In an early episode of The Simpsons, “Homer Defined,” Homer saves the nuclear plant from meltdown by randomly pushing a button on the control panel. Soon “to pull a Homer,” meaning to “succeed despite idiocy," becomes a popular catchphrase.

Is that what happened last week? Did Jerome Powell and the Federal Reserve inadvertently “pull a Homer” by helping to create a bank panic that actually might accelerate their desire to slow down the economy? That might not have been their intention, but it sure looks like it.

At least it does to former White House adviser and Goldman Sachs President Gary Cohn (although he didn’t reference The Simpsons).

"We're almost getting to a point right now where he's outsourcing monetary policy," Cohn told CNBC, referring to Powell. “I don't believe they [the banks] are going to loan money, or as much money, and therefore we're going to see a natural contraction in the economy.”

Minneapolis Fed president Neel Kashkari said basically the same thing on CBS’s Face the Nation Sunday.

"It definitely brings us closer [to recession]," Kashkari said. "What's unclear for us is how much of these banking stresses are leading to a widespread credit crunch. That credit crunch ... would then slow down the economy.”

Now, I sincerely doubt that the Fed deliberately phonied up a banking panic in order to put the brakes on the economy.

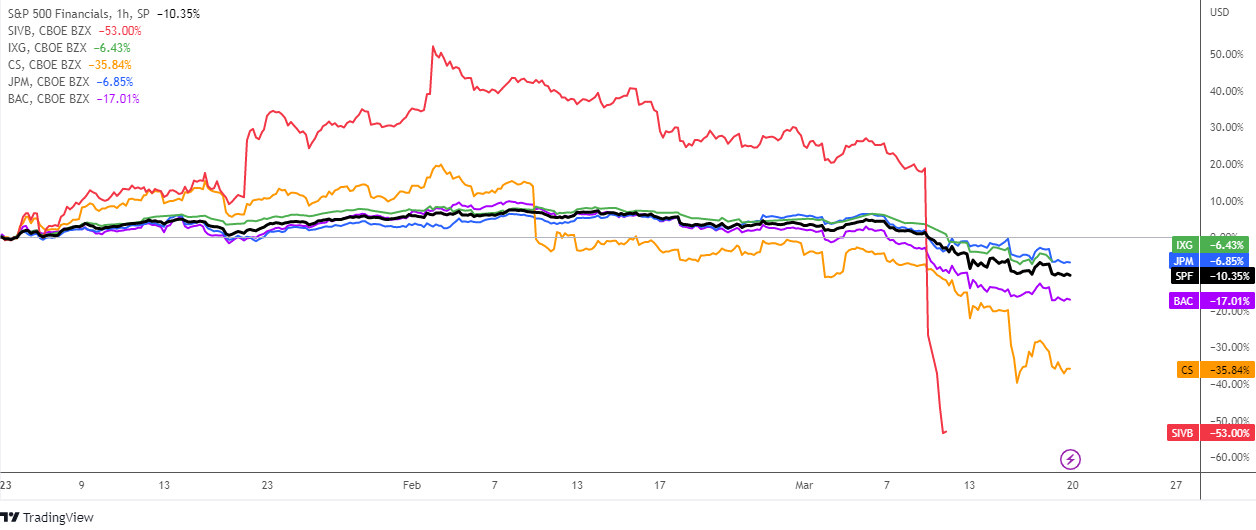

Just the same, though, it certainly did play a major role in creating one not just through monetary policy — by raising interest rates so high and so fast — but also through neglect.

Just as it did in the road leading up to the global financial crisis, the Fed allowed problems at several banks it regulated to reach the point that generated an electronic run on deposits and the banks’ eventual failure. Continue reading "Did The Fed "Pull A Homer"?"