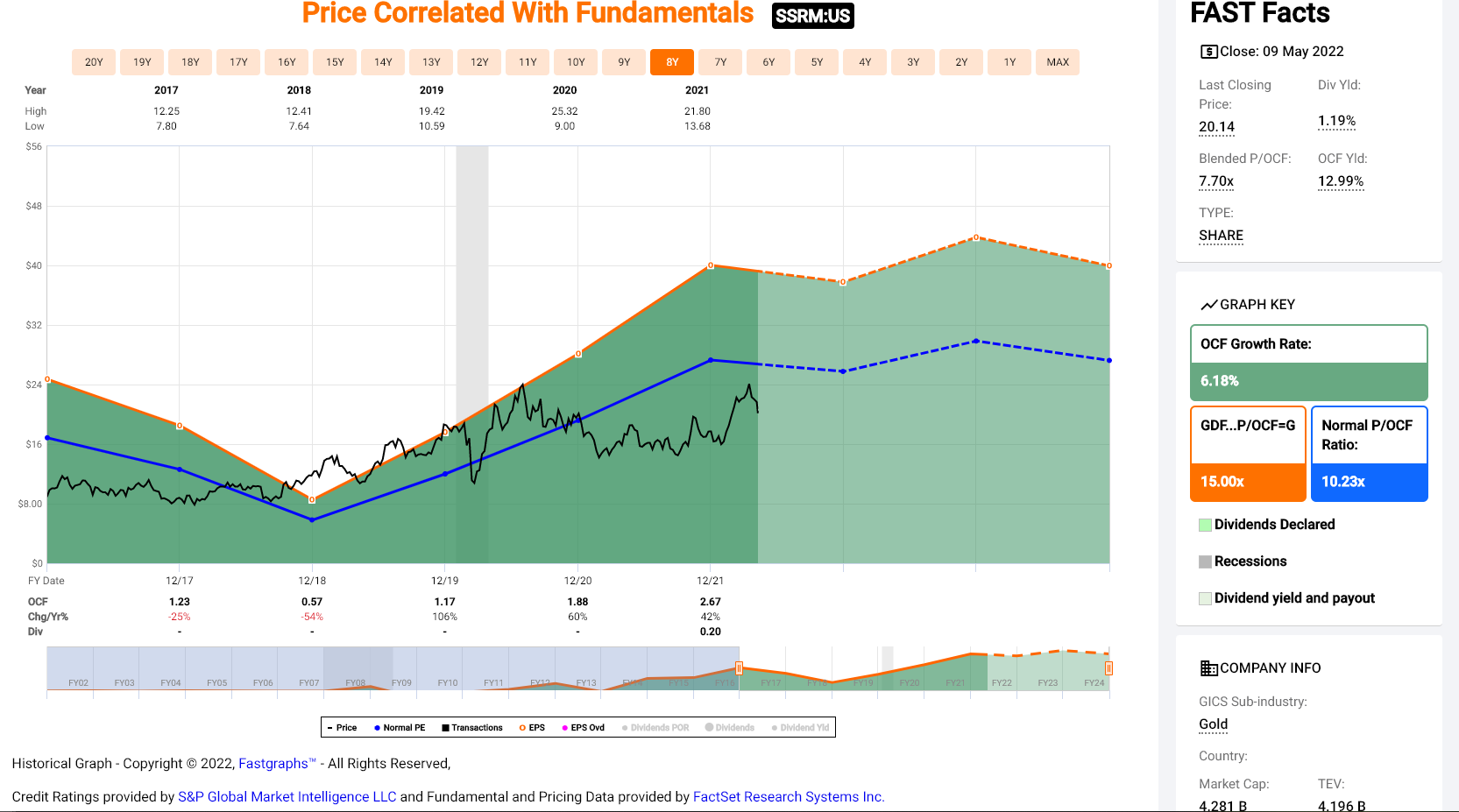

Beginning with SSR Mining (SSRM), the company released its Q1 results last week, reporting quarterly production of ~173,700 gold-equivalent ounces [GEOs], a 12% decline from the year-ago period. The stock has since sold off sharply due to its silver exposure at its Puna operations, the weaker gold price, and the view that this was a miss given the lower production at higher costs. However, this slow start to the year was largely expected due to mine sequencing, meaning that its 2nd largest asset (Marigold) will be chewing through lower-grade ore in H1 before seeing a significant increase in production in H2. Therefore, it should have no problem meeting its annual guidance mid-point of 740,000 GEOs, even if that looks quite difficult, with Q1 contributing just 23.4% of yearly ounces.

