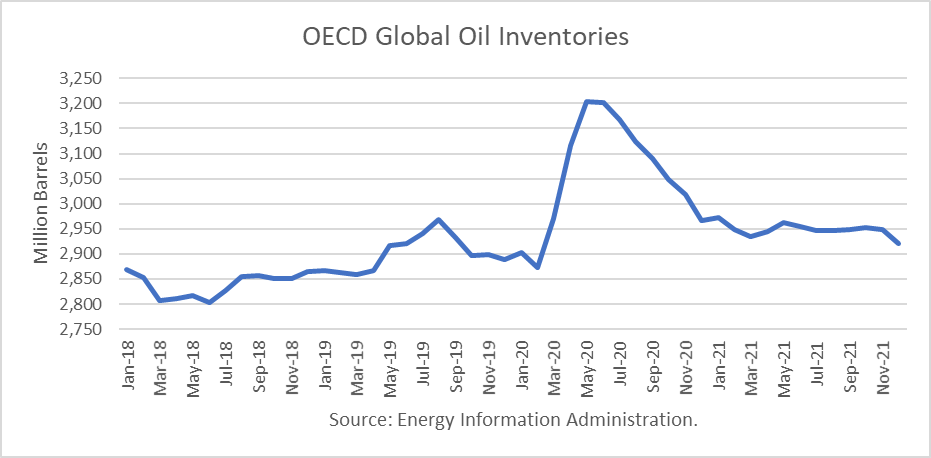

The Energy Information Administration released its Short-Term Energy Outlook for September, and it shows that OECD oil inventories likely bottomed in this cycle in June 2018 at 2.804 billion barrels. Stocks peaked at 3.204 billion in May 2020. In September 2020, it estimated stocks dropped by 34 million barrels to end at 3.090 billion, 123 million barrels higher than a year ago.

The EIA estimated global oil production at 91.70 million barrels per day (mmbd) for September, compared to global oil consumption of 95.26 mmbd. That implies an undersupply of 3.56 mmbd or 110 million barrels for the month. About 76 million barrels of the draw for September is attributable to non-OECD stocks.

For 2020, OECD inventories are now projected to build by a net 87 million barrels to 2.967 billion. For 2021 it forecasts that stocks will draw by 46 million barrels to end the year at 2.921 billion.

The EIA forecast was made incorporates the OPEC+ decision to cut production and exports. According to OPEC’s press release: Continue reading "World Oil Supply And Price Outlook, October 2020"