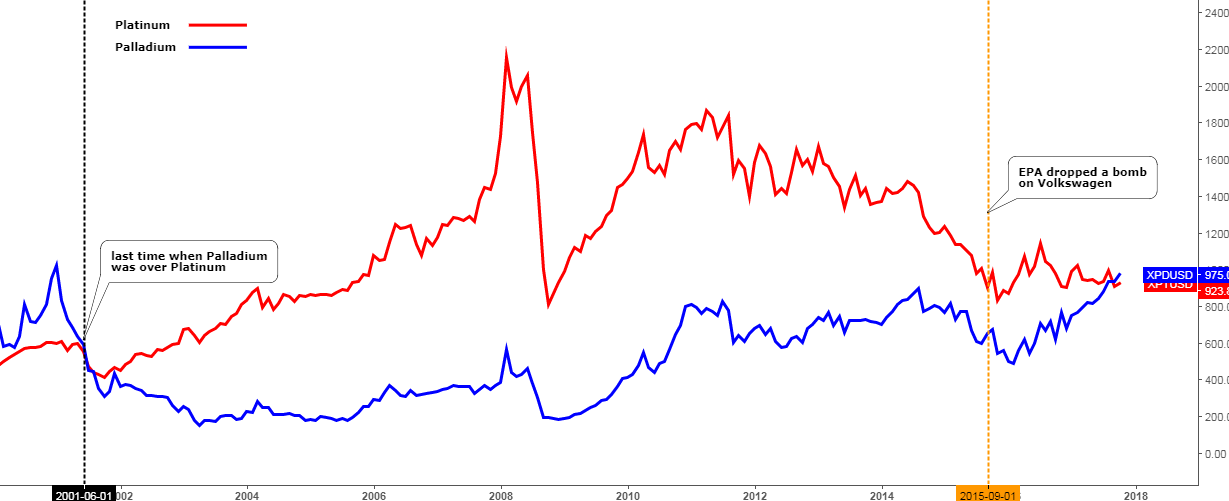

Chart 1. Platinum Vs. Palladium: Crossed Swords

Chart courtesy of tradingview.com

Sixteen years ago was the last time that platinum was cheaper than palladium in 2001 (black vertical line). By then palladium had spent a year in the dominant position over platinum, and at that time the price of both metals had been fluctuating around $600 level. Since then platinum has returned to its usual upper position to palladium, and the gap was growing exponentially in favor of platinum until it reached the peak with the $1600 of supremacy in 2008. After that, the gap began to narrow and last month it entirely evaporated as a global shift in the automotive industry showed a growing demand for gasoline and hybrid cars (palladium related) amid slowing demand for diesel cars (platinum related).

The Volkswagen emissions scandal started on the 18th of September 2015 (orange vertical line), when the United States Environmental Protection Agency (EPA) issued a notice of violation. I dedicated a post in 2015 to that significant event. The price of both metals continued higher right after that news as the reaction time to such a report always has a gap in such a giant industry.

But in the next month, we saw a massive drop in both metals of more than $100, and the fall of palladium price had lasted longer. The weakness, then suddenly ceased and both metals won back all of their losses and climbed into positive territory. And two years after the investigations started platinum is still in a little profit as palladium just hit a multi-year maximum with more than $300 in the green.

It looks like a tangible shift in the automobile industry has started to evolve this year as sales of gasoline-powered cars have overtaken diesel in the first half of this year for the first time since 2009 according to the European Automobile Manufacturers Association (ACEA). Sales of “alternative” vehicles - hybrid, electric, LPG (liquefied petroleum gas) and natural gas-powered ones rose by more than 35% (gasoline-powered cars +10%, diesel-powered vehicles minus 4%).

This is terrible news for platinum and good news for palladium because at the end of the day the gasoline-powered cars cannot escape from emissions tightening or even a total ban as has been planned in France and Britain. China with lousy air pollution could follow the pack as it is going to shift to green energy and it has great potential for being a global leader in green technology. So palladium’s triumph could be temporary.

Chart 2. Platinum Monthly: Watch Consolidation

Chart courtesy of tradingview.com

The chances for the strength of platinum would grow only when the metal overcomes the long-term trendline resistance (thick red line, $1170-$1180). The big picture looks like a large consolidation of platinum, and we could be in the final stage (black converging trend channel) as the first leg appeared in 2008 amid the global crisis. Therefore, it was quick and severe as fear crashed the market.

It looks like the market is currently trapped in a consolidation from December of 2016 between $890 and $1045 marks (orange box). Thus, the possibility of the downtrend extending lower is higher. The immediate support is located at the $890 (downside of consolidation), and we should watch that level carefully.

The next level of support (red dotted horizontal line) is located at the $752 mark (2008 low). This level could offer strong support for the metal as last time the considerable strength of the platinum emerged when the price reached that area. The last area of support is located at the downside of the black channel within the $500-530 area.

Chart 3. Palladium Monthly: Reaching Out Major Top

Chart courtesy of tradingview.com

Palladium is in a vast range which lasts from the previous century. This range is also extensive as the price fluctuates between $144 and distant $1100 mark. The strong move to the upper side started in 2008 making the higher top (2014) and higher low (2016). I used these points to build an orange uptrend within the range. The upside of this trend overlaps the major top area at the $1100 mark with a small margin. I think the current upside move could tag that area as we can see some acceleration in the price action.

The black trendline support is the line in the sand, which should be triggered once weakness appears. I highlighted the tops on the RSI sub-chart to show you previous bearish divergence, which played out dramatically cutting the price by a half from 2014 to 2016. The current RSI level stands at the 67 level. It means that another bearish divergence has been accumulated as the previous top in the RSI is located at a higher 70 level (2014) while the price behaves opposite – the current maximum at $1009 level exceeds the previous peak at the $910 level.

We have strong upside momentum amid accumulating bearish divergence, and we’ll have to wait and see which one will play out. But this situation is quite natural as before any reversal the fight of opposite market forces gets to extreme levels.

Intelligent trades!

Aibek Burabayev

INO.com Contributor, Metals

Disclosure: This contributor has no positions in any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.

What about "fundamental" factors, such as the supply and cost to produce these metals? Also, aside for automobile/emissions uses, are there any specific advantages between each of these metals?

Dear Mr. Waserman,

Thank you for a good question.

Fundamentals reflect the price behavior of both metals accurately as Palladium has projected supply deficit of 1.8 million ounces this year amid balanced market in Platinum (only 44,000-ounce projected supply deficit this year).

Both metals could replace each other in automobile catalysts but this is a costly and time consuming process of making re-tool of the production sites. Producers would wait if the price normalisation again take place for the next 2-3 years before any major change could be introduced. As I highlighted in the post above - the threat of ban of global fossil fuel powered engines could damage substantial part of demand for both metals in the long run and therefore could affect producers' plans for catalyst interchange. The "winter" is coming for both of the metals.

Best wishes, Aibek