Analysis prepared on March 19, 2018

The relative rate of growth in supply v. demand will ultimately determine stock levels and prices. And the three key predicting agencies, the International Energy Agency (IEA), Energy Information Administration (EIA), and OPEC have different views on what is likely to unfold.

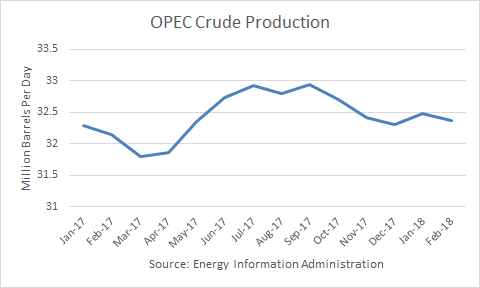

OPEC does not often predict is own production, but in December it forecast it would average 33.2 million barrels per day (mmbd) during 2018. That would far exceed its projected “call on OPEC oil,” which is world demand minus non-OPEC production. For 2018 as a whole, it predicts that figure will be 33.1 mmbd.

That demand for OPEC oil is based on a gain in demand of 1.52 mmbd and a rise in no-OPEC production of 1.15 mmbd. In my view demand is likely to be a bit stronger due to world economic growth. However, the non-OPEC supply number is much too low, given the recent rise in U.S. production of 886,000 b/d from August through November. (December production was down a bit for seasonal reasons.) Furthermore, U.S. production has yet to respond to $60/b. The rise in output last autumn was a response to $50/b.

The EIA has the most aggressive non-OPEC production estimate of a gain of 2.5 mmbd, with 2.0 occurring in the U.S. alone, and the balance in Canada and Brazil. The EIA forecast is based on a gain in crude production of 1.5 mmbd and a rise in other liquids of 500,000 b/d. WTI did not exceed $60 in any month since 2015 until January 2018. And the year-over-year gain in March 2018 is estimated to be 1.29 mmbd. And so the industry’s response to $60/b could very well enable the 1.5 mmbd gain.

The EIA’s estimate for demand is a rise of 1.7 mmbd, which I find to be realistic. But if non-OPEC supply is up 2.5 mmbd and OPEC production remains at February's 32.3 mmbd, then global inventories will rise by 80 million barrels throughout 2018.

The IEA estimates are in-between OPEC’s more bullish and EIA’s more bearish outlooks. It forecasts a demand gain of 1.4 mmbd and a supply gain of 1.7 mmbd. If OPEC production remains at 32.3 mmbd, stocks will neither rise nor fall, on balance, throughout the year.

Here are some other factors to take into consideration.

U.S. Exports and Inventories

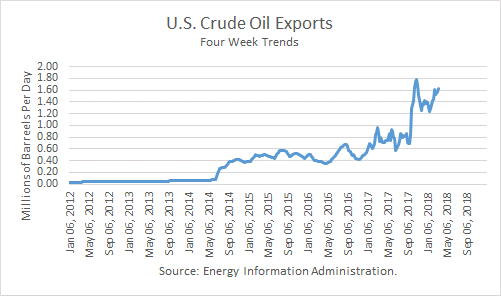

One major reason U.S. crude stocks have not built by much during this refinery maintenance period has been high crude exports.

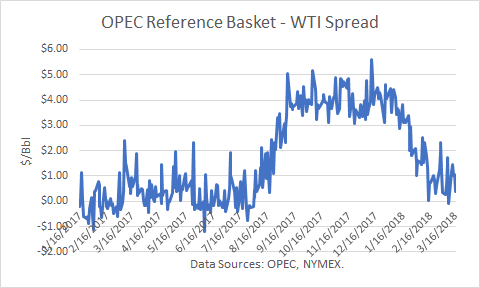

But the OPEC Reference Basket (ORB) – WTI spread has collapsed, and that should reduce crude exports to China.

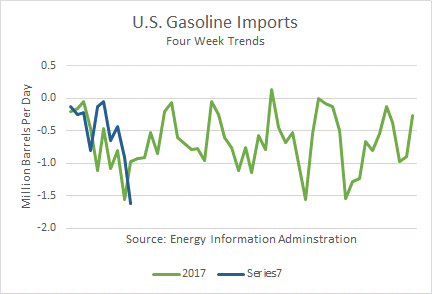

In addition, gasoline exports should drop soon, and that should enable gasoline stocks to build.

