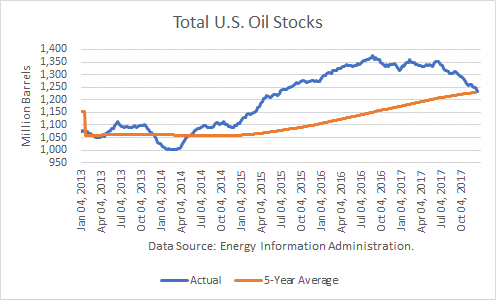

According to the Energy Information Administration (EIA), U.S. petroleum inventories (excluding SPR) fell by 14.2 million barrels in the week ending December 15, 2017. They stand about 2 million barrels (mmb) higher than the rising, rolling 5-year average and are about 96 mmb lower than a year ago.

Commercial crude stocks fell by 6.5 mmb, and SPR stocks were built by 0.4 mmb last week. Gasoline stocks rose by 1.2 mmb, and distillate stocks gained 0.8 mmb. Primary demand rose by 640,000 b/d to average 19.948 million barrels per day (mmbd).

Crude Production

The EIA estimated (using its model, click here for presentation) that U.S. crude production rose by 9,000 barrels per day to 9.789 mmbd, the highest week in EIA’s database. Production averaged 9.740 mmbd over the past four weeks, up 11.4% v. a year ago. In the year-to-date, crude production averaged 9.313 mmbd, up 6.3% v. last year. Continue reading "U.S. Production And Oil Inventories Expected to Rise in 1Q18"