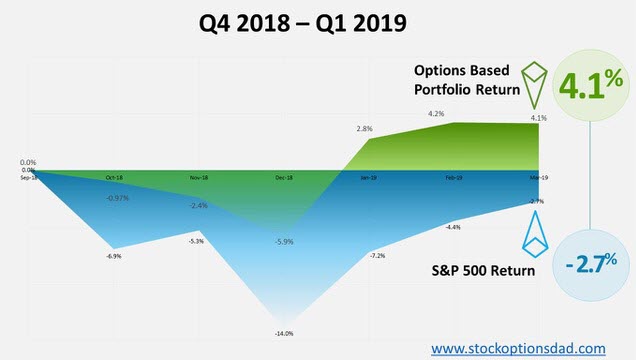

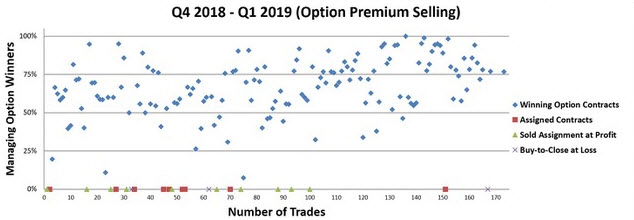

131 wins out of 151 trades later, through the Q4 2018 bear market and the Q1 2019 bull market, high-probability options trading thrives regardless of the market backdrop. Options trading is powerful because you can be wrong about the direction of a stock and still make money. Hence how I was able to achieve an 87% success rate as the market witnessed dramatic moves over the past 6 months. In Q4 2018, the S&P 500 sold off 14% and erased all of its gains for the year. The start to 2019 posted its best January in over 30 years and rounding out the quarter with a return of ~12.7%. In this article, I’ll be discussing how options trading can generate consistent income with a high-probability of success, regardless of market conditions. This is accomplished since options are a bet on where stocks won’t go, not where they will go. Following the options trading framework described in this article, my options-based portfolio resulted in a total portfolio return of 4.2% against the S&P 500 return of -3.1% over the previous 6 months. This timeframe provided both bear and bull market conditions to demonstrate the effectiveness and resiliency of options trading while outperforming the broader index by a wide margin. This seesaw from a negative to a positive market backdrop provided unique opportunities to capitalize on options trading. In Q4 2018, during the bear market, I was able to achieve a 79% options success rate by closing 66 out of 84 option contracts for wins. In Q1, during the bull market, I was able to achieve a 97% options success rate by closing 65 out of 67 option contracts for wins. Taken together, options provide a margin of safety, enabling your portfolio to mitigate risk, provide consistent income and hedge against market volatility. Options have a unique attribute since you can still be successful while generating income even if you’re wrong about the direction of the stock.

Managing Risk

Options trading can serve a great tool in managing portfolio risk as you determine your success rate. If you want to be successful in 70%, 80% or even 90% of your trades, options trading enables you to select your level of success. This, of course, comes with the trade-off of lower premiums received as the success rate elevates. Risk mitigation is particularly important for smooth and consistent portfolio gains while circumventing market wide melt-downs (i.e., Q4 of 2018). Maintaining cash on hand to engage in covered put option selling is a great way to collect monthly income via premium selling. Conversely, selling covered calls on long-term or assigned stock positions is a great way to lower the cost basis and generate consistent income as well. Focusing on implied volatility, implied volatility rank and probabilities, one can optimize option selling to yield a high probability win rate over the long term given enough trade occurrences. In the end, options are a bet on where the stock won’t go, not where it will go and collecting premium income throughout the process. These empirical data demonstrate that the probabilities play out given enough occurrences over time regardless of market condition. Over the past 6 months and 151 trades, an 87% success rate was achieved while outperforming the broader market by a widespread (S&P -4.4% vs. 4.2%).

Results

A wide array of options in different sectors with different expiration dates will ensure portfolio diversity and plenty of opportunities to take profits. I traded 62 different tickers that included stocks and ETFs while being agnostic to any particular sector or underlying stock. Over the past 6 months, my longest winning streak was 50 trades, my average contract length was ~10 trading days, and my average income per trade was $67. Out of 151 trades in a period where the market witnessed both bear and bull market scenarios, an 87% win-rate was achieved while outperforming the broader market by a wide margin. Accounting for all the contract income, assigned underlying positions that were relinquished at a profit and unrealized losses (total portfolio) yielded a return of 4.2% while the broader S&P 500 posted a return of -4.4% (Q4 2018 through Q1 2019).