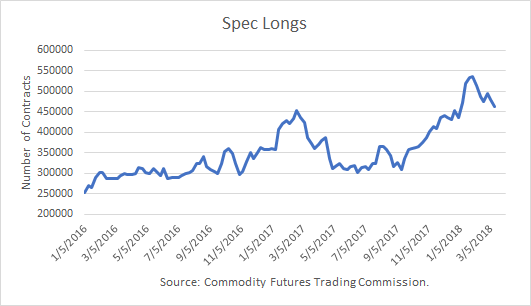

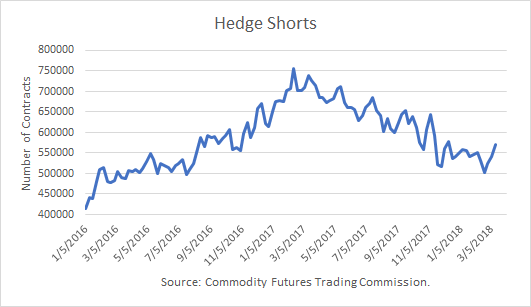

Sentiment

Crude prices peaked in late January, and bullish spec positions have been reduced slightly.

Also, oil producer hedging positions have been on the rise.

In both cases, there is a lot more room for selling to get them back to a more neutral position, which I expect if inventories build as indicated above.

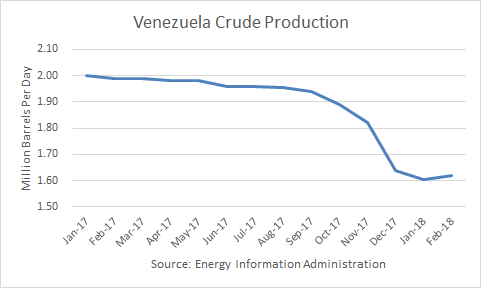

Venezuela

One big risk is production in Venezuela. Production had dropped by 370,000 year-over-year in February, and a further deterioration should be expected, unless it can secure loans from China or Russia.

Furthermore, the Trump Administration is contemplating additional sanctions, which could include an oil import or export embargo, which may cause a collapse of the country’s oil industry. But such an action would also cause a further humanitarian crisis, and the lesson of unintended consequences from U.S. foreign intervention (Iraq) has not been lost.

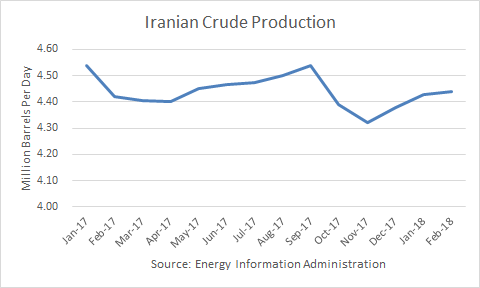

Iran

The Administration is also considering imposing sanctions on Iran, and recertification of Iran’s compliance with the nuclear deal is required in May. But a report on Friday stated that France, Britain, and Germany would favor new sanctions if the U.S. remained in the deal.

Iran has also signed a new deal with Russia to invest in the development of oil reserves in its country. And so it appears that new sanctions are unlikely to affect Iran’s production this year.

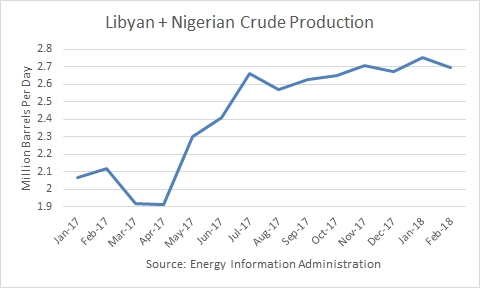

Libya and Nigeria

Production in Libya and Nigeria is always at risk due to domestic terrorists. However, recent production for the two African countries have been relatively steady at 2.7 mmbd, and both are working toward increases, as they are not included in the OPEC production deal.

Russia

Despite speculation that Russia may exit the deal early, Energy Minister Novack has most recently affirmed that Russia remains committed until the market is balanced.

Interest Rates and Dollar

The Fed has indicated that it may raise interest rates by four or five times this year.

If it does, that will support the dollar and act as a headwind for commodity prices.

Stock Market

Higher interest rates may also adversely affect the stock market, which in turn, can have collateral damage on oil equities and prices. The stock market peak in January remains in place, and so we may see further consolidation in equity prices during 2018.

Conclusions

The most important factor in the outlook is that U.S. shale production has yet to respond to the $60/b oil environment. There are 3-4 month lags in drilling and another 3-4 months lags in production from the higher drilling rate. As production reflects the higher price, the market sentiment could turn highly bearish because the OPEC deals have backfired.

The most important bullish factor has been the relatively slow build in stocks for this time of year. Also, further erosion of production in Venezuela could offset new shale production to a greater or lesser degree.

In the very short term, I expect lower crude and gasoline exports to enable U.S. stocks to increase. If that happens, I expect WTI to dive back to the $55 to $56 price area.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

It's good to know that somebody believes the letter agencies numbers. There's certainly no reason to believe what any country's government says. Also, the publicly traded companies lie to keep their stock up. What does WTI at $60 mean? Why don't you quote actual field prices for all the US producing areas? No one I know gets WTI. The 40 gravity oil I produce is at about $55.90. The money to be made on oil is in the futures market, where no one has to make or take delivery.