Meanwhile, from a cost standpoint, SSR Mining’s costs soared to $1,093/oz (Q1 2021: $970/oz), but this was largely a function of the lower gold sales. Notably, these costs are trending well below the annual guidance mid-point of $1,150/oz, especially with this being one of the higher-cost quarters. Hence, assuming it continues, this short-term overreaction looks like it could be setting up a buying opportunity. This is because I see a fair value for SSR Mining of $24.40, which is based on 9x FY2022 cash flow estimates and is a conservative multiple, given that it’s below SSRM’s historical multiple. So, if the stock were to decline below $18.30, where it would trade at a 25% discount to fair value, I would view this as a buying opportunity.

Barrick (GOLD) is the second high-quality name that’s recently been punished. It is the world’s 2nd largest gold producer, with more than ten operations globally, and its largest mining hub resides in Nevada. Like SSR Mining, Barrick had a slow start to 2022 with the production of just ~1.0 million ounces of gold, a ~10% decline from the year-ago period. However, the higher gold price picked up most of the slack, and as the year progresses, production is expected to increase meaningfully. Meanwhile, if we look ahead to FY2023, annual production should see a boost from its Cortez Mine Complex in Nevada and the restart of its Porgera Mine in Papua New Guinea, which has been in care & maintenance. For this reason, the H1 2022 year-over-year production decline is not that relevant to the big picture.

When it comes to the big picture for Barrick, the company has recently seen a massive upgrade to its investment thesis. This includes the decision to begin advancing the mammoth-sized Reko Diq Project in Pakistan, which was previously shelved. This asset could produce more than 150,000 ounces of gold per annum and more than 250 million pounds of copper per annum, translating to $1.4BB in additional annual revenue attributable to Barrick later this decade based on current metals prices. Assuming Reko Diq and Donlin are green-lighted, this could transform Barrick from a no-growth company to a company with some production growth, which is hard to find in the 2.0+ million-ounce producer space.

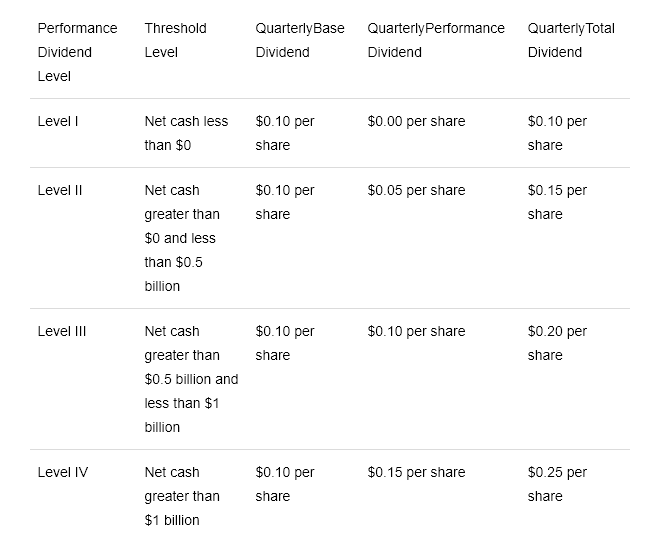

At the same time, Barrick has unveiled a buyback program to boost shareholder returns and a new dividend framework (shown above). This led to a more than 100% increase in the quarterly dividend sequentially in Q1 2022, giving investors another reason to hold the stock. So, with Barrick having a more attractive long-term production profile and a more than 3.0% dividend yield, I see this pullback as a buying opportunity.