Figure 1 – Graph displaying all cumulative returns over the previous 6 months as compared to the S&P 500 demonstrating the effectiveness of options trading in both bear and bull markets

Figure 2 – Details for options trades that were executed over the previous 6 months displaying 60% premium capture and 87% option contract success rate

Figure 3 – Details for options trades that were executed over the previous 6 months displaying 62 unique tickers traded with an average income per trade of $67

Figure 4 – Detailed trade ledger with outcomes of each trade and profit realized (e.g., if an option is sold for a net premium of $100 and then managed for a buy-to-close for a net of $10 then a 90% net realized gain is logged)

Leveraging Implied Volatility (IV) Rank

The main keys for options trading success are leveraging implied volatility and time premium decay. Markets predict how volatile stocks will be into the future via implied volatility. Implied volatility (IV) is the expected volatility of a stock over the lifecycle of the option contract. IV is influenced by supply and demand of the underlying options and by the market’s prediction of share price movement. As the expectations rise and demand for the options increase, IV will rise. Historically, this predicted volatility always overestimates actual volatility, and it’s this overestimation that can be exploited to the benefit to option sellers.

This is where IV Rank comes into play and how this is the most critical variable in options trading and its success. IV Rank is a measure of current implied volatility against the historical implied volatility range (IV low – IV high) over one year. Let’s say the IV range is 30-60 over the past year. Thus the lowest IV value is 30, and the highest IV value is 60. We need to compare the current IV value to this range to understand how the current IV ranks about its historical IV range. If the current IV value is 45, then this would equate to an IV Rank of 50% since it falls in the middle of this range. Alternatively, if the current IV value is 55, then the IV Rank is 83%.

When IV Rank approaches a value of greater than 50%, then option sellers can use this to their advantage to take in rich options premium with the expectation that this implied volatility will decrease. Any value above the 50% threshold is where the overestimation of actual volatility thrives. Selling options in these high IV Rank situations serve as a two-fold benefit since time premium is always decaying and IV will likely revert to its mean and fall. Even if the stock moves up, down or trades sideways without breaking through the strike, the option will be profitable as time and IV fall.

The high IV Rank provides rich premium and as the option lifecycle unfolds and this volatility decreases, the option time value implodes, and the option decreases in value allowing profits to be released earlier in the lifecycle without waiting until the expiration of the contract.

Trading Mechanics

- Sell option contracts one standard deviation out-of-the-money to theoretically yield an 85% probability of closing the trade at a profit at expiration

- Selling options in underlying securities that possess high implied volatility rank (greater than ~50% percentile)

- The vast majority of contracts are sold ~30 days out in duration

- I execute a buy-to-close order on all my positions around ~60% or greater profit to realize my gains and accelerate the closure of the contract to free up capital for additional positions

- If a contract is assigned, then I will hold onto the shares until the position rebounds until I can relinquish these shares at a profit

- I may sell covered calls to mitigate losses on assigned positions

- I trade a wide variety of tickers in both stocks and ETFs across all sectors while being agnostic to any particular sector or underlying security

- Position sizing typically ranges from 3%-6% of the portfolio for each trade, and I elect any dividends from assigned contracts to be paid out in cash

- All data presented account for commissions/fees; thus all numbers are final net values after backing out trading fees

Conclusion

Sticking to the mechanics of selling options with high IV rank and a strike price one standard deviation out-of-the-money, an expected ~85% probability of success over the long-term given enough trade occurrences plays out. As volatility decreases in conjunction with time decay, the option contract will decrease in value providing the option seller with the potential for realized gains early in the option lifecycle. Taken together, this translates into high probability options trading to maximize option outcomes regardless of directionality and market backdrop. Despite the bear and bull market scenarios over this 6-month timeframe, I was able to outperform the S&P 500 by a healthy margin (4.2% versus -4.4%). This seesaw of a market provided a true test to the high probability trading and durability of this options trading method and yielded an 87% success rate. These empirical data demonstrate that the probabilities play out given enough occurrences over time with varying market backdrops. Options are a bet on where stocks won’t go, not where they will go while generating consistent income and mitigating risk.

Want to learn more? Check out my previous articles here and here.

Thanks for reading,

The INO.com Team

Disclosure: The author holds shares in AAPL, AMZN, DIA, GOOGL, JPM, MSFT, QQQ, SPY and USO. The author has no business relationship with any companies mentioned in this article. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned.

Do you use vertical spreads in your option selling, or how much of it is 'naked' option selling (e.g. cash or margin-secured)?

Thanks!

Mike, you are right. There is no self-promotion that is 100% honest. The winners are shown, the losers are hidden. The pluses are sticking in your eyes but the minuses are shied away and never reflected.

The emphasis on percent winning trades is nice psychologically, but says nothing about profitability. This has been discussed forever in the trading community, so it's a little disappointing to still see this kind of "hype". A mechanical approach to option selling based on the greeks will almost always lose money. The only thing that can save such a strategy is effective risk management. Option veterans know from whence I speak.

Yep, that's the Tasty Trade method in a nutshell! Oh, you probably should mention that a lot of times your losers will be much bigger than the winners, otherwise people will think the "85% winners" equals a winning trading method.