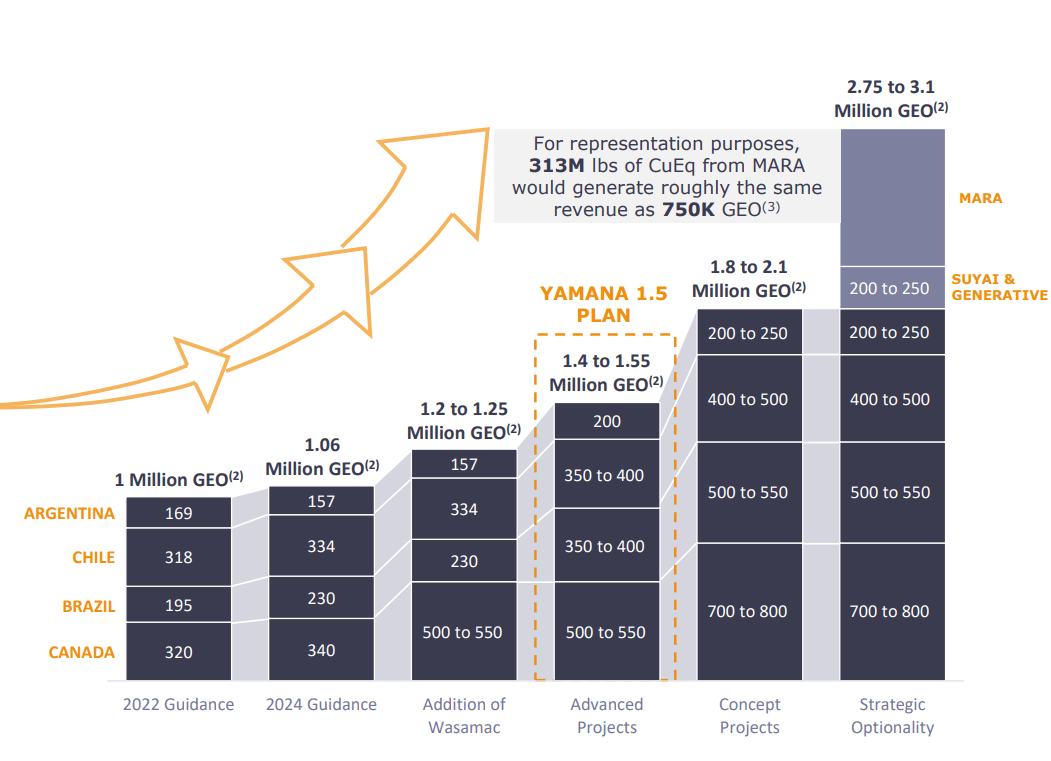

The final name worth paying close attention to is Yamana Gold (AUY), a 1MM ounce per annum producer with mines in Brazil, Canada, Chile, and Argentina. Over the past several years, Yamana has seen a significant transformation, divesting its copper asset to help improve its balance sheet and focusing on its core gold operations. This has paid dividends, with the company steadily growing production at its low-cost ($750/oz) Jacobina Mine in Brazil and adding a key asset, Wasamac, which could produce more than 200,000 ounces of gold per annum beginning in 2026.

The two critical differentiators for Yamana are its updated growth and its cost profile. From a growth standpoint, Yamana is confident that it can grow production by 50% to 1.5MM GEOs by 2030, but there’s an upside to 2.3+MM GEOs per annum if its MARA Project (~60% ownership) comes online. Meanwhile, from a cost standpoint, its relatively high-grade underground mines have allowed it to skirt past most inflationary pressures, using less diesel, less labor, and lower consumables per ounce produced than its peers. This makes AUY my favorite idea in the gold space, and I see this pullback towards $5.00 as a buying opportunity.

Yamana, Barrick, and SSR Mining are three ways to play the sector with high-quality operators that pay attractive dividends, and they typically under-promise and over-deliver. Given that these companies are back on the sale rack, I would expect any further weakness to present a buying opportunity.

Taylor Dart

INO.com Contributor

Disclosure: This contributor held a long positions in AUY and GLD at the time this blog post was published. This article is the opinion of the contributor themselves. Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.